RIA M&A Update: Q1 2024

Following a year where deal volume in the RIA industry nearly matched the all-time high of 2022, RIA M&A activity cooled in the first quarter of 2024. Fidelity’s March 2024 Wealth Management M&A Transaction Report listed 50 deals through March 2024, down 29% from the 70 deals executed during the same period in 2023.

![]()

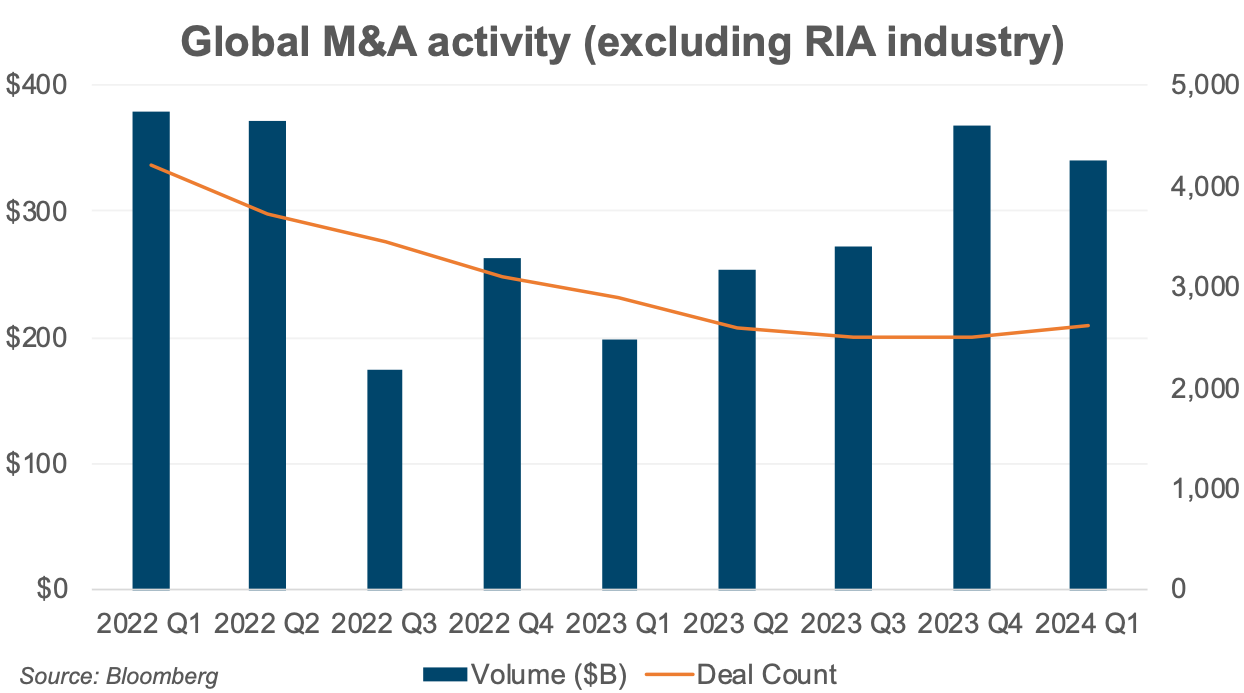

RIA deal activity experienced a greater decline than the broader M&A market. The number of M&A transactions for all industries (excluding the RIA industry) decreased 9% year-over-year through the first quarter of 2024 (per Bloomberg), compared to a decline of 29% in the RIA industry.

Despite the decline in the total number of deals, there was a significant uptick in total transacted AUM during 2024. Total transacted AUM through March 2024 was $139.2 billion—a 63% increase from the same period in 2023. The average AUM per transaction during the first quarter of 2024 was $2.8 billion, a 128% increase over the prior year. The increase in deal size has been an encouraging sign, given the rise in the cost of capital over the past two years. The growth in deal size resulted from the completion of several large transactions during the first quarter of 2024, coupled with the overall increase in AUM levels due to market performance.

