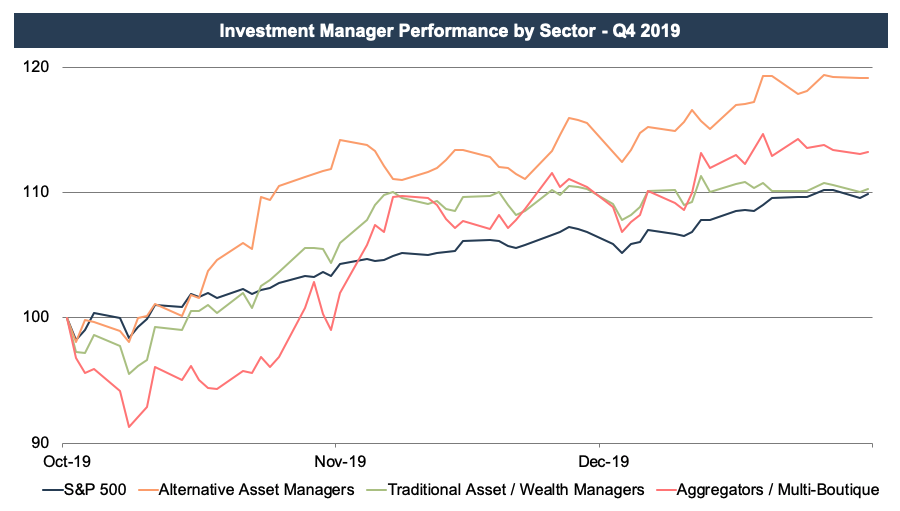

All Classes of Investment Management Firms Outperformed the Market in Q4

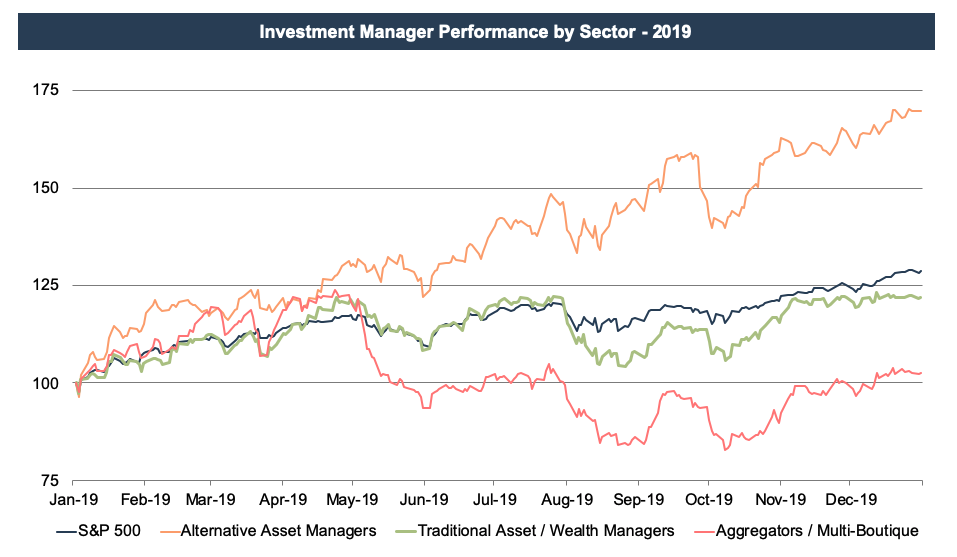

2019 Was Also a Bull Market for the RIA Industry

As good as the fourth quarter was for the S&P, it was even better for the RIA industry. All classes of investment management firms bested the market, which was up 10% for the quarter. Continued gains in the equity markets have allowed these firms to more than recover from last year’s correction, and many of these businesses are now trading at or near all-time highs.

Despite these gains, the asset management industry is facing numerous headwinds, chief among them being the ongoing pressure for lower fees. Alt managers, on the other hand, are perhaps more insulated from fee pressure due to the lack of passive alternatives to drive fees down.

