Is business ownership a binary thing? Do we either own our businesses or not? The binary notion leads business owners to think either in terms of either the status quo or of an eventual sale of the business.

The truth is that between the two bookends of status quo and an eventual third-party sale are many possibilities for creating shareholder liquidity and diversification and facilitating both ownership and management transitions. We call this time “interim time.” The literal translation of “interim” from the original Latin means, “the time between.” Interim time, then, is the time between now, or the current status quo of a business, and an ultimate sale of that business. Let’s look at the bookends:

Managing illiquid, private wealth in private businesses is far more than running the businesses themselves. We all have to manage our businesses. Managing the wealth in our businesses requires a much more active role for business owners and often a different level of attention on the business itself.

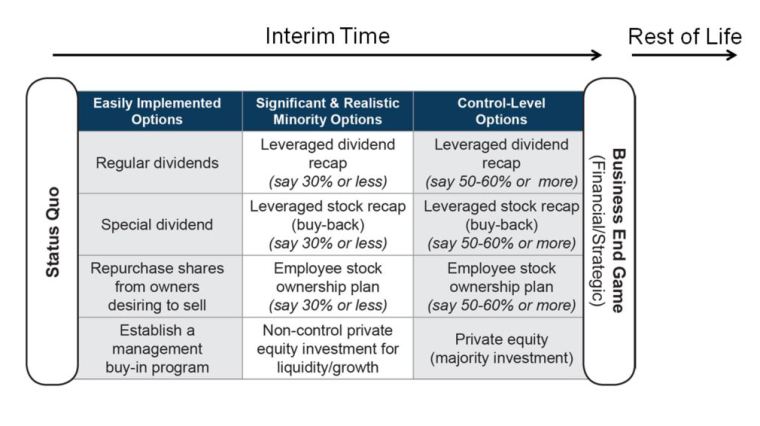

The status quo and an eventual third-party sale are, indeed, bookends. Consider the table.

If we are managing the wealth in our closely held and family businesses, we will be focused on creating liquidity opportunities over time and on achieving reasonable returns from our companies on a risk-adjusted basis. We will be using our companies as vehicles to generate liquid wealth and diversification opportunities over time.

The table shows the bookends of status quo and third-party sale options. In between are a number of options that owners of successful private companies can use to manage the wealth tied up in them and to create ongoing opportunities for liquidity and diversification.

At the far right, after the sale of a business, its owners must, in many cases, be prepared for the rest of their lives. So it is important to run a business in such a way that its owners develop liquidity and diversification to create options for the rest of their lives.

The table is certainly not all inclusive, but it does include some easily implementable options like establishing a dividend/distribution policy or making occasional share repurchases as owners need some liquidity or, for example, when an owner leaves the company. This purchase might be pursuant to the terms of a buy-sell agreement.

If your company has significant excess assets, it is probably a good idea to clean up your balance sheet and declare a special dividend. And it may be appropriate to have one or more key managers acquire small stakes in the company to facilitate alignment and future management transitions.

I call these options “easily implementable,” but they won’t happen unless someone does something.

The next category of options in the table above are termed “significant and realistic minority options.” They include relatively small leveraged dividend recapitalizations or share repurchases. The options also might include the creation of a 30% or less ESOP in appropriate circumstances. These transactions certainly won’t happen without someone doing something. They will likely require the assistance of outside expertise, and there will be certain transaction costs. Transaction costs should be considered in the context of investments.

The third category after the status quo is called “control level options.” For some successful private companies, it may be appropriate to engage in substantial transactions to create liquidity opportunities and to retain ownership in expected future growth and appreciation. Options here include:

The final category is the bookend of third-party sale transactions. It should now be clear that there are options other than selling a business today, or simply maintaining the status quo, for managing the illiquid wealth in your private company.

The shareholder benefits of employing one or more of the above strategies over time include the following:

Employing one or more of the above The One Percent Solution strategies is tantamount to using modern investment theory concepts and basic corporate finance tools in the management of illiquid private company wealth.

For more information or to discuss a valuation and transaction issue in confidence, please do not hesitate to contact us.