This following article was originally published by The Texas Lawbook.

It has been often discussed, particularly in recent years, that the value of privately held professional sports franchises is a newsworthy item. Analysts, investors, and fans alike have an interest in observing team owners buy and sell teams and watch the prices at which they trade. However, are team owners doing as well as some may portray? How about their investments as compared to their investing peers in the stock markets.

We attempt to answer these questions based on some known data sources and return analytics over time. The answers are interesting but not entirely clear.

There are two components to an investor’s rate of return: (i) interim returns in the form of cash flows or dividends, and (ii) price appreciation. Many commentators and writers have noted that some major league sports franchises have incurred operating losses in past years. For example, at one point it appeared that the MLB franchises on average had operating losses as players’ salaries increased faster than revenues. This was a big factor underlying the NFL and NHL lockouts in 2011 and 2012. There is a silver lining, however, and that appears to be the price appreciation realized from the increased values of these major league franchises.

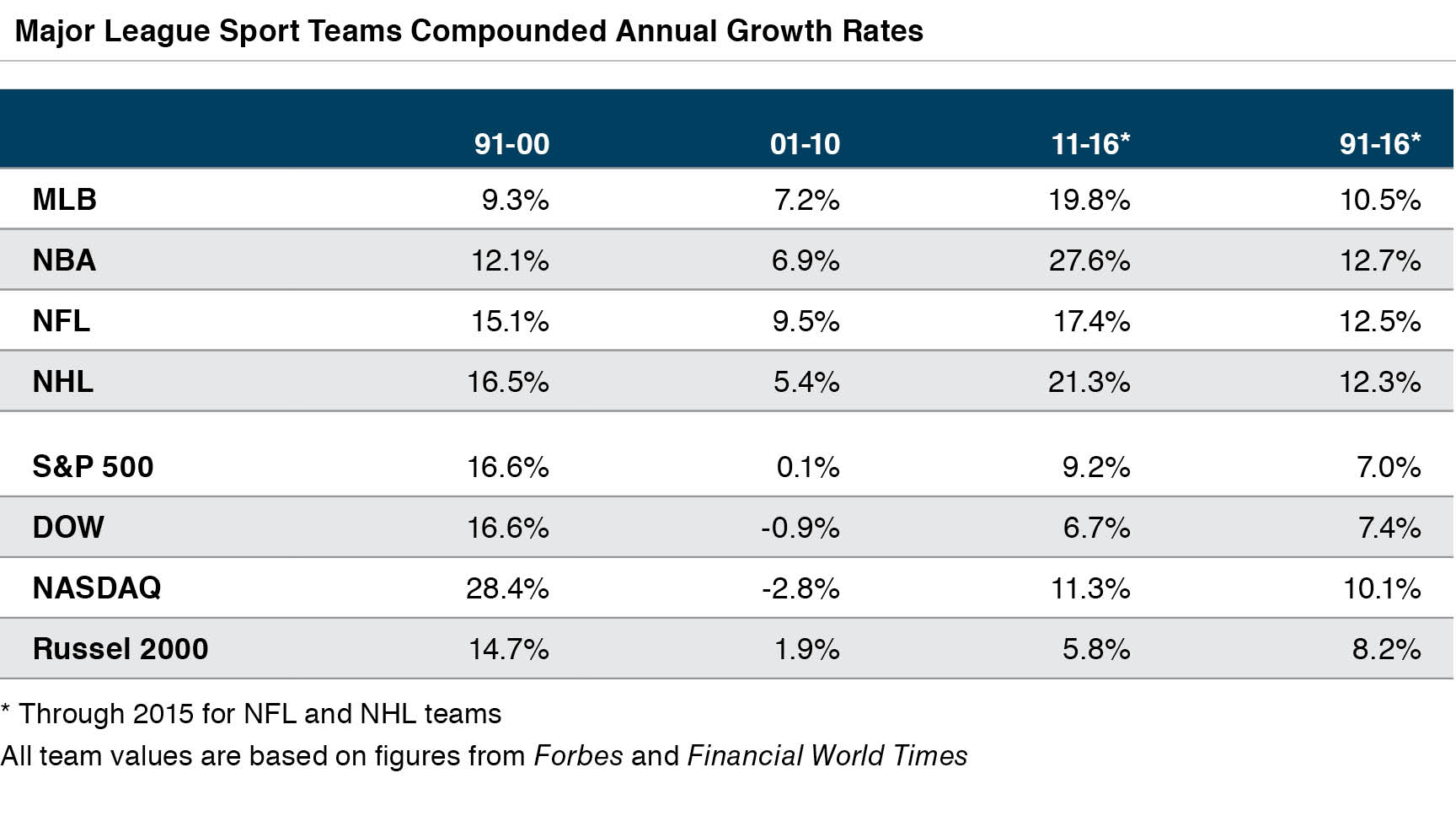

We traced over time the estimated appreciation (by league) of the values of sports teams, according to Forbes magazine. We also tracked the returns over the same time frames of several familiar equity market indices. The table below summarizes our findings.

We tracked this data going all the way back to 1991. We then sorted the returns over different decades – the 1990s, the 2000s, and our current decade. We aggregated it for the 25 total years of data.1

We observe that equity markets outperformed league appreciation in the 1990s, but the leagues caught up in the 2000s and 2010s. The biggest reason for the significant increase in the 2000s and the 2010s (among others) is television contracts – specifically, increases in national TV contracts for the NFL and NBA and regional and local contracts for MLB and NHL (and to a lesser degree the NBA as well).

Consider a few examples:

This increased TV revenue has been the primary driver of the very strong price appreciation in the 2000s and particularly in last five years (2011-2016).

In the last five years (2011-2016), the MLB team values have increased on average 19.8% compounded according to Forbes. The NBA Forbes value estimates increased by 27.6% for the same period. The NFL increased 17.4% and the NHL 21.3%. This short 5-year period has seen the highest percentage increase in the last 25 years. The compounded increases are 10% to 13% for the four major sports leagues over a 25-year period (1991-2016). In comparison, the DOW increased 7.4% compounded, the NASDQ 10.1% the S&P 500 7.0% and the Russell 2000 8.2%.

Therefore, solely from an appreciation point of view, an investment in a major league sports franchise appears to have been a very good return in the last 25 years, especially in the last five years. Of course, these returns vary by team and nothing is guaranteed. It is also notable that some teams have incurred operating losses that will offset a significant amount of the total return. This can impact investments in the form of debt or even capital calls from investors. This gets even more complicated when considering the value of minority interests in teams whereby the ability to monetize their returns is more uncertain. In fact, minority interests typically trade (however infrequently) at lower value levels than what the pro-rata value of a franchise would otherwise be worth. Therefore, appreciation returns that appear positive can come with drawbacks as well. Critical analysis is important to investors to help them determine if their returns are worth the risks.

Mercer Capital has arguably the most expertise in sports valuation and related stadium advisory in the country. For more information, contact one of our professionals.

1 We would note that Forbes does not have access to many team financials as teams are closely held (with the notable exception of the Green Bay Packers).Forbes relies on limited data and educated estimates of actual revenues and profits in order to make their estimated values.This is a limiting factor to properly value a single franchise at a single point in time.That said, as part of Forbes’ analysis they have interview access to a number of team owners to test the reasonableness of their valuations and key assumptions.In addition, their estimated values are adjusted year-to-year to account for actual sale prices of teams that sell.This is helpful when observing estimated aggregate values over a long period of time.