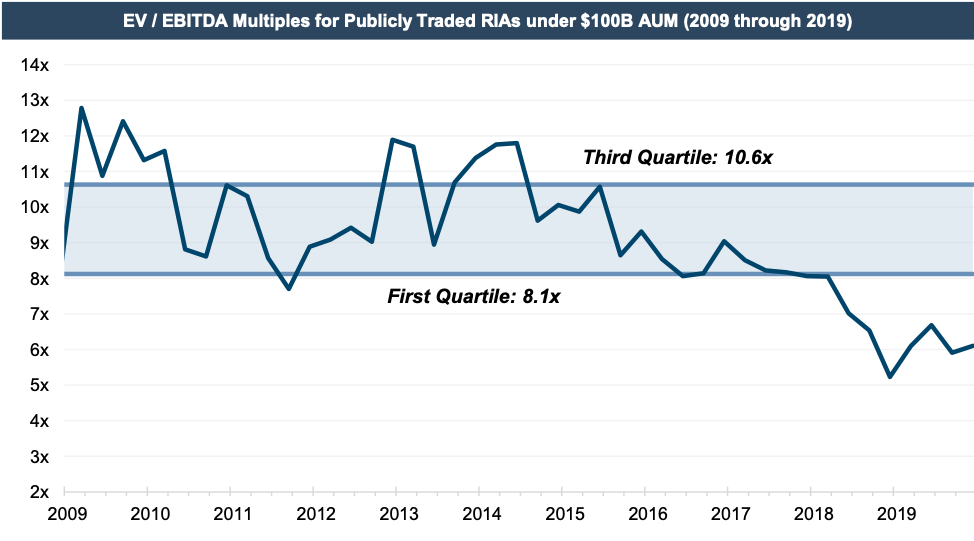

These headwinds have contributed to a decline in EBITDA multiples for traditional asset managers over the last few years despite the recent uptick in stock price performance. As shown below, EBITDA multiples for these businesses remain well below historical norms, although they have recovered from their low point in December of 2018.

Expanding the performance chart over the last year reveals an upward trend in pricing for most classes of RIAs. Over this longer timeframe, alt managers are still the strongest category, although performance has been volatile. Other pure play managers have generally moved in lockstep with the broader market while the aggregators lagged with AMG and FOCS’s performance.

The relative underperformance of the aggregator and multi-boutique index may come as a surprise given all the press about consolidation in the industry and headline deals for privately held aggregators. Over the last year, there have been two significant deals for privately-held wealth management aggregators: United Capital was bought by Goldman Sachs for $750 million, and Mercer Advisors’ PE backers sold a significant interest to a new PE firm, Oak Hill Capital Management. Both the United Capital and Mercer Advisors deals reportedly occurred at high-teens multiples of adjusted EBITDA.

Implications for Your RIA

With EBITDA multiples for publicly-traded asset managers still well below historical norms, it appears the public markets are pricing in many of the headwinds the industry faces. It is reasonable to assume that the same trend will have some impact on the pricing of privately-held asset managers as well.

But the public markets are just one reference point that informs the valuation of privately-held RIAs, and developments in the public markets may not directly translate to privately-held RIAs. Depending on the growth and risk prospects of a particular closely-held RIA relative to publicly-traded asset and wealth managers, the privately-held RIA can warrant a much higher, or much lower, multiple.

Improving Outlook

The outlook for RIAs depends on a number of factors. Investor demand for a particular manager’s asset class, fee pressure, rising costs, and regulatory overhang can all impact RIA valuations to varying extents. The one commonality, though, is that RIAs are all impacted by the market. Their product is, after all, the market.

The impact of market movements varies by sector, however. Alternative asset managers tend to be more idiosyncratic but are still influenced by investor sentiment regarding their hard-to-value assets. Wealth manager valuations are tied to the demand from consolidators while traditional asset managers are more vulnerable to trends in asset flows and fee pressure. Aggregators and multi-boutiques are in the business of buying RIAs, and their success depends on their ability to string together deals at attractive valuations with cheap financing.

On balance, the outlook for RIAs appears to have improved since the significant market drop in December 2018. Since then, industry multiples have rebounded somewhat, and the broader market has recovered its losses and then some—which should have a positive impact on future RIA revenues and earnings.

More attractive valuations could entice more M&A, coming off the heels of a record year in asset manager deal making. We’ll keep an eye on all of it during what will likely be a very interesting year for RIA valuations.