Over the past three decades, community and regional banks have scaled back consumer lending while large banks and specialty finance companies have captured significant market share through economies of scale and robust origination platforms. Firms like American Express (NYSE:AXP), Capital One (NYSE:COF), Synchrony Financial (NYSE:SYF), and Ally Financial (NYSE:ALLY) leverage FDIC-insured deposit funding to power their lending operations. Most of these players, along with acquired entities like Discover Financial, operate at the intersection of payments and credit. Visa (NYSE:V) and Mastercard (NYSE:MC) are important payment partners to traditional banks, however.

Since the GFC ended in 2009, fintech has transformed consumer credit and payments, intensifying competition for banks and expanding credit access, particularly for subprime and near-prime borrowers. Fintech lenders such as OppFi (NYSE:OPFI), Enova (NYSE:ENVA), and Oportun (NASDAQGS:OPRT) have carved out niches by using data-driven underwriting and digital delivery to serve underserved markets.

BNPL providers like Affirm Holdings (NASDAQGS:AFRM), Klarna (NYSE:KLAR), and Sezzle (NASDAQCM:SEZL) have further reshaped the landscape, offering easy payment options to consumers while boosting merchant sales. Established players like PayPal (NASDAQGS:PYPL) and Block (NYSE:SQ) have also embraced BNPL, with Block’s Afterpay and Cash App exemplifying a broader mission to democratize financial services.

The operating environment for these companies has been favorable this year because funding is relatively easy with wide open capital markets; the Trump Administration has virtually dismantled the CFPB and borrowing costs are declining with Fed rate cuts. In 2023, funding was difficult in the wake of SVB’s failure (e.g., Affirm struggled to complete one or more securitizations), and the CFPB under the Biden Administration presented a challenging regulatory environment.

Post-Dodd-Frank, many banks retreated from small-dollar and unsecured lending due to heightened compliance costs and regulatory scrutiny, which diminished the appeal of these products. Fintechs filled the gap, leveraging technology to serve subprime and near-prime consumers. Companies like OppFi paired underserved borrowers with credit products through digital channels, often via partnerships with small banks.

Using alternative data, machine-learning underwriting, and payroll-linked repayment models, these firms positioned themselves as modern alternatives to payday loans and credit cards. BNPL providers like Affirm and Klarna followed suit, offering short-term, interest-free or low-interest installment plans that gained traction amid post-COVID e-commerce growth.

In recent years, the distinction between banks, fintech lenders and payments has blurred somewhat. Block’s company description captures this from a portfolio perspective:

Block builds technology to increase access to the global economy. Each of our brands unlocks different aspects of the economy. Square makes commerce and financial services accessible to sellers. Cash App is the easy way to spend, send, and store money. Afterpay is transforming the way customers manage their spending. TIDAL is a music platform that empowers artists. Bitkey is a simple self-custody wallet built for bitcoin. Proto is a suite of bitcoin mining products and services. Together, we’re helping build a financial system that is open to everyone.

For fintech lenders offering “lending as a service,” access to low-cost, stable deposit funding and perhaps greater regulatory certainty remains a coveted advantage of traditional commercial banking. Some have accessed bank funding. LendingClub acquired Radius Bank in 2021 to become a bank, and SoFi’s 2022 charter has bolstered its funding advantage. Others, like OppFi, rely on FDIC-insured bank partners to originate loans while retaining servicing or purchasing receivables.

Banks’ deposit-funded models offer a structural edge, especially after recent rate-driven deposit repricing while most fintechs and BNPL providers remain heavily dependent on capital markets and alternative lenders. Regulatory scrutiny, particularly of “rent-a-bank” partnerships, adds further complexity.