Per Echelon’s RIA M&A Deal Report, “This elevated number of larger transactions, in light of buyers facing a higher cost of capital and economic uncertainty, demonstrates buyer resilience and likely indicates that $1BN+ deal activity will increase to 2021 levels or higher once macroeconomic headwinds, namely higher interest rates subside.”

Another contributor to the increase in deal size has been RIAs partnering with private equity firms. According to Fidelity’s March 2024 Wealth Management M&A Transaction Report, private equity backing was involved in 88% of the transactions in March. Per Echelon’s RIA M&A Deal Report,

“Another driver of deal size was the heightened creativity in deal structures, adopted by private equity firms seeking to get deals across the finish line in the face of higher borrowing costs. Structured minority investments, with features such as paid-in-kind and preferred distribution rights, have become more popular in the largest transactions, especially those involving sellers with more than $10 billion in assets.”

Noteworthy transactions backed by private equity include Caprock’s acquisition of Grey Street Capital, Mariner Wealth Advisor’s purchase of Fourth Street Performance Partners, and Hightower’s acquisition of Capital Management Group of New York.

The prevalence of serial acquirers and aggregators has continued in the RIA M&A market. In recent years, the professionalization of the buyer market and the entrance of outside capital have driven demand and increased competition for deals. Serial acquirers and aggregators have increasingly contributed to deal volume, supported by dedicated deal teams and access to capital. Such firms accounted for approximately 70% of transactions during the first quarter of 2024. Mercer Advisors, Miracle Mile Advisors, and Allworth Financial completed multiple deals during the fourth quarter.

Deal activity has also been supported by the supply side of the M&A equation, as the impetus to sell is often based on more than market timing. Sellers are often looking to solve succession issues, improve quality of life, and access organic growth strategies. Such deal rationales are not sensitive to the market environment and will likely continue to fuel the M&A pipeline even during market downturns.

What Does This Mean for Your RIA?

For RIAs planning to grow through strategic acquisitions: Pricing for RIAs has trended upwards in recent years, leaving you more exposed to underperformance. Structural developments in the industry and the proliferation of capital availability and acquirer models will likely continue to support higher multiples than the industry has seen. That said, a long-term investment horizon is the greatest hedge against valuation risks. Short-term volatility aside, RIAs continue to be the ultimate growth and yield strategy for strategic buyers looking to grow their practice or investors capable of long-term holding periods. RIAs will likely continue to benefit from higher profitability and growth than their broker-dealer counterparts and other diversified financial institutions.

For RIAs considering internal transactions: We’re often engaged to address valuation issues in internal transaction scenarios, where valuation considerations are top of mind. Internal transactions don’t occur in a vacuum, and the same factors driving consolidation and M&A activity have influenced valuations in internal transactions as well. As valuations have increased, financing in internal transactions has become a crucial secondary consideration where buyers (usually next-gen management) lack the ability or willingness to purchase a substantial portion of the business outright. As the RIA industry has grown, so too has the number of external capital providers who will finance internal transactions. A seller-financed note has traditionally been one of the primary ways to transition ownership to the next generation of owners (and, in some instances, may still be the best option). Still, an increasing amount of bank financing and other external capital options can provide selling partners with more immediate liquidity and potentially offer the next-gen cheaper financing costs.

If you are an RIA considering selling: Whatever the market conditions are when you go to sell, it is essential to have a clear vision of your firm, its value, and what kind of partner you want before you go to market. As the RIA industry has grown, a broad spectrum of buyer profiles has emerged to accommodate different seller motivations and allow for varying levels of autonomy post-transaction. A strategic buyer will likely be interested in acquiring a controlling position in your firm and integrating a significant portion of the business to create scale. At the other end of the spectrum, a sale to a patient capital provider can allow your firm to retain its independence and continue operating with minimal outside interference. Given the wide range of buyer models out there, picking the right buyer type to align with your goals and motivations is a critical decision that can significantly impact personal and career satisfaction after the transaction closes.

About Mercer Capital

We are a valuation firm that is organized according to industry specialization. Our Investment Management Team provides valuation, transaction, litigation, and consulting services to a client base consisting of asset managers, wealth managers, independent trust companies, broker-dealers, PE firms and alternative managers, and related investment consultancies.