The petroleum industry was one of the first major industries to widely adopt the discounted cash flow (DCF) method to value assets and projects—particularly oil and gas reserves. These techniques are generally accepted and understood in oil and gas circles to provide reasonable and accurate appraisals of hydrocarbon reserves. When market, operational, or geological uncertainties become challenging, however, such as in today’s low price environment, the DCF can break down in light of marketplace realities and “gaps” in perceived values can appear.

While DCF techniques are generally reliable for proven developed reserves (PDPs), they do not always capture the uncertainties and opportunities associated with the proven undeveloped reserves (PUDs) and particularly are not representative of the less certain upside of possible and probable (P2 &P3) categories. The DCF’s use of present value mathematics deters investment at low ends of pricing cycles. The reality of the marketplace, however, is often not so clear; sometimes it can be downright murky.

In the past, sophisticated acquirers accounted for PUDs upside and uncertainty by reducing expected returns from an industry weighted average cost of capital (WACC) or applying a judgmental reserve adjustments factor (RAF) to downward adjust reserves for risk. These techniques effectively increased the otherwise negative DCF value for an asset or project’s upside associated with the PUDs and unproven reserves.

At times, market conditions can require buyers and sellers to reconsider methods used to evaluate and price an asset differently than in the past. In our opinion, such a time currently exists in the pricing cycle of oil reserves, in particular to PUDs and unproven reserves. In light of oil’s low price environment, coupled with the forecasted future price deck, many—if not most—PUDs appear to have a negative DCF value.

In the past, we have analyzed actual market transactions to show that buyers still pay for PUDs and unproven reserves despite a DCF that results in little or no value. In today’s market, however, asset transactions of “non-core assets” indicate zero value for all categories of unproven reserves. A highlighted example of this is Samson Oil and Gas’s recent purchase of 41 net producing wells in the Williston Basin in North Dakota and Montana. The properties produce approximately 720 BOEPD and contain estimated reserves of 9.5 million barrels of oil equivalent. Samson paid $16.5 million for the properties in early January 2016 and estimates that within five years they can fund the drilling of PUDs. Samson’s adjusted reserve report, using the most current market commodity prices, indicated PDP reserves worth $15.5 million, PDNPs worth $1 million and PUDs worth $35 million—a total of $52 million in reserves present valued at 10%. This breakdown indicates dollar for dollar value was given on the PDP and PDNP reserves, but zero cash value given on the PUDs.

Is this transaction the best indication of fair market value or fair value?

We believe there is a convincing argument to be made that the Samson transaction and a handful of other asset deals in the previous six months are not the best indication of asset value. In short, these sales could be categorized as distressed or “fire sale” transactions for the following reasons:

In this low price environment, buyers don’t have to blink first. These factors indicate that some companies may feel pressure to lower their asking prices to levels that continuously attract bidders. The market looks distressed.

What does this mean for the fair market value/fair value of oil and gas assets? The definitions of fair market value and fair value require buyers and sellers to operate in a “distress-free” environment. When the marketplace is not distress-free, perhaps non-market methods should be utilized to estimate the real value of PUDs and unproven reserves. In these scenarios, one useful method to price these assets is the use of option theory.

If one solely relied on the market approach, it appears much of these unproven reserves would be deemed worthless. Why then, and under what circumstances, might the unproven reserves have significant value?

The answer lies within the optionality of a property’s future DCF values. In particular, if the acquirer has a long time to drill, one of two forces come into play: either (1) the current price outlook can change radically for a resource, and subsequently alter the PUDs or (2) drilling technology can change, such as the onslaught of hydraulic fracturing, and the unproven reserves accrue significant DCF value.

This optionality premium or valuation increment is typically most pronounced in unconventional resource play reserves, such as coal bed methane gas, heavy oil, or foreign reserves. This is additionally pronounced when the PUDs and unproven reserves are held by production. These types of reserves do not require investment within a fixed short timeframe.

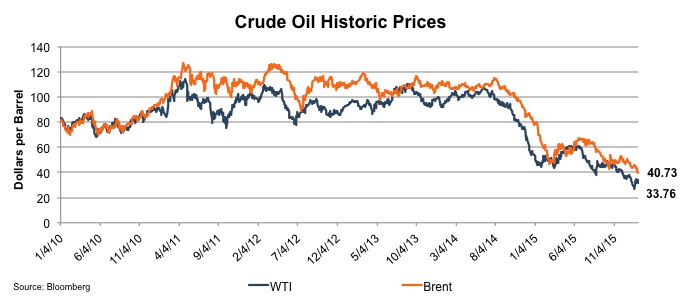

One of the primary challenges for industry participants when valuing and pricing oil and gas reserves is addressing PUDs and unproven reserves. As oil prices have dropped over 50% in the last six months, reaching 12 year lows, it should be anticipated that PUD values may drop from 75 cents on the dollar to 20 cents on the dollar or less. After the Great Recession, some PUDs faced a similar, yet more modest, decline in price. The price level recovery for PUDs in 2011 was partly attributable to the recovery in the U.S. and global economies, and partly due to increases in the price of oil.

Five main factors have significantly increased the world supply of oil and driven down prices:

In August of 2015, it was estimated that Iran’s return to the global oil market would add approximately one million barrels of oil a day to the market and decrease the price of oil by $10 per barrel. Iran is currently ready to increase exports by half a million barrels of oil per day, and the fear of further over-supply pushed the price of oil below $30 on Friday, January 15. Now, the question is when will oil prices recover? The Chief of the IEA estimated that oil prices will recover in 2017. Prices are predicted to remain low in 2016 as expected demand for oil is growing at lower rates than in the past thanks to economic slowdowns in China, India, and Europe. However, the growth in oil supply is predicted to slow in 2017 as the current cuts in research and development catch up with many exploration and production companies. We must also remind ourselves of the crash in oil prices in 1985 that remained below $20 until 2003.

