Alternative Asset Managers

Performance Update

In May of this year, assets in passively managed funds equaled assets actively managed for the first time in history. As investors seek low-cost solutions, alternative managers are working to solidify their place in investors’ portfolios. Despite the headwinds the asset management industry faces, most investors still value the diversification offered by alternative assets, particularly late in the economic cycle. In this post, we take a closer look at how alternative asset managers are performing in light of the broader shift from active to passive management and increased fee pressure.

Industry Outlook

While hedge funds are not a perfect proxy for the broader alternatives industry, we can better understand the pressure the industry faces by analyzing hedge fund asset flows. Hedge funds recorded their fifth consecutive quarterly withdrawal in Q2 2019 and the largest semiannual outflow ($47.4 billion) since the second half of 2016. Despite this, hedge fund assets under management grew 4.4% since the end of 2018 as positive performance offset fund flows. While hedge funds have underperformed over the last decade (since 2009 the S&P 500 index has dwarfed the performance of hedge funds as measured by the HFRI Fund Weighted Composite Index), recent volatility has improved their performance on a relative basis. Hedge fund capital typically lags performance, so we expect to see asset outflows slow in the coming months as investors reallocate their portfolios in light of recent performance.

Alternative assets typically serve to either increase diversification or enhance portfolio returns. In a near-zero interest rate environment, institutional investors have sought return generating assets. Over the last couple of years, pension funds have started diversifying their portfolios to include alternative assets in order to chase higher risk, higher return assets. It is typically more difficult for the average investor to gain exposure to alternative assets due to the often significant minimum investment requirements. While some efforts have been made to expand distribution to the retail market, institutional investors are still the primary target market for alternative managers. Over the last several years, alternative asset managers have been largely successful at securing a spot in institutional investors’ portfolios.

In terms of diversification, investors have started positioning themselves for longer-term volatility due to increased geopolitical tensions and a slowing IPO market. While investor interest in uncorrelated asset classes such as alternatives fell during the longest bull market run in history, recent volatility could push investors back to the asset class.

Practice Management

Today, the main priority for most alternative asset managers is raising assets. Assets follow performance, especially in the alternatives space, and one way to directly impact investor returns is to reduce fees. After a decade of lackluster performance, reducing costs has become a key issue for alternative managers seeking to bring in new assets. Amidst fee pressure, alterative managers are deviating from the typical “2 and 20” model.

While traditional asset managers have been able to reduce fees by achieving some measure of scale, alternative managers must be careful to not sacrifice specialization in key strategies for scale. Alternative managers have seen some success utilizing technology in the front office or outsourcing certain functions in order to reduce overhead and spare time for management to focus on asset raising.

Industry Valuations

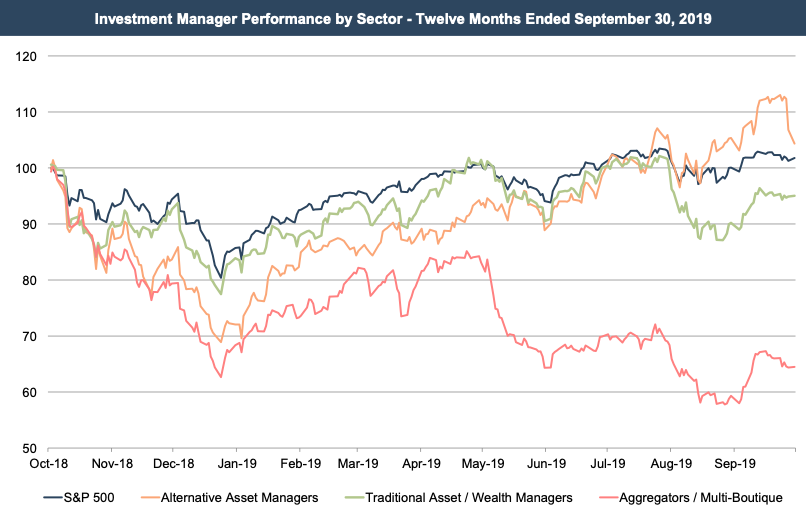

In the eyes of market participants, the industry has performed well over the last year. Generally, alternative asset managers have been more resilient to price declines than traditional asset and wealth managers. Our alternative asset manager index is up 4.4% year-over-year, compared to our index of traditional asset and wealth manages which was down for the year.

Price to LTM earnings multiples have recently increased for alternative asset managers as prices over the last year increased by a median of 16%. Current pricing is close to the 52 week high and forward multiples are noticeably lower than LTM multiples, suggesting that publicly traded alternative asset managers are currently trading at peak valuations and earnings are expected to increase over the next twelve months.

Summary

Despite improving performance over the last few years, the industry continues to face a number of headwinds, including fee pressure and expanding index opportunities. While the idea of passively managed alternative asset products seems like an oxymoron, a number of funds exist with a goal of imitating private equity returns. Innovative products are being made available to the investing public every day. And while there is currently no passive substitute to alternatives, we do believe that the industry will continue to be influenced by many of the same pressures that traditional asset managers are facing today despite the recent uptick in alt manager valuations.