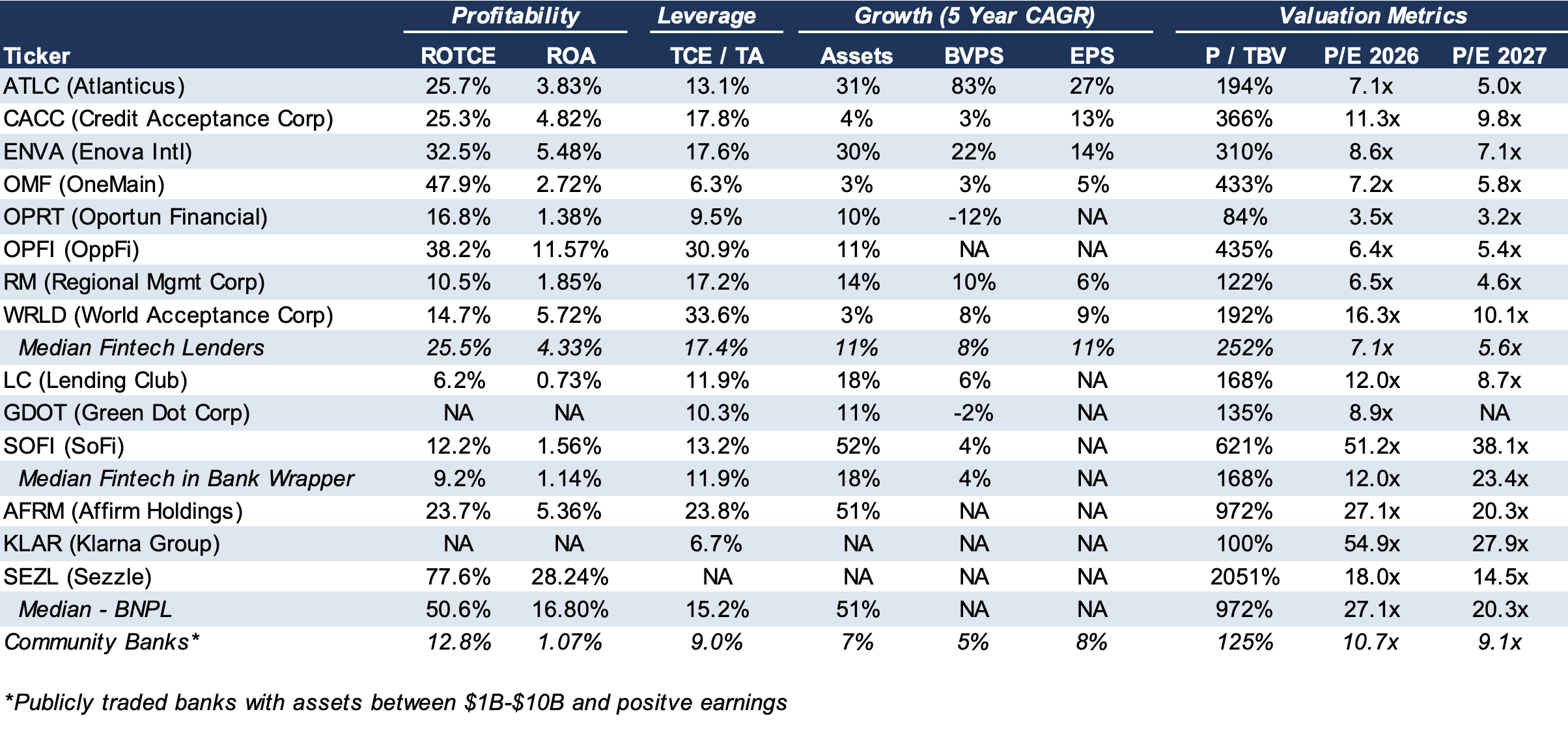

We are struck by the similarities and dissimilarities between banks and fintech lenders. Multiples are heavily influenced based upon investor perceptions of earnings growth (or free cash flow/excess capital) and risk (funding, compliance and credit). Overlaid are questions about the role of BNPL in providing incremental credit to subprime consumers and thereby sustaining consumer spending as student loan deferral end.

Valuations reflect these dynamics to some extent whereby lower growth implies lower earnings multiples for banks vs. fintech/BNPL whereas less funding and arguably regulatory risk translates to higher relative multiples. Perhaps the two big multiple determinants roughly offset between banks and the new economy lenders.

