Medical Devices Overview

The medical device manufacturing industry produces equipment designed to diagnose and treat patients within global healthcare systems. Medical devices range from simple tongue depressors and bandages, to complex programmable pacemakers and sophisticated imaging systems. Major product categories include surgical implants and instruments, medical supplies, electro-medical equipment, in-vitro diagnostic equipment and reagents, irradiation apparatuses, and dental goods.

The following outlines five structural factors and trends that influence demand and supply of medical devices and related procedures.

1. Demographics

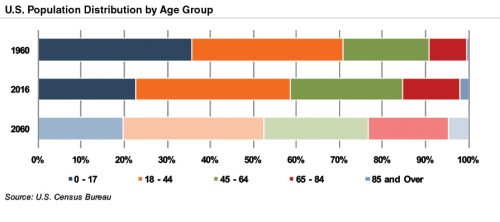

The aging population, driven by declining fertility rates and increasing life expectancy, represents a major demand driver for medical devices. The U.S. elderly population (persons aged 65 and above) totaled 49 million in 2016 (15% of the population). The U.S. Census Bureau estimates that the elderly will roughly double by 2060 to 95 million, representing 23% of the total population.

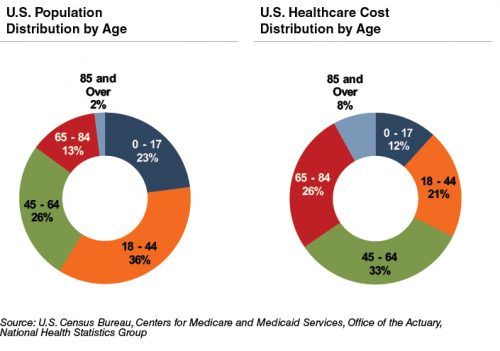

The elderly account for nearly one-third of total healthcare consumption. Personal healthcare spending for the population segment was $19,000 per person in 2012, five times the spending per child ($3,600) and almost triple the spending per working-age person ($6,600).

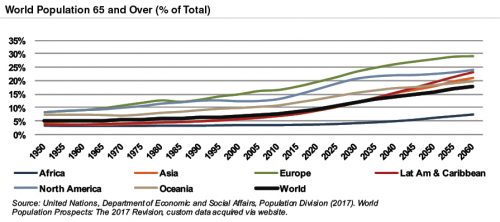

According to United Nations projections, the global elderly population will rise from approximately 610 million (8.3% of world population) in 2015 to 1.8 billion (17.8% of world population) in 2060. Europe’s elderly are projected to reach nearly 29% of the population by 2060, making it the world’s oldest region. While Latin America and Asia are currently relatively young, these regions are expected to undergo drastic transformations over the next several decades, with the elderly population expected to expand from approximately 8% in 2015 to more than 21% of the total population by 2060.

2. Healthcare Spending and the Legislative Landscape in the U.S.

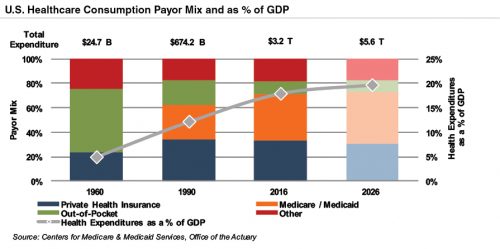

Demographic shifts underlie the expected growth in total U.S. healthcare expenditure from $3.3 trillion in 2016 to $5.7 trillion in 2026, an average annual growth rate of 5.5%. While this projected average annual growth rate is more modest than that of 7.3% observed from 1990 through 2007, it is more rapid than the observed rate of 4.2% between 2008 and 2016. Projected growth in annual spending for Medicare (7.4%) and Medicaid (5.8%) is expected to contribute substantially to the increase in national health expenditure over the coming decade. Healthcare spending as a percentage of GDP is expected to expand from 18% in 2016 to nearly 20% by 2026.

