2018 Was a Banner Year for Asset Manager M&A

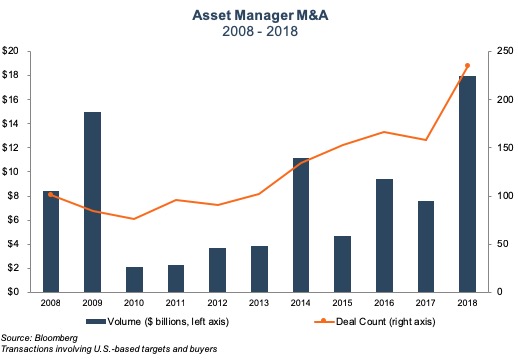

Asset manager M&A was robust throughout 2018 against a backdrop of volatile market conditions. Several trends which have driven the uptick in sector M&A in recent years continued into 2018, including increasing activity by RIA aggregators and rising cost pressures. Total deal count during 2018 increased 49% versus 2017 and total disclosed deal value was up nearly 140% to $18.0 billion. In terms of both deal volume and deal count, asset manager M&A reached the highest levels since 2009.

M&A was particularly strong in the fourth quarter when Invesco Ltd. (IVZ) announced plans to acquire the OppenheimerFunds unit from MassMutual for $5.7 billion in one of the largest sector deals over the last decade. IVZ will tack on $250 billion in AUM as a result of the deal, pushing total AUM to $1.2 trillion and making the combined firm the 13th largest asset manager by AUM globally and the 6th largest by retail AUM in the U.S. The deal marks a major bet on active management for IVZ, as OppenheimerFunds’ products are concentrated in actively-managed specialized asset classes, including international equity, emerging market equities, and alternative income. Invesco CEO Martin Flanagan explained the rationale for scale during an earnings call back in 2017:

“Since I’ve been in the industry, there’s been declarations of massive consolidation. I do think though, this time there are a set of factors in place that weren’t in place before, where scale does matter, largely driven by the cost coming out of the regulatory environments and the low rate environments in cyber and alike.” Martin Flanagan, President and CEO, Invesco Ltd. – 1Q17 Earnings Call

RIA aggregators continued to be active acquirers in the space, with Mercer Advisors (no relation), and United Capital Advisors each acquiring multiple RIAs during 2018. The wealth management consolidator Focus Financial Partners (FOCS) has been active since its July IPO as well. In August, FOCS announced the acquisition of Atlanta-based Edge Capital Group, which manages $3.5 billion in client assets. FOCS also announced multiple sub-acquisitions by its affiliates during the second half of 2018.

Consolidation Rationales

The underpinnings of the M&A trend we’ve seen in the sector include increasing compliance and technology costs, broadly declining fees, aging shareholder bases, and slowing organic growth for many active managers. While these pressures have been compressing margins for years, sector M&A has historically been muted, due in part to challenges specific to asset manager combinations, including the risks of cultural incompatibility and size impeding alpha generation. Nevertheless, the industry structure has a high degree of operating leverage, which suggests that scale could alleviate margin pressure as long as it doesn’t inhibit performance.

“Absolutely, this has been an elevated period of M&A activity in the industry and you should assume … we’re looking at all of the opportunities in the market.” Nathaniel Dalton, CEO, Affiliated Managers Group Inc – 2Q18 Earnings Call

“Increased size will enable us to continue to invest in areas that are critical to the long-term success of our platform, such as technology, operations, client service and investment support, and to leverage those investments across a broader base of assets.” David Craig Brown, CEO & Chairman, Victory Capital – 3Q18 Earnings Call

Consolidation pressures in the industry are largely the result of secular trends. On the revenue side, realized fees continue to decrease as funds flow from active to passive. On the cost side, an evolving regulatory environment threatens increasing technology and compliance costs. Over the past several years, these consolidation rationales have led to a significant uptick in the number of transactions as firms seek to realize economies of scale, enhance product offerings, and gain distribution leverage.

Market Impact

Recent increases in M&A activity come against a backdrop of a long-running bull market in asset prices that finally capitulated in late 2018. Over the past several years, steady market gains have more than offset the consistent and significant negative AUM outflows that many active managers have seen. Now that the market has pulled back, AUM, revenue, and earnings are likely to be lower for many asset managers.

The recent market pullback will impact sector deal making in several ways. Notably, earnings multiples for publicly traded asset managers have fallen considerably during 2018, which suggests that market sentiment for the sector has waned as the broader market has declined. While the lower multiple environment is clearly less favorable for sellers, market volatility may force some smaller, less profitable firms into selling in order to remain viable. For buyers, the lower multiple environment may make the sector look relatively underpriced though some may be spooked by the recent volatility.

M&A Outlook

With over 11,000 RIAs currently operating in the U.S., the industry is still very fragmented and ripe for consolidation. Given the uncertainty of asset flows in the sector, we expect firms to continue to seek bolt-on acquisitions that offer scale and known cost savings from back office efficiencies. Expanding distribution footprints and product offerings will also continue to be a key acquisition rationale as firms struggle with organic growth. An aging ownership base is another impetus. The recent market volatility will also be a key consideration for both sellers and buyers in 2019.