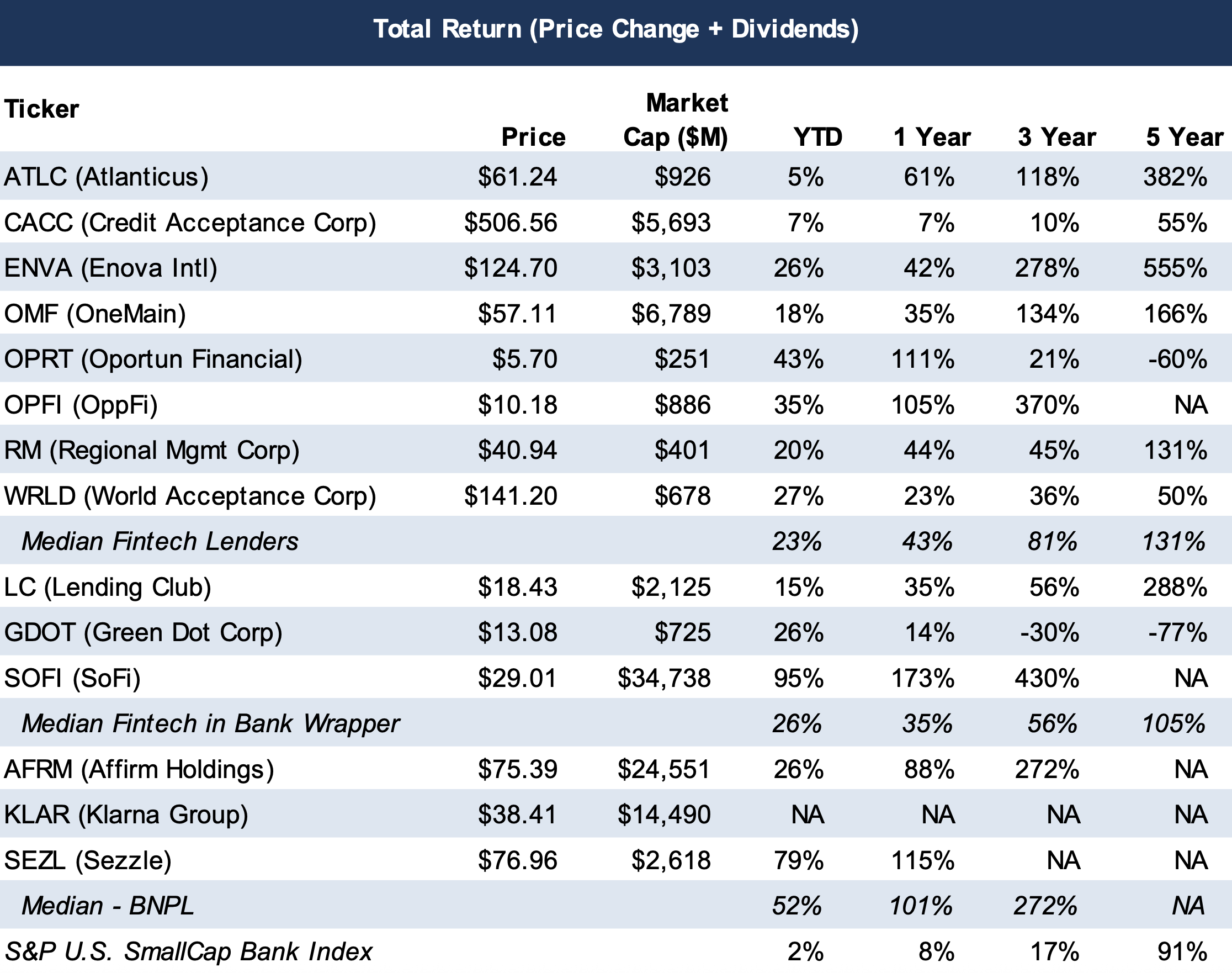

As of late October 2025, fintech lenders trade at ~7x forward earnings, often above book value, signaling market confidence in their scalability but wariness of credit and funding risks. Traditional banks, by contrast, command 9–10x earnings and 1.1–1.3x tangible book value, reflecting the stability of deposit funding and diversified income streams. High-performing fintechs and BNPL platforms with disciplined underwriting and scalable technology post strong returns on equity, commanding premium multiples. Weaker players, however, face low single-digit P/E ratios or trade below book value due to credit losses or regulatory missteps.

This “trust discount” applied to fintechs and BNPL providers creates opportunities. Banks can acquire fintech platforms to modernize underwriting and distribution, while fintechs with strong analytics but limited capital can benefit from deeper bank partnerships. For example, BNPL providers like Affirm could enhance bank offerings by integrating flexible payment options into existing credit products.

As digital lending evolves, success will hinge on balancing innovation with timeless banking principles based upon capital, credit and funding stability with innovation, growth and a larger addressable market that fintech/BNPL enables.

Mercer Capital is a business valuation and financial advisory firm that values the securities and assets (e.g., portfolio fair value) of privately held financial and non-financial companies. Our advisory services entail M&A representation and the provision of transaction opinions (fairness and solvency). Please call if we can be of assistance.