Since inception, Medicare has accounted for an increasing proportion of total US healthcare expenditures. Medicare currently provides healthcare benefits for an estimated 57 million elderly and disabled people, constituting approximately 15% of the federal budget in 2016. Medicare represents the largest portion of total healthcare costs, constituting 20% of total health spending in 2015. Medicare also accounts for 26% of hospital spending, 29% of retail prescription drugs sales, and 23% of physician services.

Owing to the growing influence of Medicare in aggregate healthcare consumption, legislative developments can have a potentially outsized effect on the demand and pricing for medical products and services. Net mandatory benefit outlays (gross outlays less offsetting receipts) to Medicare totaled $588 billion in 2016, and are expected to reach $1.1 trillion by 2026.

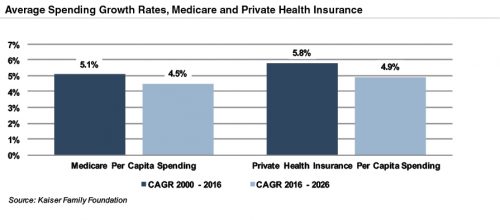

The Patient Protection and Affordable Care Act (“ACA”) of 2010 incorporated changes that are expected to constrain annual growth in Medicare spending over the next several decades, including reductions in Medicare payments to plans and providers, increased revenues, and new delivery system reforms that aim to improve efficiency and quality of patient care and reduce costs. On a per person basis, Medicare spending is projected to grow at 4.5% annually between 2016 and 2026, compared to 5.1% average annualized growth realized between 2000 and 2016.

As part of ACA legislation, a 2.3% excise tax was imposed on certain medical devices for sales by manufacturers, producers, or importers. The tax had become effective on December 31, 2012, but met resistance from industry participants and policy makers. In late 2015, Congress passed legislation promulgating a two-year moratorium on the tax beginning January 2016. In January 2018, the moratorium suspending the medical device excise tax was extended through 2019.

3. Third-Party Coverage and Reimbursement

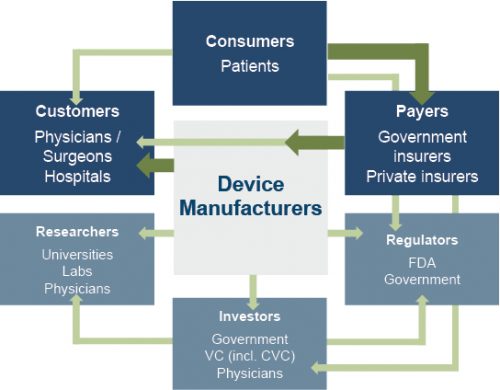

The primary customers of medical device companies are physicians (and/or product approval committees at their hospitals), who select the appropriate equipment for consumers (patients). In most developed economies, the consumers themselves are one (or more) step removed from interactions with manufacturers, and therefore pricing of medical devices. Device manufacturers ultimately receive payments from insurers, who usually reimburse healthcare providers for routine procedures (rather than for specific components like the devices used). Accordingly, medical device purchasing decisions tend to be largely disconnected from price.

Third-party payors (both private and government programs) are keen to reevaluate their payment policies to constrain rising healthcare costs. Several elements of the ACA are expected to limit reimbursement growth for hospitals, which form the largest market for medical devices. Lower reimbursement growth will likely persuade hospitals to scrutinize medical purchases by adopting i) higher standards to evaluate the benefits of new procedures and devices, and ii) a more disciplined price bargaining stance.

The transition of the healthcare delivery paradigm from fee-for-service (FFS) to value models is expected to lead to fewer hospital admissions and procedures, given the focus on cost-cutting and efficiency. In 2015, the Department of Health and Human Services (HHS) announced goals to have 85% and 90% of all Medicare payments tied to quality or value by 2016 and 2018, respectively, and 30% and 50% of total Medicare payments tied to alternative payment models (APM) by the end of 2016 and 2018, respectively. A report issued by the Health Care Payment Learning & Action Network (LAN), a public-private partnership launched in March 2015 by HHS, found that 29% of payments were tied to APMs, a 6% increase from 2015 to 2016.

