Although it is difficult to discern with the ten-year U.S. Treasury presently yielding about 2.4% compared to 3.0% at the beginning of the year, many market participants believe the Federal Reserve will begin to raise the Fed Funds target rate next year. The thought process is not illogical. Consider that:

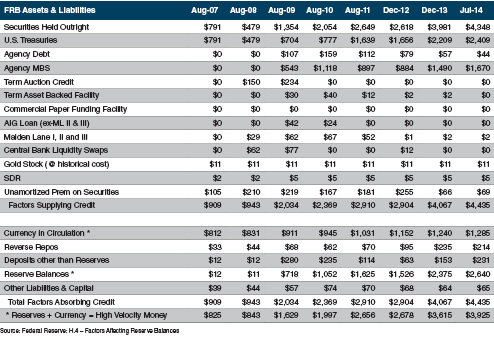

How high short-term rates may rise is unknown. (A corollary question for others is what, if anything, will the Fed do with its enlarged balance sheet as shown in Table 1.) Pimco’s Bill Gross has opined that the “new neutral” target rate will be around 2% rather than a historical policy bias of 4%. For lenders, money market funds and trust/processing companies, a hike in short rates cannot occur soon enough.

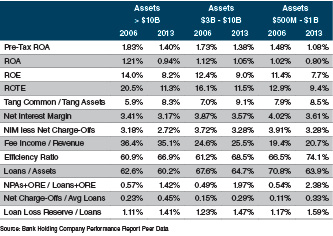

Although the Fed’s zero interest rate policy (“ZIRP”) helped reinvigorate markets, the economy and asset quality, it is increasingly weighing on revenues via depressed net interest margins (“NIM”) and post-recession profitability as shown in Table 2.

For traditional banks that primarily rely upon spread revenue, this is especially true. Funding costs cannot go lower, while asset yields remain under pressure. The asset yield story is nuanced, however. Bond portfolio yields have stabilized after years of cash flows being reinvested at lower rates. Loan portfolio yields partly depend on the mix, but the general trend since the financial crisis occurred continues to be down for two reasons. One is the reduction in the base rate (LIBOR, swap rate and 5-/10-year U.S. Treasury) that occurred during 2008-2011. Since then lower loan yields largely have reflected intensifying competition as lenders become more confident about the economy and less tolerant of holding excess amounts of liquidity and bonds. Banks have lowered or waived loan floors and have been willing to accept lower margins over the base rate to put higher yielding assets on the books. Some may recall the mantra last heard in 1993 when the Funds target was 3.0% and again in 2003 when it was 1.0%: “cash is trash.”

The other nuanced aspect of asset yields is the impact gradually improving loan growth for a broader swath of the industry has had on NIMs. Funding loan growth with excess liquidity and bonds entails a yield pick-up. What intensified competition does not show until the credit cycle turns is how much credit standards were relaxed to drive volume. Time will tell, though anecdotal stories we hear indicate there has been significant loosening of standards.

Should the FOMC follow through and raise short rates next year, most banks with a reasonable amount of LIBOR- and/or prime-based loans and non-interest bearing deposits will see revenues increase—provided deposit rates do not have to be raised aggressively and there are not too many (or too high) loan floors.

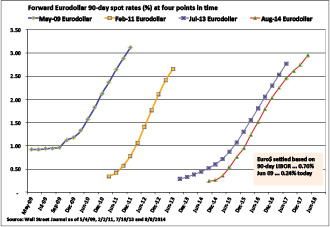

It seems like an ideal set-up for banks if the Fed will do its part. That said, we have been here before. Figure 3 reflects the forward Eurodollar curve at four separate dates: May 2009, February 2011, July 2013 and August 2014. Eurodollar contracts reflect future spot rates for U.S. dollars based upon where 90-day LIBOR is expected to settle. The contracts trade in a highly liquid market, unlike those for Fed Funds futures.

What Figure 3 shows is that the market has expected short rates to rise soon as soon as ZIRP was implemented. In May 2009, the expectation was that by late 2010 short rates would begin to rise. In early 2011, a strong fourth quarter 2010 GDP report (+3.2%) pushed contract prices down and forward spot rates sharply higher. The forward curve in July 2013 reflected higher short rates by late 2014. Currently, the forward curve projects higher short rates by mid-2015. And on it goes.

Bank executives and directors should be planning if the inevitable does not happen. Worse, what happens if rates stay low before the next recession occurs? Banks will struggle with a lower cushion in the form of pre-tax, pre-provision earnings to fund losses and/or build loan loss reserves than would be the case if short-rates and the NIM were higher. Of course, Dodd-Frank has mandated higher capital ratios to cushion losses as a perverse offset to ZIRP.

We at Mercer Capital have differing opinions about how Fed policy will evolve over the next year or two, but none of us (or you) knows for sure. Opinions are no substitute for planning. We do believe the planning process for a much longer period of ZIRP will require executives to think hard about the relevance of branch networks, the prudence of significantly shortening the duration of bond portfolios and how much credit risk is being assumed to achieve loan growth. A question that assumes more urgency is: Should the Board move sooner rather than later to sell or merge with a similar-sized institution if the Fed is not going to raise short rates (much) and thereby boost what may be an unacceptably low ROE for many banks?

We at Mercer Capital do not have the answer to every question, but we can help you ask the right questions and frame the answers in terms of thinking about shareholder value.

Reprinted from Bank Watch, August 2014.