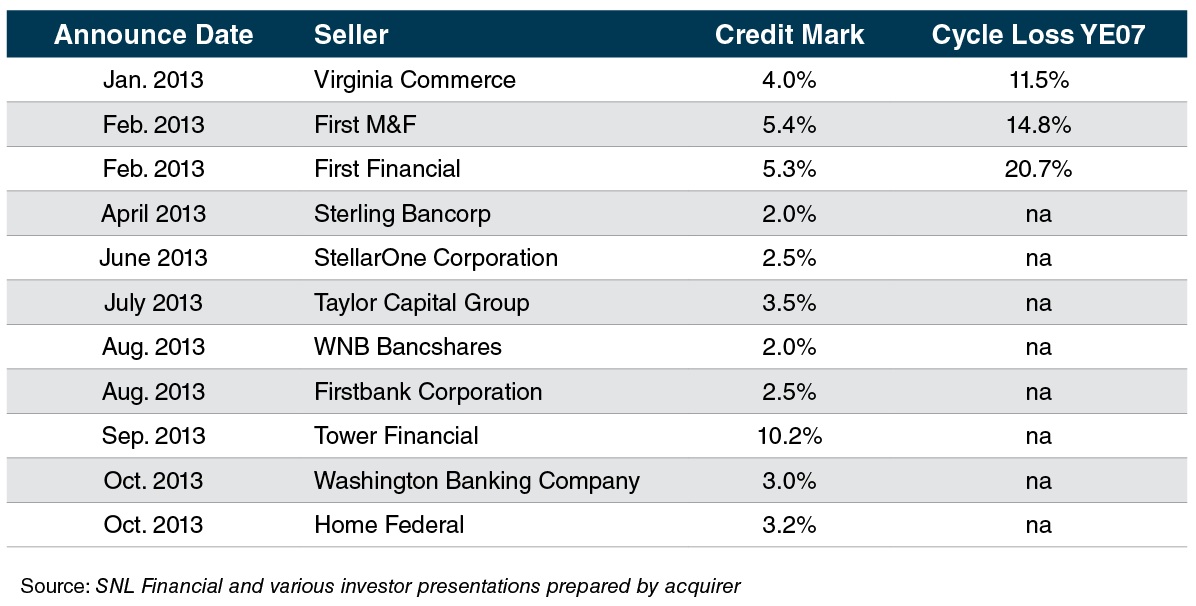

Merger related accounting issues for bank acquirers are often complex. In recent years, the credit mark on the acquired loan portfolio has often been cited as an impediment to M&A activity as this mark can be the most critical component that determines whether the pro-forma capital ratios are adequate. As economic conditions have improved in 2013, bank M&A activity has also picked up and we thought it would be useful to take a look at the estimated credit marks for some of the larger deals announced in 2013 (i.e., where the acquirer was publicly traded and the reported deal values were greater than $100 million) to see if any trends emerged.

As detailed below, the estimated credit marks declined during 2013 with only one deal reporting a credit mark larger than 4% after the first quarter of 2013 compared to all deals being in excess of 4% in the first quarter of 2013. The reported estimated credit marks for 2013 were also generally below those reported in larger deals in 2010, 2011, and 2012 when the estimated credit marks were often in excess of 5%.

This trend reflects a number of factors including most notably:

Mercer Capital has provided a number of valuations for potential acquirers to assist with ascertaining the value and estimated credit mark of the acquired loan portfolio. In addition to loan portfolio valuation services, we also provide acquirers with valuations of other financial assets and liabilities acquired in a bank transaction, including depositor intangible assets, time deposits, and trust preferred securities.

Feel free to give us a call to discuss any valuation issues in confidence as you plan for a potential acquisition.