All EBITDA Is Not Created Equal

Awaiting kick off on the afternoon of the big game, one of the perennial features of the interminable pre-game show is the obligatory head-to-head matchup segment, in which the network analysts go through the starting lineups position by position, comparing the relative strengths and weaknesses of the quarterbacks, linebackers, kickers, waterboys, etc. The conceit of the segment is that, while both teams will field the same basic positions, not all cornerbacks are created equal. If the analyst can reliably discern which team has the advantage at the most individual positions, perhaps that will reveal the winner ahead of time. For our part, we predict that Kansas City Tampa Bay will win by 10 22 points.

All of which got us to thinking about, well, EBITDA (earnings before interest, taxes, depreciation, and amortization). In the world of family-owned and other private businesses, EBITDA is the most commonly cited performance measure. Much like left tackles, every company has EBITDA, but some EBITDA is better than others. Why is that?

What Is EBITDA and Why Does It Matter?

EBITDA is an example of a non-GAAP performance measure, meaning it is not a line item on audited financial statements. EBITDA gets a lot of attention because it is a proxy for the operating cash flow that is, in turn, available for a broad variety of corporate purposes. EBITDA is especially popular in the M&A markets because it is a measure of the discretionary cash flow available to a potential buyer of a business.

EBITDA also promotes comparability across firms by “normalizing” for structural features of how those companies are organized, financed, and assembled. This is best seen by considering the various adjustments to net income that are made to arrive at EBITDA. We will start from the bottom of the income statement.

- Income Taxes – Many family businesses are organized as tax pass-through entities (S corps or LLCs) and report no corporate income tax expense. Because taxes are excluded from EBITDA, all companies are on equal footing, regardless of their tax structure.

- Interest Expense – Financing operations with debt rather than equity does not directly influence the operating results of the business. As with taxes, interest expense is excluded from EBITDA, allowing direct comparison of performance by different companies having different capital structures.

- Depreciation Expense – Depreciation expense is a non-cash charge that accountants use to allocate the cost of long-lived assets to the accounting periods during which the assets are expected to be used. As you might guess, a lot of assumptions go into those calculations, each of which potentially impairs the comparability of reported earnings to those of other companies that may make different assumptions. Since EBITDA ignores depreciation charges, it erases that potential obstacle to comparability.

- Amortization Expense – Some companies grow through acquisition, while others grow organically. If acquirers pay more than the value of the net tangible assets of the target companies, they must write off the excess in the periods following the acquisition. Companies growing organically do not have comparable amortization expenses. Thus, EBITDA is comparable for businesses, whether they grow through acquisition or organically.

Limitations of EBITDA

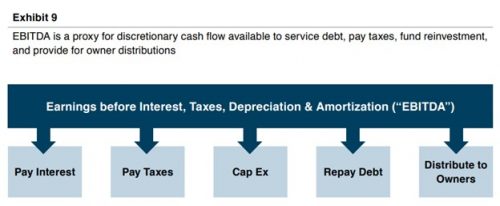

The following chart (Exhibit 9 from our whitepaper, Basics of Financial Statement Analysis) illustrates the five basic uses of EBITDA.

Importantly, of these five uses, only three provide direct returns to capital providers: paying interest, repaying debt, and distributing to owners. The other two, paying taxes and capital expenditures, do not directly accrue to the benefit of shareholders.

This is generally obvious with regard to taxes but requires more finesse for capital expenditures. We can divide capital expenditures (in the economic rather than accounting sense) into two groups:

- Maintenance Capital Expenditures – Family businesses focused on sustainability recognize that a portion of operating cash flow must be set aside each year to maintain productive capacity. Depreciation expense is an imperfect proxy for this obligation. The reality of this maintenance capex burden lies at the heart of legendary investor Warren Buffett’s infamous tooth fairy warning on EBITDA.

- Growth Capital Expenditures – But not all capex is maintenance capex. Family businesses also invest to grow (whether through M&A or organic investments). Since these investments should only be made if the expected returns exceed the company’s cost of capital, these “elective” expenditures are made in lieu of distributions to capital providers in the expectation that they will generate long-term benefits that more than makeup for the deferral in distributions.

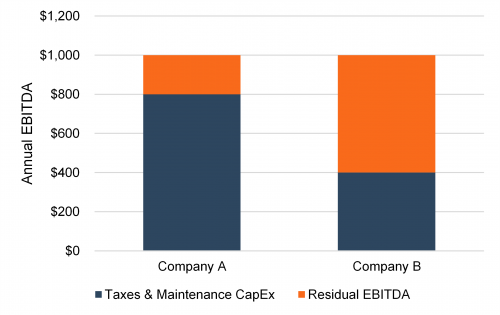

The point of all this is that a dollar of EBITDA is not just a dollar of EBITDA. The quality of a dollar of EBITDA depends on how much of that dollar is allocable to taxes and maintenance capital expenditures. Consider the two companies summarized in the following chart.

Company A and Company B both generate the same amount of EBITDA, yet Company B’s EBITDA is of much higher quality because taxes and maintenance capital expenditures consume a much smaller portion of EBITDA than for Company A. Accordingly, investors will likely assign a higher EBITDA multiple to Company B than Company A (all else equal). This is borne out when we look at data for non-financial companies in the Russell 2000.

Company A and Company B both generate the same amount of EBITDA, yet Company B’s EBITDA is of much higher quality because taxes and maintenance capital expenditures consume a much smaller portion of EBITDA than for Company A. Accordingly, investors will likely assign a higher EBITDA multiple to Company B than Company A (all else equal). This is borne out when we look at data for non-financial companies in the Russell 2000.

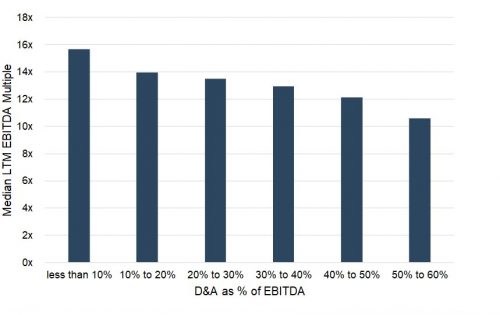

The value assigned by the market to each dollar of EBITDA follows a predictable pattern as depreciation & amortization consumes a greater portion of EBITDA. Ideally, we would look at depreciation only, but the data aggregation services generally only provide the aggregate number. Even so, the point stands.

Conclusion

So, should family business directors be as dismissive toward EBITDA as Warren Buffett? We do not think so, although it is important for directors to take Mr. Buffett’s reservations to heart and understand that not every dollar of EBITDA is created equally. This is important for two reasons. First, doing so helps directors take EBITDA multiples with the appropriate grain of salt. Since the value of a dollar of EBITDA depends on the quality of that dollar, quoted EBITDA multiples should be evaluated with due caution. Second, this underscores the importance of incremental EBITDA. Once taxes and maintenance capital expenditures have been covered, marginal dollars of EBITDA are of the highest quality (and therefore most valuable). As a result, improving EBITDA margins can have a multiplicative impact on the value of your family business by both providing more EBITDA and justifying a higher multiple.

And that is a winning game plan.