The other significant industry news from the first quarter was the $1.05 billion equity investment in New York Community Bank (NYSE: NYCB) by an investor group led by former Secretary of the Treasury Steve Mnuchin. The investment was necessary to boost loss absorbing capital and to shore up confidence to stem a possible deposit run after its share price collapsed during February following a surprise fourth quarter loss that was later revised higher for a $2.4 billion goodwill write-off.

The initially reported 4Q23 loss of $252 million was not catastrophic, especially considering the company reported net income of $2.4 billion excluding the goodwill write-off as a result of the bargain gain from the purchase of the failed Signature Bank; however, the fourth quarter loss that arose from a $538 million provision for loan losses highlighted investor concerns about NYCB’s sizable exposure to NYC rent-controlled apartments and offices.

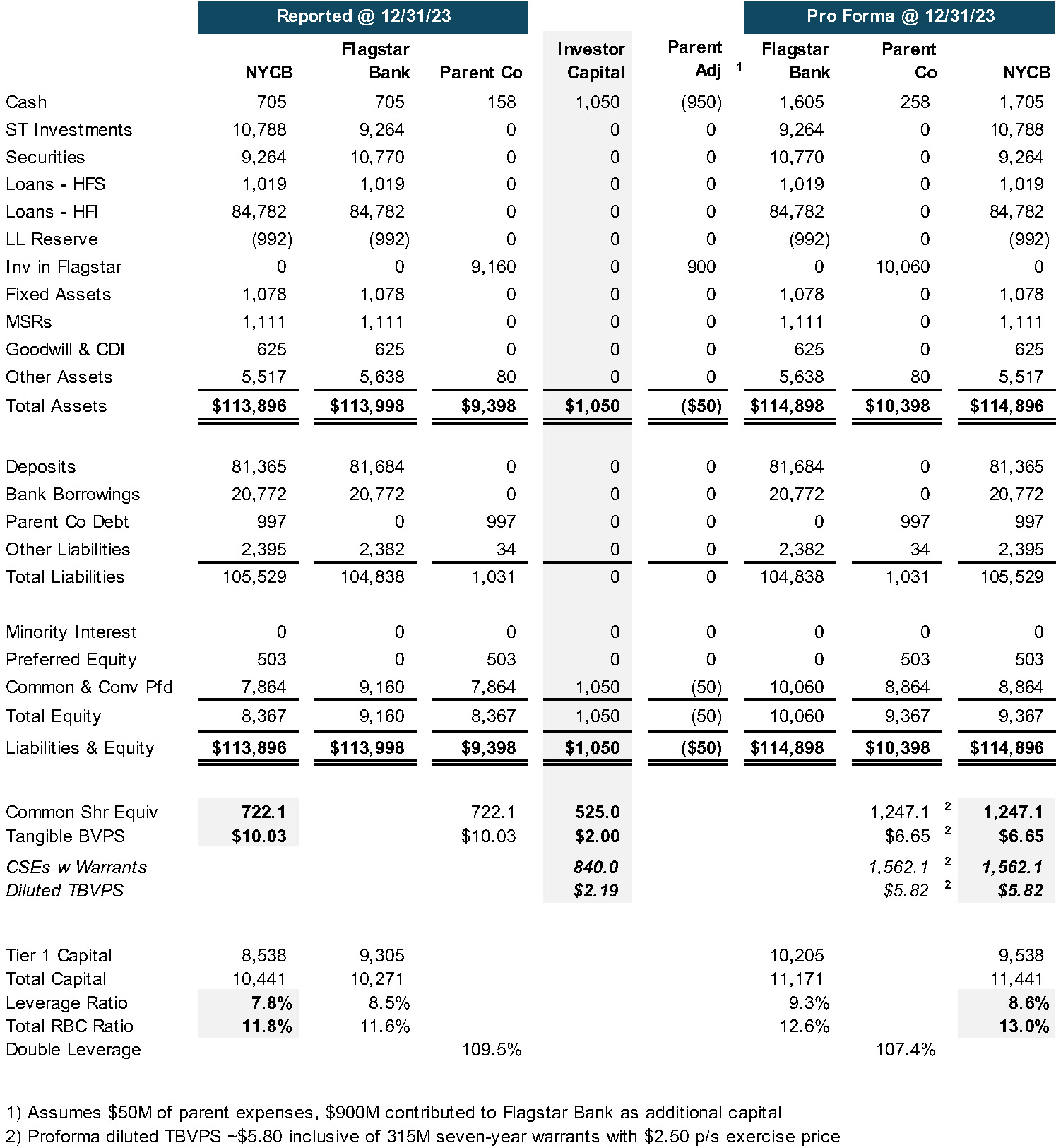

The figure on the right presents our proforma analysis of the transaction and its impact on the consolidated company (NYCB), the parent company in which the group invested, and wholly owned Flagstar Bank, N.A. The adage that capital is exorbitantly expensive if available at all when it must be raised comes to mind here with NYCB.

Source: Mercer Capital, NYCB SEC filings, and S&P Global Market Intelligence

We note the following:

Our additional thoughts on the transaction can be found HERE, and a link to NYCB’s investor deck announcing the transaction can be found HERE.

If we can assist your board with a capital raise or other significant transaction, please call us.