We recognize what matters today for many funds is helping portfolio companies survive a sharp drop in revenues rather than discerning how much first quarter marks may fall from the last valuation.

Scooter rental firm Lime reportedly is trying to raise capital at a valuation that is 80% below its last raise. Dilution and a valuation mark-down may be a bitter pill for existing investors, but for many money losing enterprises with dwindling cash such as Lime, it is unavoidable if the firm is to survive.

Our focus is on valuing illiquid securities, not sourcing capital. One of our colleagues once said that valuing private equity and credit portfolios is about marking as close to market as possible; it is not marking to a price target predicated on an investment thesis. The accountants provide perspective and guidance, but not precision beyond the preference hierarchy of Level 1 vs. Level 2 vs. Level 3 valuation inputs. ASC 820-10-20 defines fair value as, “the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.” Fair value from the accountant’s perspective represents the exit price of the subject asset for a market participant in the principal or most advantageous market. Exit multiples are a theoretical concept today in which private equity and credit markets are frozen, but that will not always be the case. One never knows how much price dislocation is due to illiquidity vs. the market’s reassessment of fundamentals. Time will tell, but the impact of the governments response to COVID-19 on the economy is unlikely to be transitory. As it relates to marking private equity and credit to market or some semblance thereof, we offer these initial thoughts:

So how does one value private equity and credit in a developing recession or depression that may be very deep and of an unknown duration? Our view is that investors will be more focused than ever on cash flow and earning power because the era of ridiculous valuations on flimsy pro-forma EBITDA is over.

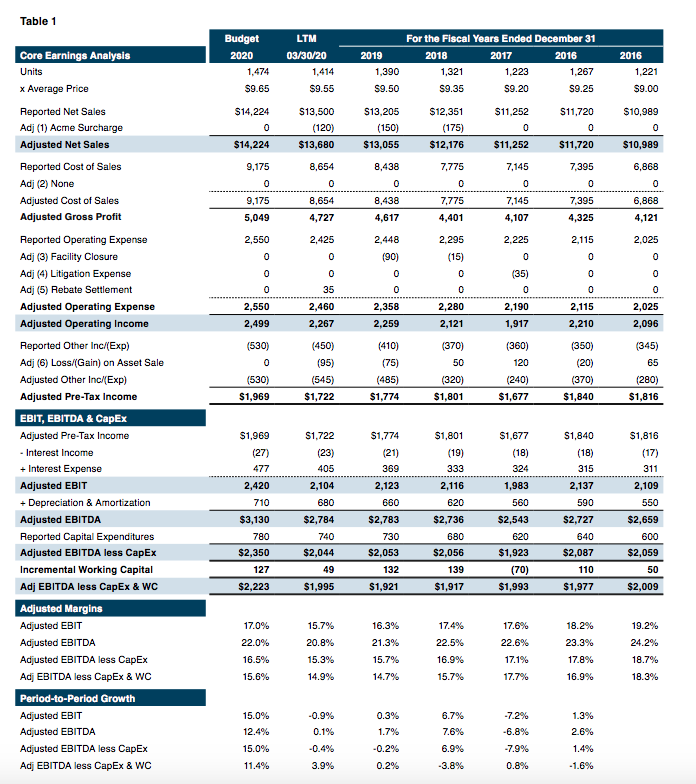

Table 1 provides a sample overview of the template we use at Mercer Capital. The process is not intended to create an alternate reality; rather, it is designed to shed light on core trends about where the company has been and where it may be headed. Adjustments are intended to strip-out non-recurring items and items that are not related to the operations of the business.

In addition, EBITDA is but one measure to be examined because EBITDA is a good base earnings measure, but it does not measure cash flow. Capex, working capital and debt service requirements are to be considered, too.

The adjusted earnings history should create a bridge to next year’s budget, and the budget a bridge to multi-year projections. The basic question to be addressed: Does the historical trend in adjusted earnings lead one to conclude that the budget and multi-year projections are reasonable with the underlying premise that the adjustments applied are reasonable?

The analysis also is to be used to derive earning power. Earning power represents a base earning measure that is representative through the firm’s (or industry’s) business cycle and therefore requires examination of earnings over an entire business cycle. If the company has grown such that adjusted earnings several years ago are less relevant, then earning power can be derived from the product of a representative revenue measure such as the latest 12 months or even the budget and an average EBITDA margin over the business cycle.

Terminal values like cash flow will be subjected to more scrutiny, too. As noted previously, guideline transaction data is not as informative today given the change to the economy that has occurred. That is not to say guideline company and transaction data is not relevant, but probably requires a larger than normal haircut for fundamental adjustment.

Alternatively, the build-up method in which current earning power and the terminal value cash flow in a DCF model are capitalized may provide a better estimate of fair value than pre-COVID transaction data.

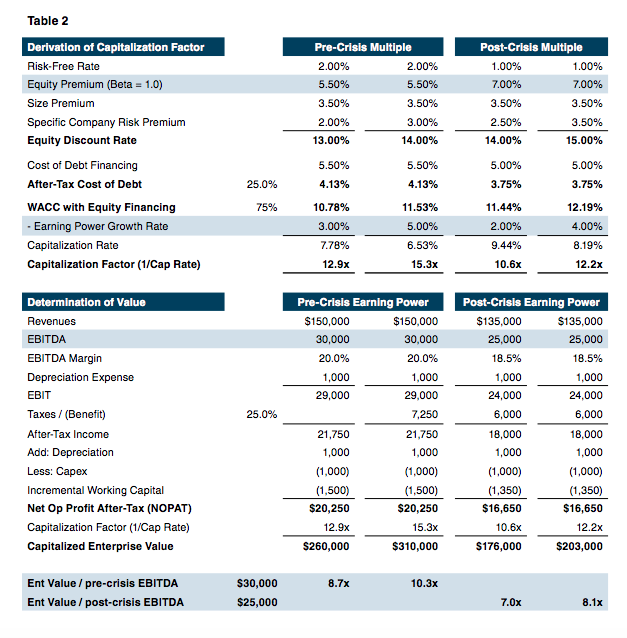

Table 2 presents a perspective on why market participants may often times conclude the multiple applicable to a given company should be lower in the post-COVID-19 world. The process will lead to lower values than would have been derived prior to February 2020 because earning power and cash flow projections will be lower; risk premium applied to develop a weighted average cost of capital will be greater; and the expected long-term growth rate in earning power will be lower. That may change over time as risk premia recede and business cash flows rebound, but that is not the world that exists today as it relates to marking-to-market (or model).

Originally published in Mercer Capital’s Portfolio Valuation | Private Equity and Credit Newsletter

{kind=link}

{kind=link}