I recently attended the 2019 Spring Conference of the National Auto Dealers Counsel (NADC) in Dana Point, California. This article provides a couple of key takeaways from the day and a half sessions on the current conditions in the industry.

Car subscription services are becoming a popular alternative to leasing. Each service varies in structure and is operated by dealers, manufacturers, and third parties. Some offer reasonable traditional leases or allow customers to make monthly payments, but allow more flexibility/frequency in swapping vehicles for changing preferences and needs.

Some manufacturers are only initially offering subscription services regionally, or in specific markets (BMW and Mercedes-Benz are offering vehicle subscription services in the Nashville market).

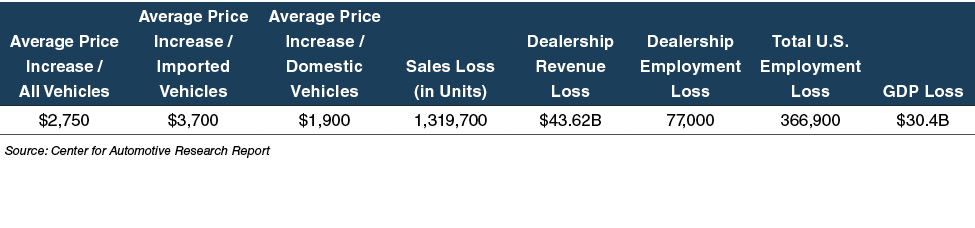

There has been a lot of talk in the news recently about impending tariffs in the auto dealer industry. Many unknowns and questions remain—Will President Trump enact tariffs? How will they affect the auto industry?

The Center for Automotive Research Report has compiled statistics to show the likely effects of tariffs on new/ used vehicle pricing, estimated losses for dealers, and projected employment and GDP loss (as seen below). With so much at stake, the auto dealer industry will keep a close eye on monitoring any new developments.

Amid the many changes that have resulted from the recent tax reform (the Tax Cuts and Jobs Act (TCJA)), here are a few directly impacting the auto dealer industry:

Originally published in the Value Focus: Auto Dealer Industry Newsletter, Year-End 2018.