The August 2019 BankWatch described key considerations in analyzing the financial statements of banks. However, we did not address one crucial set of relationships – those between a bank holding company (“BHC”) and its subsidiary depository institution.

Most banks are owned by bank holding companies. While investors often state that they own an interest in a bank, this may not be legally precise. Usually, they own a share of stock in a bank holding company, which in turn owns a controlling interest in a subsidiary bank’s common stock. Where a bank holding company exists, this entity’s common stock generally is the subject of valuation analyses.

Part 3 of the Community Bank Valuation series explores important relationships between banks and their holding companies, focusing particularly on cash flow and leverage.

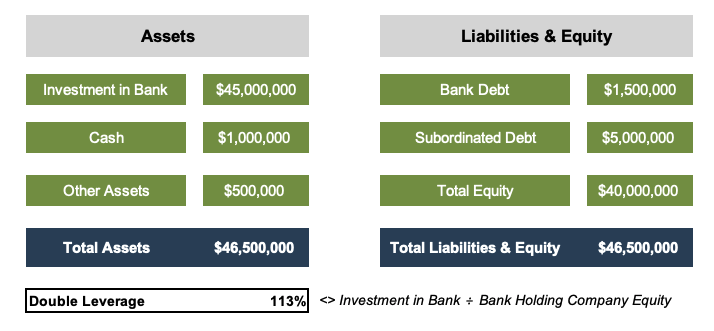

Compared to a bank’s balance sheet, a holding company’s balance sheet has fewer moving parts. The “left side” of its balance sheet, or its assets, usually is rather boring. The more intriguing analytical question, though, is how the bank holding company finances its investment in the bank. The following table presents a balance sheet for a BHC controlling 100% of the common stock of a bank with $500 million of total assets.

Usually, the holding company’s assets consist virtually entirely of its investment in its subsidiary bank or banks, which equals the bank’s total equity. The investment in the bank is carried at equity, meaning that it increases by the bank’s net income and decreases by dividends paid from the bank to the holding company, among other transactions. Other material assets may include:

Interestingly, BHCs can borrow from banks – just not their bank subsidiary – and other capital providers. If the funds are downstreamed into the bank, the borrowings can be transformed from an instrument not includible in the BHC’s regulatory capital into Tier 1 capital at the bank. In order of seniority these funding sources include:

A BHC’s equity usually consists almost entirely of common stock, which generally must be the principal form of capitalization under BHC regulations. However, BHCs can issue preferred stock, and regulations view most favorably non-cumulative, perpetual preferred stock.

Why do holding companies exist? First, they provide an efficient way to raise funds that can be injected as capital into the bank, thereby accommodating its organic growth. Second, they can facilitate acquisitions. Third, BHCs can more efficiently conduct shareholder transactions, such as repurchases.

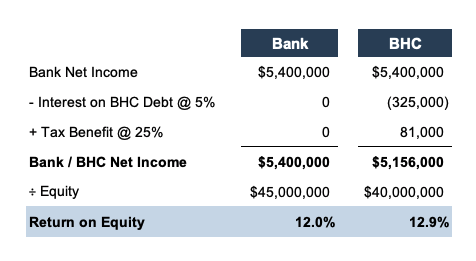

By using leverage, a BHC can enhance the bank’s stand-alone return on equity (or exacerbate the ROE pressure arising from adverse financial scenarios). As indicated in Table 2, BHC leverage magnifies the subsidiary bank’s 12.0% ROE to 12.9% after considering the cost of the BHC’s debt.

As for a non-financial company, too much leverage can mean that the beneficial effect to shareholders of a higher ROE is swamped by the additional risk of financial distress. Various metrics exist to measure the holding company’s leverage, but one is the “double leverage” ratio, which is calculated as the investment in the bank subsidiary divided by the BHC’s equity. As indicated in Table 1 on page one, the BHC’s ratio is 113%, which is consistent with the median reported by all smaller BHCs at June 30, 2019 (112%, excluding some BHCs for which the BHC’s equity exceeds the bank investment).

Unfortunately, BHC regulatory filings and audited financial statements do not provide a sources and uses of funds schedule, although some cash flow data is provided. Nevertheless, understanding the BHC’s obligations, and the cash required to service those obligations, is essential.

Sources of funds consist principally of the following:

Uses of funds include the following:

Analysts should compare a bank’s ability to pay dividends, given its profitability level and need to retain earnings to fund its growth, against the BHC’s various claims on cash. Mismatches can sometimes arise due to changes in the bank’s performance or operating strategy. For example, consider a BHC that historically has paid high dividends to shareholders. If its subsidiary bank adopts a new strategic plan focused on organic growth, then the bank will need to retain earnings rather than pay dividends to the BHC and, ultimately, BHC shareholders. Additional borrowings could fund a short-term gap, but this is not a long-term solution to a BHC cash flow mismatch.

Two other special circumstances arise when analyzing BHC cash flow:

Capital requirements for BHCs vary based upon their asset size. Under current regulations, BHCs with assets below $3.0 billion are subject to the Federal Reserve’s Small Bank Holding Company Policy Statement. This regulation does not establish any specific minimum capital ratios for small BHCs; however, a debt/ equity ratio limitation exists for debt arising from acquisitions. Therefore, small BHCs have significant flexibility in managing their capital structure, although the Federal Reserve theoretically remains a check on their creativity.

Large BHCs are subject to the Basel III regulations, which involve capital ratios calculated based on Tier 1 and total capital. Tier 1 capital generally is limited to common equity, non-cumulative perpetual preferred stock, and grandfathered TruPS. In addition to the allowance for loan losses, Tier 2 capital may include subordinated debt. Large BHC management can balance these capital sources to minimize the BHC’s weighted average cost of capital, maintain flexibility for unexpected events or opportunities, and ensure compliance with regulatory expectations.

While the subsidiary bank receives most of the analytical attention, the holding company on a standalone (or parent company) basis should not be overlooked. This is particularly true if the holding company has significant obligations to service debt or pay other expenses. By understanding the linkages between the bank and holding company, analysts can better assess a BHC’s potential future returns to shareholders and risk factors posed by the BHC that could jeopardize those returns.

Originally published in Bank Watch, September 2019.