As previously mentioned, PUDs are typically valued using the same DCF model as proven producing reserves after adding in an estimate for the capital costs (capital expenditures) to drill. Then the pricing level is adjusted for the incremental risk and the uncertainty of drilling “success,” i.e., commercial volumes, life and risk of excessive water volumes, etc. This incremental risk could be accounted for with either a higher discount rate in the DCF, a RAF or a haircut. Historically, in a similar oil price environment as we face today, a raw DCF would suggest little or no value for the PUDs or unproven reserves. Interestingly, market transactions with similar reserves (i.e., with little or no proven producing reserves) have demonstrated significant amounts attributable to non-producing reserves, thus demonstrating the marketplace’s recognition of this optionality upside.

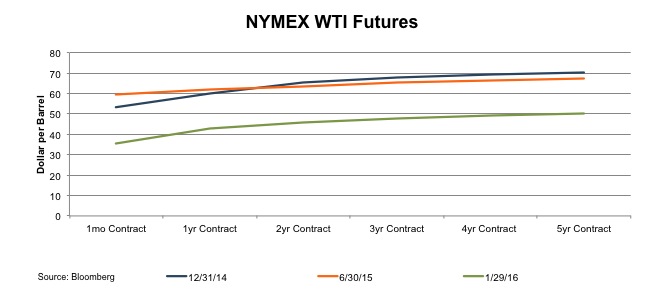

Studies have shown that NYMEX futures are not a very accurate predictor of the future, and yet buyers are estimating the value of this option into the prices they are willing to pay. When NYMEX forecasts $35 per barrel, it could actually be $45 when that future date rolls around.

So what actions do acquirers take when values are out of the money in terms of drilling economic wells? Why do acquirers still pay for the non-producing and seemingly unprofitable acreage? Experienced dealmakers realize that the NYMEX future projections amount to informed speculation by analysts and economists which many times vary widely from actual results. Note in the chart above how much the future forecasted prices changed in only one year.

In practice, undeveloped acreage ownership functions as an option for reserve owners; therefore, an option pricing model can be a realistic way to guide a prospective acquirer or valuation expert to the appropriate segment of market pricing for undeveloped acreage. This is especially true at the bottom of the historic pricing range occurring for the NG commodity currently.

This technique is not a new concept as several papers have been written on this premise. Articles on this subject were written as far back as 1988 or perhaps further, and some have been presented at international seminars.

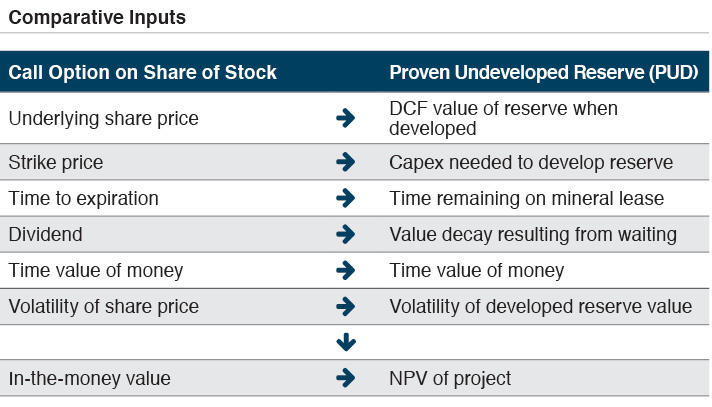

The PUD and unproved valuation model is typically seen as an adaptation of the Black Scholes option model. An applicability signal for this method is when the owners of the PUDs have the opportunity, but not the requirement, to drill the PUD and unproven wells and the time periods are long, i.e. five to 10 years. The value of the PUDs thus includes both a DCF value, if applicable, plus the optionality of the upside driven by potentially higher future commodity prices and other factors. The comparative inputs, viewed as a real option, are shown in table below.

There are, of course, key differences in PUD optionality and stock options as well as limitations to the model. Amid its usefulness, the model can be challenging to implement. Below are some areas in particular where keen rigorous analysis can be critical:

The availability of drilling resources tends to decline while the costs of drilling and oilfield services tend to rise, often precipitously, when oil and gas prices rise. These factors can present an oscillating delta in both cost and timing uncertainties as the marketplace responds by investing capital into underdeveloped reserves while the fuse burns on existing lease rights. The time value of an option can increase significantly if (1) the mineral rights are owned; (2) unconventional resource play reserves are included; (3) there are foreign reserves; or (4) the reserves are held by production. In these instances, the PUD and unproved reserve option to drill can be deferred over many years, thereby extending the option.

Utilization of modified option theory is not in the conventional vocabulary among many oil patch dealmakers, but the concept is clearly implicitly considered (as evidenced in many market transactions). This application of option modeling becomes most relevant near the bottom of historic cycles for a commodity. Here, the DCF will often yield little or no value even though transactions are being made for substantial values, thereby validating our belief that option theory is being utilized in the marketplace either directly or indirectly. If the right to drill can be postponed an extended period of time, i.e. five to ten years, the time value of those out of money drilling opportunities can have significant worth in the marketplace.

We caution, however, that there are limitations in the model’s effectiveness. Black Sholes’ inputs do not always capture some of the inherent risks that must be considered in proper valuation efforts. Specific and careful applications of assumptions are musts. Nevertheless, option pricing can be a valuable tool if wielded with knowledge, skill, and good information, providing an additional lens to peer into a sometimes murky marketplace.

Mercer Capital has significant experience valuing assets and companies in the energy industry, primarily oil and gas, bio fuels and other minerals. Contact a Mercer Capital professional today to discuss your valuation needs in confidence.