While the shift toward value-based care is continuing, the pace could slow under the new administration. In November 2017, the CMS partially canceled bundled payment programs for certain joint replacement and cardiac rehabilitation procedures. However, indications are that the CMS supports value-based care and wants pilot programs to accelerate. Ultimately, lower reimbursement rates and reduced procedure volume will likely limit pricing gains for medical devices and equipment.

The medical device industry faces similar reimbursement issues globally, as the EU and other jurisdictions face increasing healthcare costs, as well. A number of countries have instituted price ceilings on certain medical procedures, which could deflate the reimbursement rates of third-party payors, forcing down product prices. Industry participants are required to report manufacturing costs and medical device reimbursement rates are set potentially below those figures in certain major markets like Germany, France, Japan, Taiwan, Korea, China and Brazil. Whether third-party payors consider certain devices medically reasonable or necessary for operations presents a hurdle that device makers and manufacturers must overcome in bringing their devices to market.

4. Competitive Factors and Regulatory Regime

Historically, much of the growth for medical technology companies has been predicated on continual product innovations that make devices easier for doctors to use and improve health outcomes for the patients. Successful product development usually requires significant R&D outlays and a measure of luck. However, viable new devices can elevate average selling prices, market penetration, and market share.

Government regulations curb competition in two ways to foster an environment where firms may realize an acceptable level of returns on their R&D investments. First, firms that are first to the market with a new product can benefit from patents and intellectual property protection giving them a competitive advantage for a finite period. Second, regulations govern medical device design and development, preclinical and clinical testing, premarket clearance or approval, registration and listing, manufacturing, labeling, storage, advertising and promotions, sales and distribution, export and import, and post market surveillance.

Regulatory Overview in the U.S.

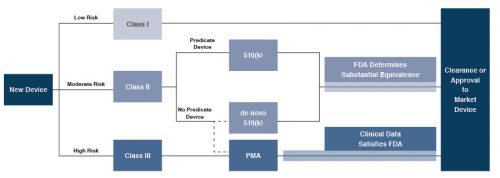

In the U.S., the FDA generally oversees the implementation of the second set of regulations. Some relatively simple devices deemed to pose low risk are exempt from the FDA’s clearance requirement and can be marketed in the U.S. without prior authorization. For the remaining devices, commercial distribution requires marketing authorization from the FDA, which comes in primarily two flavors.

- The premarket notification (“510(k) clearance”) process requires the manufacturer to demonstrate that a device is “substantially equivalent” to an existing device that is legally marketed in the U.S. The 510(k) clearance process may occasionally require clinical data, and generally takes between 90 days and one year for completion.

- The premarket approval (“PMA”) process is more stringent, time-consuming and expensive. A PMA application must be supported by valid scientific evidence, which typically entails collection of extensive technical, preclinical, clinical and manufacturing data. Once the PMA is submitted and found to be complete, the FDA begins an in-depth review, which is required by statute to take no longer than 180 days. However, the process typically takes significantly longer, and may require several years to complete.

Pursuant to the Medical Device User Fee Modernization Act (MDUFA), the FDA collects user fees for the review of devices for marketing clearance or approval. The current iteration of the Medical Device User Fee Act (MDUFA IV) came into effect in October 2017. Under MDUFA IV, the FDA is authorized to collect almost $1 billion in user fees, an increase of more than $320 million over MDUFA III, between 2017 and 2022.

Regulatory Overview Outside the U.S.

The European Union (EU), along with countries such as Japan, Canada, and Australia all operate strict regulatory regimes similar to that of the FDA, and international consensus is moving towards more stringent regulations. Stricter regulations for new devices may slow release dates and may negatively affect companies within the industry.

Medical device manufacturers face a single regulatory body across the EU. In order for a medical device to be allowed on the market, it must meet the requirements set by the EU Medical Devices Directive. Devices must receive a Conformité Européenne (CE) Mark certificate before they are allowed to be sold in that market. This CE marking verifies that a device meets all regulatory requirements, including EU safety standards. A set of different directives apply to different types of devices, potentially increasing the complexity and cost of compliance.

