A stress test is defined as a risk management tool that consists of estimating the bank’s financial position over a time horizon – approximately two years – under different scenarios (typically a baseline, adverse, and severe scenario).

Recent regulatory commentary suggests that community banks should be developing and implementing some form of stress testing on at least an annual basis. For additional perspective, consider the following excerpts:

While the potential regulatory benefits are notable, stress testing should be viewed as more than just a regulatory check-the-box exercise. Similar to stress tests performed by cardiologists to determine the health of a patient’s heart, bank stress tests can provide a variety of benefits that could serve to ultimately improve the health of the bank. Stress testing benefits include:

For example, a stronger bank may determine that it has sufficient capital to withstand extremely stressed scenarios and thus can consider acquisitions, special dividends, or buybacks. Alternatively, a weaker bank may determine that considering a sale or capital raise is the optimal path forward. Additionally, estimating loan losses embedded within a sound stress test can provide the bank with a head start on the pending shift in loan loss reserve accounting from the current “incurred loss” model to the more forward-looking approach proposed in FASB’s CECL (Current Expected Credit Loss) model.

We acknowledge that community bank stress testing can be a complex exercise as it requires the bank to essentially perform the role of both doctor and patient. For example, the bank must administer the test, determine and analyze the outputs of its performance, and provide support for key assumptions/results. There are also a variety of potential stress testing methods and economic scenarios for the bank to consider when setting up their test. In addition, the qualitative, written support for the test and its results is often as important as the results themselves. For all of these reasons, it is important that banks begin building their stress testing expertise sooner rather than later.

In order to assist community bankers with this complex and often time-consuming exercise, we offer three potential solutions to make the process as efficient and valuable as possible.

Our experts will review and validate your existing stress test model

This Toolkit provides a wealth of qualitative and quantitative data as well as excel models to assist your bank with the preparation of its Stress Test and/or Capital Plan. It was created specifically for community banks and intended to provide all the tools needed to perform a sound Stress Test.

While helpful for a variety of stress testing methods, the Toolkit is specifically designed to provide all the quantitative and qualitative pieces to assist banks with “top down” portfolio stress testing. OCC Supervisory Guidance noted, “For most community banks, a simple, stressed loss-rate analysis based on call report categories may provide an acceptable foundation to determine if additional analysis is necessary.”

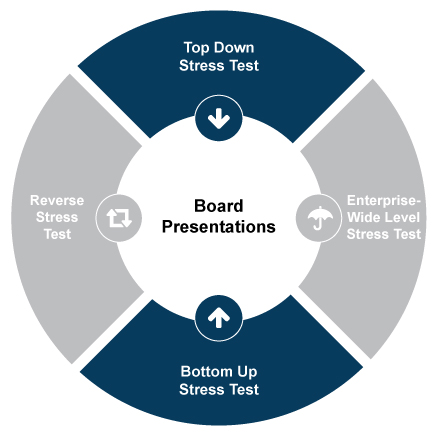

“Top Down” stress testing consists of estimating stress loss rates under different scenarios on pools of loans with common characteristics. Four key steps that this Toolkit can assist you with:

The Toolkit is our most cost-effective option and provides bank managers and directors with the key qualitative and quantitative tools needed to prepare a reasonable and sound stress test efficiently.

Mercer Capital’s Toolkit contains the following analyses specifically tailored to your institution:

For more information on Mercer Capital’s Stress Testing and Capital Planning Toolkit, contact Jay Wilson here.

The hallmark of community banking has historically been the diversity across institutions and the guidance from the OCC suggests that community banks should keep this in mind when adopting appropriate stress testing methods by taking into account each bank’s attributes, including the unique business strategy, size, products, sophistication, and overall risk profile. While not prescriptive in regards to the particular stress testing methods, the guidance suggests a wide range of effective methods depending on the Bank’s complexity and portfolio risk.

Having successfully completed thousands of community bank engagements over the last 30 years, Mercer Capital has the experience and expertise to understand your bank’s unique strengths and weaknesses and help to solve your complex stress testing issues.

Mercer Capital can help scale and improve your bank’s stress testing by assisting your bank in a variety of ways, ranging from providing advice and support for assumptions within your Bank’s pre-existing stress test to developing a unique, custom stress test for your bank that incorporates your bank’s desired level of complexity and adequately captures the unique risks facing your bank.

Depending on the design of your stress tests and the potential economic scenarios under consideration, we will prepare a stress test and provide specific research to assist with key assumptions. During the planning process of the engagement, we will work with you to determine the level of complexity needed to address your concerns and objectives.

Regardless of the approach, the desired outcome is a stress test that can be utilized by managers, directors, and regulators to monitor capital adequacy, manage risk, enhance the bank’s performance, and improve strategic decisions.

For more information, contact Jay Wilson here.

We provide custom stress testing services ranging from the “top-down” stress test to more rigorous forms of stress testing.

Top Down stress testing consists of estimating stress loss rates under different adverse scenarios on pools of loans with common characteristics. Top down stress testing consists of four key steps:

Mercer Capital has designed a stress test Toolkit specifically to assist with the Top Down Stress Testing Process and also has stress testing models that can be customized to fit your bank’s needs.

