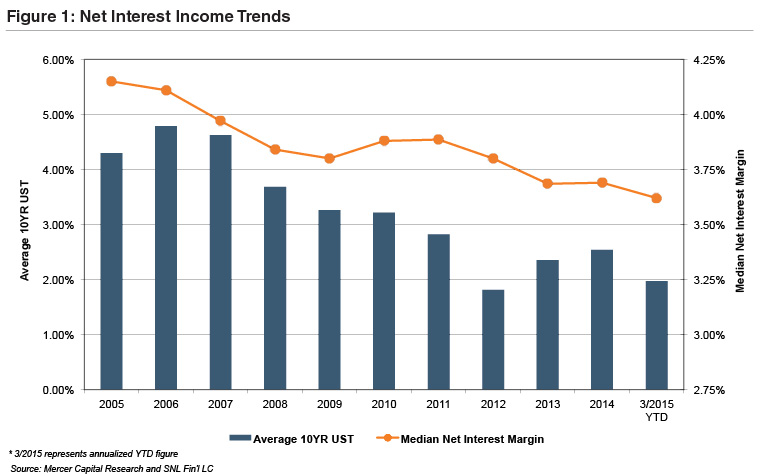

Following the Great Recession, significant attention has been focused on bank earnings and earning power. While community bank returns on equity (ROE) have improved since the depths of the recession, they are still below pre-recession levels. One factor squeezing revenue is falling net interest margins (i.e., the difference between rates earned on loans and securities, and rates paid to depositors). Community banks are more margin dependent than their larger brethren and have been impacted to a greater extent from this declining NIM trend. As detailed in Figure 1 below, NIMs for community banks (defined to be those with assets between $100 million and $5 billion) have steadily declined and were at their lowest point in the last ten years in early 2015.

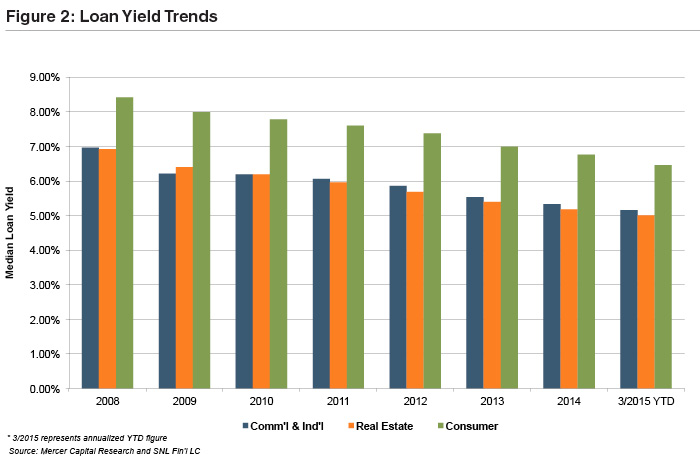

While there are a number of factors that impact NIMs, the primary culprit for the declining trend is the interest rate environment. As the Federal Reserve’s zero-interest rate policy (“ZIRP”) grinds on, earning asset yields continue to reprice lower while deposit costs reached a floor several quarters ago. Loan growth has also been challenging for many banks for a variety of reasons, which has stoked competitive pressures and negatively impacted lending margins. While competitive pressures can come in many forms, several data-points indicate intense loan competition giving way to easing terms. For example, the April 2015 Senior Loan Officer Opinion Survey on Bank Lending Practices noted continued easing on terms in a number of loan segments. This appears to be supported further by reported community bank loan yields, which have slid close to 200 basis points (in all loan segments analyzed) since 2008 as shown in Figure 2.

Aside from paying tribute to the late B.B. King and playing “Everyday, everyday I have the blues,” what can community bankers do in order to combat the margin blues? While not all-encompassing, below we have listed a few strategic options to consider:

Mercer Capital has a long history of working with banks and helping to solve complex problems ranging from valuation issues to considering different strategic options. If you would like to discuss your bank’s unique situation in confidence and ways that your bank may consider addressing the margin blues, feel free to give us a call or email.