The U.S. bond market is undergoing its worst bear market in decades. Barclays U.S. Aggregate Bond Market Index produced a total return of negative 14.5% through September 30, 2022 and negative 16.0% through November 8, 2022. Excluding coupon income, the year-to-date loss was 17.2% which speaks to how low coupon income is given the nominal difference between price change and total return.

Click here to expand the image above

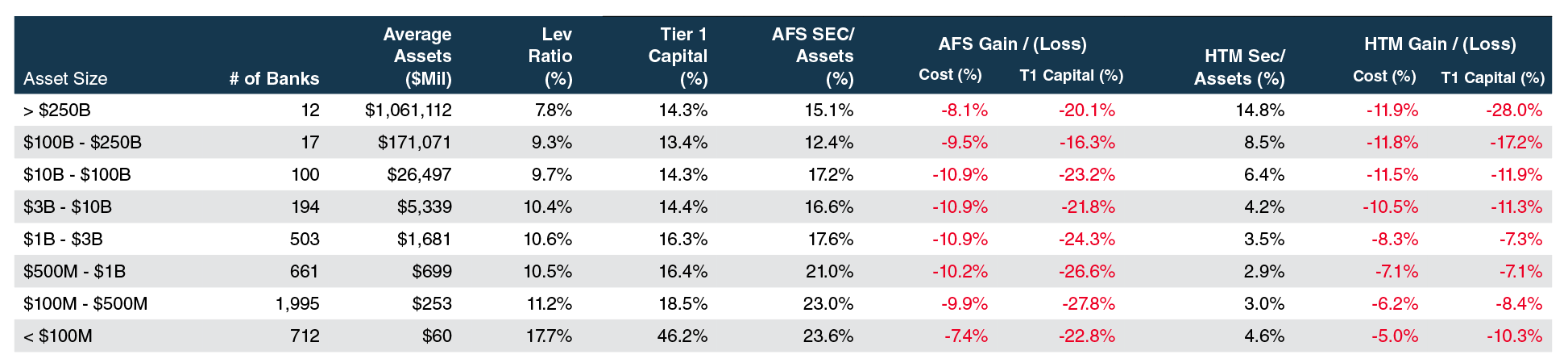

As shown in the figure below, U.S. commercial banks have suffered unrealized losses in their bond portfolios equal to roughly 10% of the cost basis of both AFS and HTM classified portfolios as of September 30, which compares to a price reduction of 15.6% in the Barclay’s index as of quarter end.

The less-worse performance by U.S. banks likely reflects less duration than the index, which has an effective duration of 6.25 years and weighted average maturity of 8.25 years. Our observation is that for the most part outsized losses among U.S. banks reflect an outsized position in municipals and/or MBS. The index composition is heavily skewed to U.S. Treasuries and U.S. Agency obligations given the heavy issuance of government backed debt the past 15 years or so.

While management and directors at most banks are unhappy with their bond portfolios, institutional investors have taken a more nuanced view of the impact of rising rates based upon the tenor of third quarter earnings calls and the reaction of most stocks upon the release of earnings. Rising rates have supported bank earnings even though fixed-rate loan and bond portfolios are slow to reprice as floating-rate loans have repriced and banks have lagged deposit rates.

Investor concern is more focused on liquidity risks. Some (or many) banks eventually may have to raise deposit rates sharply to stem outflows and/or fund loan growth because selling bonds is not a viable option given the magnitude of unrealized losses that if realized will reduce regulatory capital.

Our prior commentary on bank bond portfolios following the release of the first and second quarter Call Reports can be found here and here.