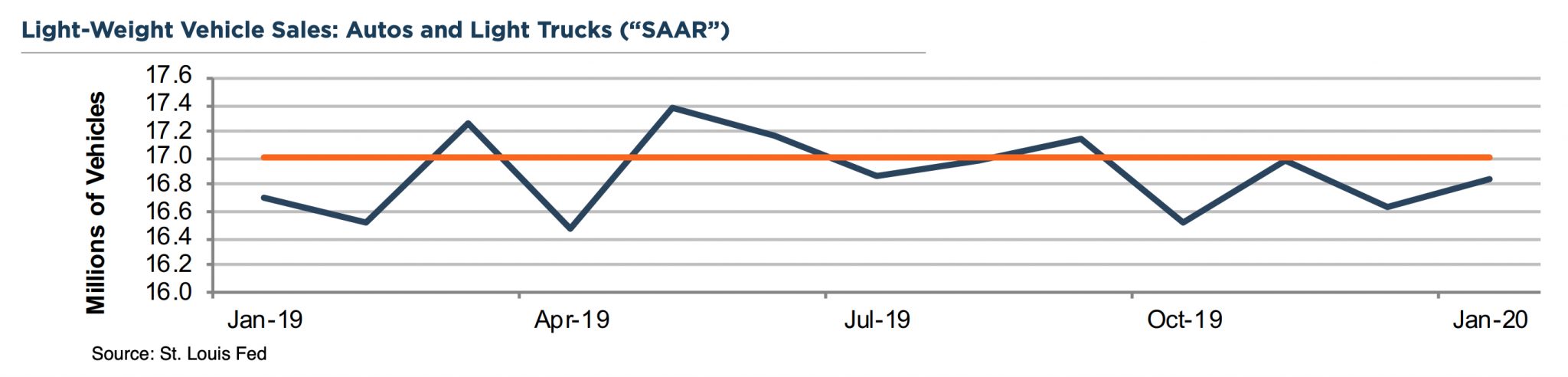

SAAR came in at 16.844 million for January 2020, up about 1% from both the prior month and the prior year. Actual sales of 1.13 million units was slightly down from January 2019. Similarly, while SAAR was up from last month, sales volume was down 25% from December. However, this is the reason the auto industry seasonally adjusts, as dealers offer significant discounts (e.g. Toyota-thon and Happy Honda-Days) at year-end. In each of the past ten years, the month of December has had higher than average sales volume, whereas January and February have each had below average. October and November are also below average, as consumers anticipate falling prices. Incentives reached all-time highs in December at $4,600 per vehicle, while January’s figure dropped to $4,000 as dealers clear out 2019 model year inventory. As seen above, SAAR has been below 17 million more often than not in the past year.

NADA maintained their 2020 sales expectation of 16.8 million units. This was higher than forecasts provided by Asbury Automotive Group and Group 1 Automotive of 16.5 million and 16.7 million, respectively. As unit volume is expected to drop below the 17 million threshold for the first time since 2014, public company executives are distancing their companies from this metric. We listened to Q4 earnings calls for three of the public auto dealers (Group 1, Penske, and Asbury) within the past two weeks, and all three highlighted common themes to increased profitability.

“Our Service and Parts operation throughout the organization provide recurring revenue which generates 46% of our company gross profit. We continue to demonstrate that PAG’s business model is much more than monthly new vehicles sales or the SAAR.” – Roger Penske, Chairman and CEO of Penske Automotive Group

“We were able to achieve record adjusted net income […] by concentrating on areas of the business where we exert greater control: used vehicles, parts and service, F&I, and cost.” – Earl Hesterberg, President and CEO of Group 1 Automotive