Beyond the Balance Sheet: Four Strategic Questions for Family Business Directors

If the income statement is a movie that records how your family business performed during a particular period, the balance sheet is a snapshot that records what your family business looked like at a particular date.

The defining characteristic of an asset is that it represents a future economic benefit. So, as you review your family business’s balance sheet, your focus should not be on how much the various assets cost, but instead on what future economic benefits those assets will generate. As a family business director, you need to focus not just on what assets your business owns, but more importantly, why your family business owns those assets.

Today, we’re going to pose four questions that family business directors should think about with regard to their company’s asset base.

1. What is your family business’s cash strategy?

We see cash fulfilling a number of different roles for our family business clients:

- Liquidity to meet current obligations as they come due. This is the most fundamental (and necessary) use of cash in a family business. Do you have a target level of cash to meet the operating needs of the business?

- Sinking fund for future capital expenditures or debt repayment. Accumulating cash balances to pay for anticipated investments or loan repayments can eliminate transaction costs for financing events, reduce interest expense, and reduce the risk that credit will not be available when needed. These are worthwhile objectives for many family businesses, but there is a cost to these benefits in the form of depressed returns on family capital.

- Hedge against uncertainty. Some family businesses maintain additional cash balances to provide a margin of safety against the uncertainty inherent in their business model.

- Insurance against failure of corporate strategy. Eventually, prudent risk management morphs into unhealthy risk aversion as some family businesses hold such large cash balances that they are no longer hedging uncertainty, but attempting to insure against failure. In addition to dragging down returns of family capital, this use of cash can promote management complacence (we never have to worry about making payroll, etc.) or encourage inefficient capital investment (all that money does eventually burn a hole in someone’s pocket). Directors should carefully evaluate just whose risks are being managed in this case: the family shareholders, or management?

- The asset of last resort. Finally, for some family businesses, cash can become the asset of last resort. This most often reflects some degree of family dysfunction, often expressed in the belief of family leaders that family shareholders can’t be trusted with dividends, so the money is safer in the company. And if the company doesn’t have a productive use for the capital, it just sits there, weighing down returns on family capital.

2. What is your family business’s working capital strategy?

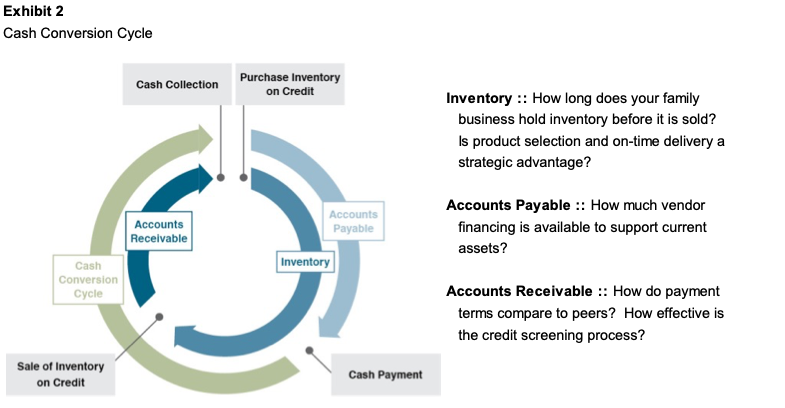

The most comprehensive measure of working capital management is the cash conversion cycle, which measures the time elapsed from when cash is paid for inventory to when cash is received from customers. Different industries and business models have different cash conversion cycle expectations. The graphic below illustrates the cash conversion cycle and identifies some key questions for family business directors with regard to each major component. Less working capital is not always best; there may be potential strategic advantages to maintaining deep inventories or providing generous customer financing terms, but if such is the case, the rationale and corresponding benefits (superior pricing, etc.) need to be clearly noted.

3. How effective is your capital budgeting process?

The balance of net fixed assets is the cumulative result of all the capital budgeting decisions your family business makes. How effective is that process? Do managers have a clearly articulated strategy that guides what sorts of capital investments are needed? Has the board established hurdle rates for capital investment to define financial feasibility for proposed projects? Does the company have a strategy for minimizing the impact of cognitive biases that lead to over-optimistic projections? Is there a feedback mechanism in place to ensure that actual results are compared to projections for proposed capital projects? As a family business director, you should be diligent to ensure that the capital budgeting process works to advance the company’s strategy.

4. Do you know what makes your family business valuable?

This is not the same thing as knowing what your family business is worth (although that is important, too). Instead, the focus is on understanding what core attributes of your family business make it valuable. In one sense, your family business can be viewed as a portfolio of assets. If those assets work together in executing an effective strategy that takes advantage of – and builds – the company’s sustainable competitive advantages, the value of the whole can be far greater than the sum of the individual assets. The competitive advantages that drive higher market values become progressively more difficult to sustain.

What is your family business’s story and strategy? What makes it valuable? Without a clear answer to these questions, your family business is likely to get “stuck” and eventually experience slowing sales growth and shrinking returns, both of which have unpleasant side effects on the family.

As a family business director, your role is akin to that of a portfolio manager. As a good portfolio manager, you should care not just what assets your family business owns, but why it owns them. In other words, what makes your family business valuable, and how does the current portfolio of assets contribute to enhancing and sustaining that value?

Conclusion

Understanding your family business’s asset base is more than a financial exercise; it is a strategic responsibility. By asking the right questions about cash, working capital, capital investments, and what truly drives value, directors can shift the conversation from what the business owns to why it owns it. This shift in perspective not only promotes smarter decision-making but also ensures that every asset is aligned with the long-term goals of the family and the business. If you haven’t revisited your asset strategy lately, now may be the perfect time to start the conversation.