For more information or to speak with Mercer Capital, click here.

“Bottom Up” (also often referred to as transaction level stress testing) looks at key loan relationships individually, assessing the potential impact of adverse economic conditions on those borrowers, and estimating loan losses for each loan. The results of individual transaction level stress tests can then be aggregated to provide portfolio level results.

Here the key steps include determining which loan relationships to assess individually (should it be limited to particular types of loans or relationships above a specific size or loans tied to a specific industry/sector or some other factor).

In order to assess the potential impact of the economic scenarios and loss rates under each scenario, estimates of the probability of default as well as severity of loss in the event of default should be determined. This typically requires an intensive analysis of each credit and looking at key characteristics for each credit such as financial performance (debt-service coverage ratios, guarantor support), past-due history, collateral type and estimated value.

Once the loss rates are estimated for particular loans or loan relationships then the losses are estimated for each loan portfolio segment by aggregating the results.

Reverse Stress Testing can also be performed whereby a specific adverse outcome is assumed that is sufficient to breach the bank’s capital ratios (often referred to as a “break the bank” scenario). Management then considers what types of events could lead to such outcomes. Once identified, management can then consider how likely those conditions are and what contingency plans or additional steps should be made to mitigate this risk.

Enterprise-Wide Level Stress Testing attempts to take risk management out of the silo and consider the enterprise-wide impact of a stress scenario by analyzing “multiple types of risk and their interrelated effects on the overall financial impact.”

The risks might include credit, counter-party credit, interest rate, liquidity, reputational, operational, or legal risk. In its simplest form, enterprise-wide stress testing can entail aggregating the transaction and/or portfolio level stress testing results and then incorporating these other risks into scenario modeling to consider related impacts across the firm from the stressed scenario previously considered.

We can discuss your internally or externally prepared stress test with your board to ensure that they understand the results and help to prioritize their strategic objectives/initiative.

For more information, contact Jay Wilson here.

If you need an expert to review or validate your existing stress test model, we can help.

Mercer Capital is one of the nation’s leading financial institution valuation and consulting firm. Our professionals have over 30 years of experience working with bank management and boards of directors on strategic issues.

Mercer Capital’s confirmation & validation service can include:

A qualitative review of the conceptual soundness of the methodologies being used, as well as the depth and appropriateness of supporting documentation is part of our service. Also included in our validation services is an in-depth report to assist your internal teams with stress testing requirements and help gain regulatory approval.

For more information, contact Jay Wilson here.

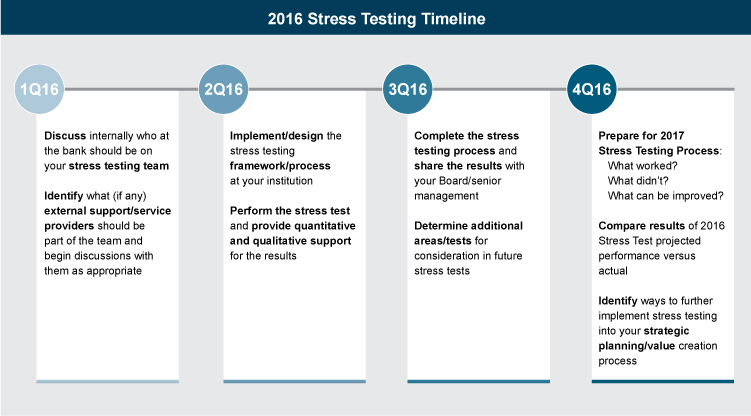

We created a timeline that can help your bank develop a stress testing process and framework appropriate for the size and complexity of your institution.

Mercer Capital is the nation’s premier financial institution valuation and consulting firm. Mercer Capital assists banks, thrifts, credit unions, and other depository institutions with significant corporate valuation requirements, transactional advisory services, and other strategic decisions.

Founded in 1982, in the midst of and in response to a previous crisis affecting the financial services industry, Mercer Capital has witnessed the industry’s cycles. Today, as in 1982, Mercer Capital’s largest industry concentration is financial institutions.

Despite industry cycles, Mercer Capital’s approach has remained the same – understanding key factors driving the industry, identifying the impact of industry trends on our clients, and delivering a reasoned and supported analysis in light of industry and client specific trends.

The Financial Institutions Group of Mercer Capital provides a broad range of specialized valuation and advisory services to the financial services industry.

Through a number of community bank engagements performed, Mercer Capital has developed several areas of expertise.

Mercer Capital’s loan valuation work product, including likelihood of default and loss severity assumptions for both loan portfolios, as well as individual loans, has withstood review and scrutiny of both accounting firms and regulatory agencies.

You can rely on the industry expertise and analytical rigor of Mercer Capital for your stress testing needs.

To discuss a stress testing issue in confidence, contact a Mercer Capital professional.

Jay D. Wilson, Jr., CFA, ASA, CBA

901.685.2120 | wilsonj@mercercapital.com

Andrew K. Gibbs, CFA, CPA/ABV (Andy)

901.685.2120 | gibbsa@mercercapital.com

Jeff K. Davis, CFA

615.345.0350 | jeffdavis@mercercapital.com