Starting later this week, the roads throughout Italy will be filled with more than the usual complement of exotic sports cars as the annual endurance race known as the Mille Miglia kicks off on May 18. The 1000 mile (or so) race was a major event between 1927 and 1957 in which major European auto manufacturers competed to show off not just the speed but the durability of their cars. Ferrari and Alfa Romeo typically dominated the event, although BMW won the only race held during World War 2 (go figure). For the past 30 years, the Mille Miglia has been a classic car tribute race in which wealthy collectors extravagantly thrash their pricey antique sports cars over vast stretches of Tuscan countryside and their livers with oceans of prosecco. If Mille Miglia was ever about the destination, today it is certainly all about the journey.

Focus Finds Another Way Point on the Journey to IPO

As part of the analyst community that closely follows developments in the investment management industry, we were disappointed (but not surprised) that Focus Financial Partners pulled their S-1, again, and found a private equity recap partner instead of going public. Picking up on last week’s blog theme, Focus likes to tout their strategy of building an international network of efficiently connected wealth management firms as an “unfair advantage”, but it appears that their real capability is finding capital when necessary to avoid a public offering. Stone Point Capital and KKR bought 70% of the company, enabling prior private equity partners, affiliates who had sold their firms to Focus in exchange for stock, and employees with equity compensation to monetize their positions while Focus remains private.

Stone Point / KKR’s investment thesis probably works something like this: wealth management is idiosyncratic, but also a relatively stable source of fees over time. Less threatened by robo-advisors and passive investing than the press would like to think, Focus Financial offers the opportunity to standardize back-of-the-house issues with a scaled up wealth advisory firm while keeping the storefront identity of advisors in place. That gives pricing power on the front end and efficiency on the back end to ultimately build a better sustainable margin. If this is successful, margin widens by five or ten percentage points relative to a stand-alone RIA. Focus can add more scale and some multiple arbitrage by buying smaller practices at single digit multiples. Once AUM tops $100 billion, you might pick up a turn on the EBITDA multiple. If markets don’t experience a prolonged decline during the holding period, Focus will pay Stone Point / KKR a high single-digit coupon on an unleveraged basis and/or will support some leverage to enhance ROE. With motivated advisors seeking new business and a market tailwind, private equity returns of 20% or more are available over the usual holding period of five to seven years, which has been getting longer because of a persistently weak IPO environment.

At present, private equity has the “unfair advantage” of tremendous access to capital and freedom from regulatory oversight. Focus has a significant head-start in creating a national platform for wealth advisory firms, and is positioned to take advantage of an increasing need for exits by the aging population of wealth advisors. Put Stone Point / KKR’s unfair advantage together with that of Focus, and suddenly there’s no need for an IPO.

Focus Fundamentals

There is plenty we don’t know about the recap, but we can infer a few things which explain the value of the transaction to the buyers. The ADVs of the 45 or so affiliate firms of Focus Financial reveal aggregate discretionary AUM at year end 2016 of approximately $60 billion, plus nondiscretionary AUM of another $15 billion for total AUM of over $75 billion. Per these ADVs, it also appears that almost all of the firms are wholly owned by Focus, so their AUM is wholly attributable to Focus Financial as well.

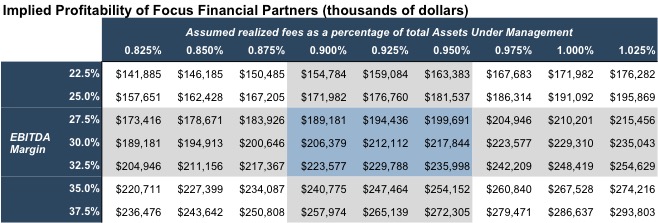

Revenue is a function of AUM and Focus’s realized (or actual) fee schedule. Focus Financial’s affiliate wealth management firms generally serve the upper end of the mass affluent market, such that we estimate realized fees of a little less than 100 basis points. Realized fees of 90 to 95 basis points on total AUM would suggest that Focus generates revenue of $700 million to $725 million annually.

We are curious about what sort of margin Focus has been able to demonstrate. The theory behind a roll-up (Focus executives insist the firm is not a roll-up) is economies of scale through common platforms, bundled research and technology, centralized marketing support, and other back office necessities. The question is how much are these efficiencies mitigated by the need for executive infrastructure, corporate development staff, integration costs, and the like. One final complication is what compensation levels have to be to motivate revenue producers at Focus’s affiliate firms. The RIA community is famous for mixing equity returns and compensation, but once equity is sold to Focus, the line of demarcation becomes clear, and compensation is a charge to margin. Our guess is that Focus’s profitability isn’t very different than we might expect from the affiliate firms on a stand?alone basis, or somewhere between 25% and 35%. If their EBITDA margin is around 30%, then Focus should be generating annual cash flow a bit north of $200 million.

Focus Valuation Metrics

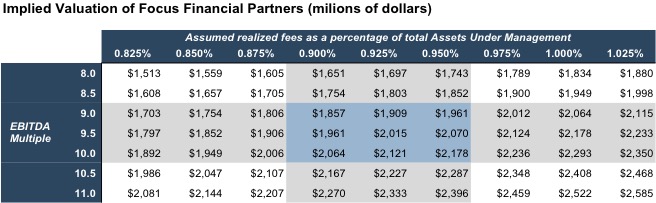

Reports suggest that the Stone Point / KKR recap valued Focus at around $2.0 billion. Given the performance metrics we’ve estimated above, that pricing implies an EBITDA multiple of between 9x and 10x, which makes sense to us and is more or less consistent with public market pricing, minus a modest discount.

Two weeks prior to the recap, firms like Legg Mason were trading at 12x EBITDA, with AMG at 14x. It is possible that Focus’s performance was a bit less than we estimate, and if fees realized were a bit shy of 90 basis points and/or if Focus’s EBITDA margin was closer to 25%, then a $2.0 billion valuation would require an EBITDA multiple of closer to 12x. However, we think it is unlikely that Stone Point and KKR paid a top-tic multiple for Focus; doing so would leave them with less upside at exit.

Selling to private equity is a lower risk transaction, which no doubt pressured the valuation. Accepting some discount enabled sellers to get out clean rather than sell some through an IPO and the rest over an SEC regulated timeline. Selling to private equity also allowed the parties to keep the ultimate terms and conditions of sale private. We think it is also unlikely, however, that the discount to public market pricing was much greater than 20% or so for Focus, because a bigger haircut would have induced Focus to consummate their IPO.

Are We There Yet?

Plenty has been written over the past two years about holding periods lengthening because ample private equity funding has diminished the liquidity advantage of public markets. The expense of being public and the disclosure requirements are off putting to many, and the flow of capital into the private equity community makes it much easier to keep companies like Focus out of the public markets. We watched enthusiasm for going public wane fifteen years ago with the dotcom bust and the advent of Sarbanes-Oxley. We would still suggest that no matter how long the private equity journey, the destination hasn’t changed. The PE community can only recycle investment ideas and investment dollars so many times – eventually Focus and other companies like it will have to go public. Even the Mille Miglia has a finish line.