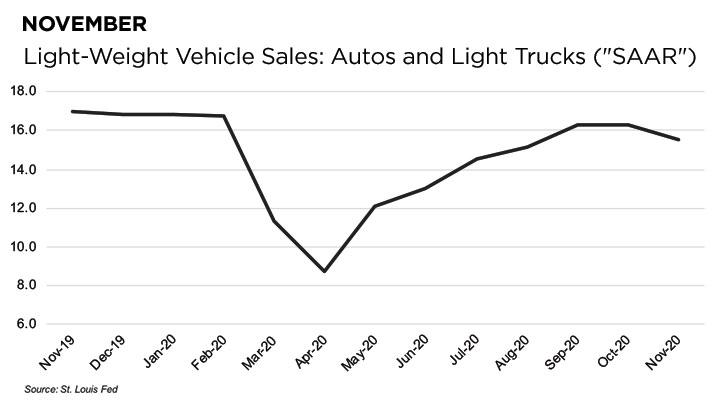

Mercer Capital › Auto Dealer Valuation Insights › SAAR › November 2020 SAAR › November-SAAR November-SAAR December 14, 2020