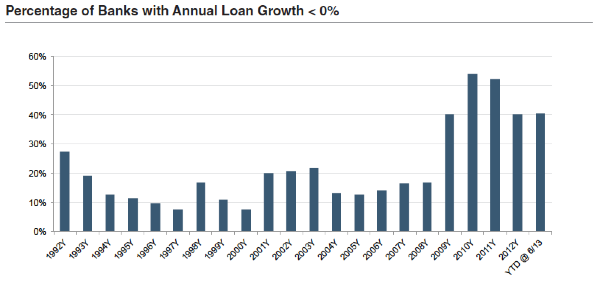

Loan growth continues to remain a struggle for community banks as loan demand remains weak in most regions. Based on Call Report data as of June 30, 2013 for approximately 3,750 banks with assets between $100 million and $5 billion, more than 50% of banks reported lower loan balances in 2010 and 2011. In 2012 and year-to-date in 2013, approximately 40% of banks have reported lower loan balances.

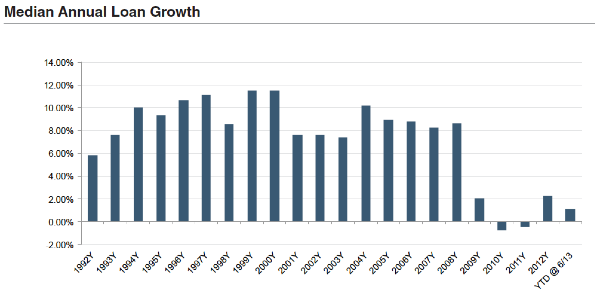

Community banks as a group reported negative median loan growth in 2010 and 2011. Beginning in 2012, loan growth resumed, with the community bank group examined realizing median growth of 2.2%. Year-to-date through June 2013, median growth was 1.1%, or 2.2% annualized, on pace with the 2012 growth figure. The low level of growth in loan portfolios is well below the historical average, including prior recessions. During the 2001-2002 recession, for example, median loan growth was approximately 7.5% for the community bank sample.

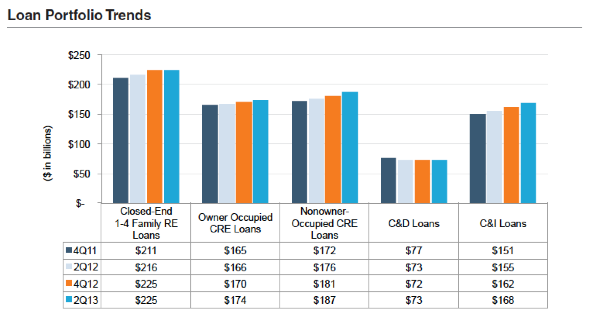

The modest loan growth realized in 2012 and year-to-date in 2013 has been spread across portfolio sectors, with all non-agricultural loan categories up 6.8% at June 30, 2013 from year-end 2011. Within the non-ag categories, 1-4 family mortgages were up 6.4%, CRE loans were up 7.4% with most of the increase in nonowner-occupied CRE loans, and commercial/industrial loans were up 11.3%. Construction and development credits were the only sector that saw declines in the last 18 months, with total C&D loans down 4.9% from year-end 2011.

An analysis of mortgage data by SNL Financial indicates that residential loan growth has been consistent across the country, with 932 of the 955 metro areas with available data reporting increases in originations.1 The analysis by SNL looks at comprehensive data filed by lenders pursuant to the Home Mortgage Disclosure Act for the 2012 fiscal year. The analysis shows the largest increases in mortgage lending activity in the areas that were hardest-hit by the recession, including Orlando, Phoenix, Las Vegas, Detroit, and Sacramento, which all posted growth in mortgage lending over 75% in 2012. Overall, funded mortgage loan volume was up 43% from 2011, increasing from $1.5 trillion to $2.1 trillion for the metro areas included in the data set.

For the community bank sample, total growth in single-family mortgages was slower than the aggregate mortgage data for all institutions, with loan volume up 6.5% for the 2012 fiscal year, indicating that the majority of loan growth, at least in the residential mortgage sector, was led by larger institutions.

1 “Loan Growth Spanned Entire US in 2012,” by Sam Carr and Fox, Zach. Published by SNL Financial, October 3, 2013.