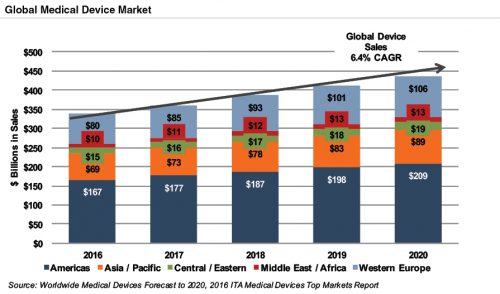

5. Emerging Global Markets

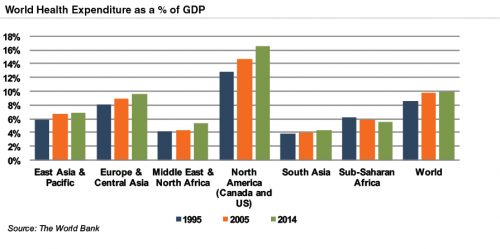

Emerging economies are claiming a growing share of global healthcare consumption, including medical devices and related procedures, owing to relative economic prosperity, growing medical awareness, and increasing (and increasingly aging) populations. As global health expenditure continues to increase, sales to countries outside the U.S. represent a potential avenue for growth for domestic medical device companies. According to the World Bank, all regions (except Sub-Saharan Africa) have seen an increase in healthcare spending as a percentage of total output over the last two decades.

Global medical devices sales are estimated to increase 6.4% annually from 2016 to 2020, reaching nearly $440 billion according to the International Trade Administration. While the Americas are projected to remain the world’s largest medical device market, the Asia/Pacific and Western Europe markets are expected to expand at a quicker pace over the next several years.

Bonus Items for 2018

The following is a (non-ordered) list of items likely relevant for the medical device and med tech industry over the shorter-term.

Tax Reform

Passage of tax reform legislation in late 2017 appears to have invigorated market participants across many sectors of the economy. While the full effect of the new legislation will likely play out over the course of the rest of the year and beyond, the implications for valuation (multiples) are generally expected to be positive. The effective tax rates for many multinational medical device companies were already below the new corporate rate. Accordingly, reductions in overall tax burdens for device companies are likely modest. A more immediate effect materialized in the form of a transition tax on corporate cash parked outside the U.S. (for example, Johnson and Johnson reported a one-time $13.6 billion charge related to the new tax law). With a lower tax rate available on deemed repatriation, many corporations will likely have a more direct access to hitherto-unused overseas funds.

Innovation

Given the structural underpinnings (discussed in earlier sections), continued innovation is probably a low-risk bet vis-à-vis the medical device industry and is likely to materialize along three dimensions. First, the traditional product pipeline nursed by the industry over the years is likely to continue turning out iterative and transformative changes to improve or create new devices (hardware). Second, cost pressures as well as technological developments outside the industry will likely fuel new data analysis and tele-communication products and services (software) that augment or complement the traditionally product-only offerings of device and med tech companies. Finally, business model innovations in response to the changing pricing and competitive landscape will become increasingly relevant, especially for the more mature devices.

M&A

The level of deal activity in the industry observed in 2017 will likely continue in 2018 as consolidation within certain sub-sectors could provide (a degree of) inoculation against the ravages of competitive forces. Some potential acquirers will also be buoyed by the unlocking of the cash resources previously trapped overseas. As in 2017, transaction motivations will likely mirror the three dimensions of innovation as firms pursue i) acquisition of complementary products, ii) access to newer higher-growth markets or segments, and iii) ability to address changes in the modes of care delivery that increasingly favor lower acuity settings over lengthy hospital stays.

Summary

Demographic shifts underlie the long-term market opportunity for medical device manufacturers. While efforts to control costs on the part of the government insurer in the U.S. may limit future pricing growth for incumbent products, a growing global market provides domestic device manufacturers with an opportunity to broaden and diversify their geographic revenue base. Developing new products and procedures is risky and usually more resource intensive compared to some other growth sectors of the economy. However, barriers to entry in the form of existing regulations provide a measure of relief from competition, especially for newly developed products.