Although successful bank acquisitions largely hinge on deal execution and realizing expense synergies, properly assessing and pricing credit represents a primary deal risk. Additionally, the acquirer’s pro forma capital ratios are always important, but even more so in a heightened regulatory environment and merger approval process. Against this backdrop, merger-related accounting issues for bank acquirers have become increasingly important in recent years and the most significant fair value mark typically relates to the determination of the fair value of the loan portfolio.

Fair value is guided by ASC 820 and defines value as the price received/paid by market participants in orderly transactions. It is a process that involves a number of assumptions about market conditions, loan portfolio segment cash flows inclusive of assumptions related to expected credit losses, appropriate discount rates, and the like. To properly evaluate a target’s loan portfolio, the portfolio should be evaluated on its own merits, but markets do provide perspective on where the cycle is and how this compares to historical levels.

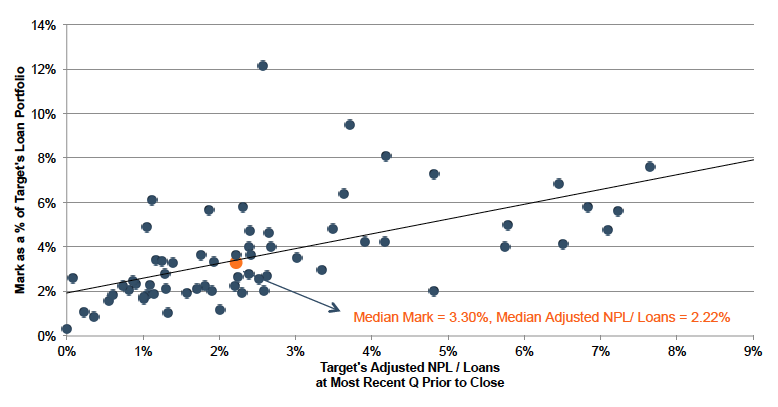

We reviewed fair values of recently announced community bank deals to determine if any trends emerged. As detailed in Figure 1, the fair value mark (i.e., the discount based on the estimated fair value compared to the reported gross loan balance) in recent deals appears to increase as the level of problem assets increases. However, the range remains quite wide and rarely hits the trendline, which could partially reflect the unique nature of isolated community bank loan portfolios. Overall, the median fair value mark observed was 3.30% while the median level of adjusted non-performing loans (as a percentage of loans) was 2.22%.

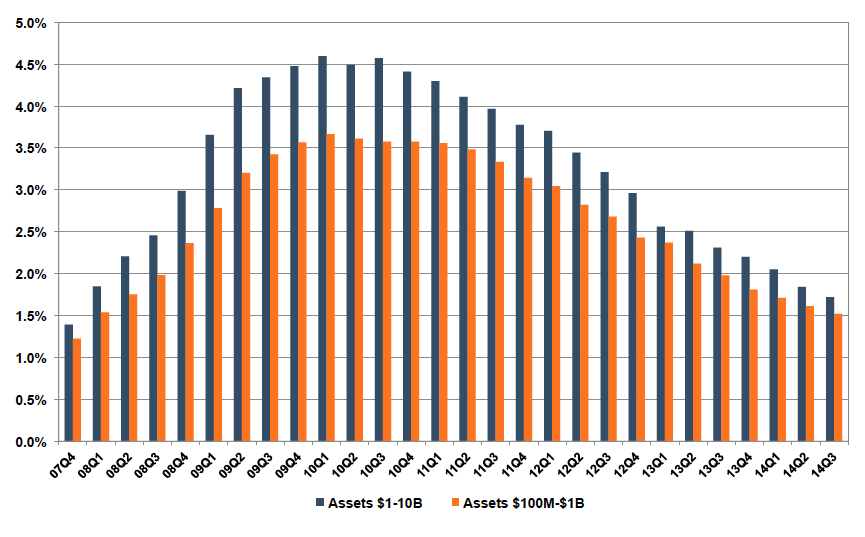

The recent fair value marks were generally below those reported in deals during (2008-2010) and immediately after the financial crisis (2010-2012). This trend reflects a number of factors including:

Mercer Capital has provided a number of valuations for potential acquirers to assist with ascertaining the fair value of acquired loan portfolio. In addition to loan portfolio valuation services, we also provide acquirers with valuations of other financial assets and liabilities acquired in a bank transaction, including depositor intangible assets, time deposits, and trust preferred securities. Feel free to give us a call or email to discuss any valuation issues in confidence as you plan for a potential acquisition.

Reprinted from Bank Watch February 2015.