A Guide to Corporate Finance Fundamentals

Part 2 | Finance Basics: Capital Structure

This post is the second of four installments from our Corporate Finance in 30 Minutes whitepaper. In this series of posts, we walk through the three key decisions of capital structure, capital budgeting, and dividend policy to assist family business directors and shareholders without a finance background to make relevant and meaningful contributions to the most consequential financial decisions all companies must make.

Three Questions

Corporate finance is the search for rational answers to three fundamental questions.

- The Capital Structure Question: What is the most efficient mix of capital? In other words, is there such a thing as too little or too much debt?

- The Capital Budgeting Question: What capital projects merit investment? In other words, given the expectations of those providing capital to the business, how should potential capital projects be evaluated and selected?

- The Distribution Policy Question: What mix of returns do shareholders desire? In other words, do shareholders prefer current income or capital appreciation? Do these shareholder preferences “fit” the company’s strategic position? Can these shareholder preferences be accommodated within the existing capital structure?

These three questions do not stand alone, but the answer to each one influences the answers to the others.

Question #1: Capital Structure

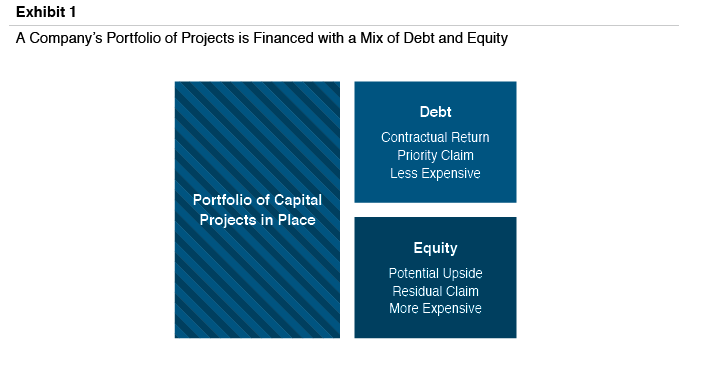

From a corporate finance perspective, a family business can be thought of as a portfolio of capital projects. The portfolio must be financed with a combination of debt and equity. The specific combination of debt and equity used is called the company’s capital structure.

As noted in Exhibit 1, lenders are entitled to a contractual return and have a priority claim on the company’s assets. Shareholders, in contrast, benefit from the potential upside of growth opportunities, but have only a residual claim on the company’s assets. Since return follows risk, the expected return for debt holders is lower than that for equity holders.

The analysis of capital structure is complicated by the iterative nature of the risks facing debt and equity holders. For any given proportion of debt and equity, the cost of debt will be lower than the cost of equity.

However, increasing the proportion of debt in the capital structure increases the risk of both the debt and the equity, which in turn raises the cost of each. As illustrated in Exhibit 2, at some point the benefit of using a greater proportion of lower-cost debt is eventually offset by the escalating cost of both capital sources.

The optimal capital structure minimizes the overall cost of capital. As shown in Exhibit 2, the optimal capital structure for a company is likely a range rather than a single point, since the underlying measurements are naturally imprecise.

Topics for Board Discussion

While the optimal capital structure cannot be defined with precision, the deliberations of an informed family business board and shareholders will focus on the following:

- What is the company’s current capital structure? The first step is estimating the value of the business enterprise as a whole. What multiple of EBITDA (or some other performance measure) does management believe is appropriate for the Company? What is the basis for that multiple (public companies, transactions, or some rule of thumb)? How do the risk and growth characteristics of the company compare to the selected benchmark?

- How does the company’s capital structure compare to peers? Capital structure is often related to the nature and intensity of a company’s asset requirements, sensitivity to economic cycles and other industry attributes.

- What is the availability and cost of marginal sources of capital? If the company anticipates growth, the supporting capital can come through retention of earnings, issuance of new equity, and/or borrowing. Given the company’s current capital structure, what effect would the various marginal financing decisions have on the overall cost of capital?

- What is the company’s target capital structure? How, if at all, does it differ from the current capital structure? How does it compare to peers? What factors contribute to the differences from peers? Such factors could include differing strategic focus, unique elements of the company’s business model, or shareholder risk preferences.

WHITEPAPER