Brexit and Killen Underscore the Need for Buyer Protection in Asset Manager Transactions

Black swan events and the very nature of the asset management business illustrate the importance of contingent consideration in RIA acquisitions for prospective buyers. The volatility associated with equity managers means AUM and financial performance can swing widely with market conditions, so doubling down on a one-time payment for an RIA can be extremely risky, particularly at high valuations. Of course, the market can just as easily pivot in the buyer’s favor after the deal closes, but gaining Board approval for such gambles is an exercise in futility if insurance is available in the form of contingent consideration.

Back in December, we blogged about Tri-State Capital’s recently announced acquisition of $2.6 billion manager, The Killen Group of Berwyn, PA. The deal terms included an initial $15 million payment and contingent consideration of 7x any incremental growth in Killen’s annual run rate EBITDA in excess of $3 million for the pending calendar year (2016). Upon announcement, the estimated total deal value was in the $30-$35 million range, but when the deal closed in April, this estimate dropped to $15-$20 million. The table below illustrates the implied valuation metrics and returns had this deal been structured as a one-time payment under the two value scenarios.

Fortunately for Tri-State, the bank elected to structure the deal as an earn-out whereby roughly half of the total potential consideration was guaranteed and the remaining half had to be “earned” by meeting certain earnings objectives following deal closure. The downward revision implies that the business is not likely to generate more than $3 million in EBITDA this year, and an ~11x purchase for a closely held RIA with compliance issues and a declining AUM balance (ADV disclosures indicate that Killen’s AUM fell 27% in 2015) would have been hard to justify had the total deal value been paid up front. Instead, Tri-State is still likely to boast a decent ROI on this deal without paying another dime for it if the business fails to perform in line with initial expectations. The following table shows the implied total deal value under four different scenarios of EBITDA for this year.

Under this structure, the seller is incentivized to ensure the business continues to perform after the initial payment. This assurance is critical in many RIAs that are often heavily dependent upon the selling shareholder(s) for client relationships or investing acumen. If key accounts are not transitioned to the prospective acquirer or the market corrects itself following the transaction, the buyer will likely be off the hook for further consideration.

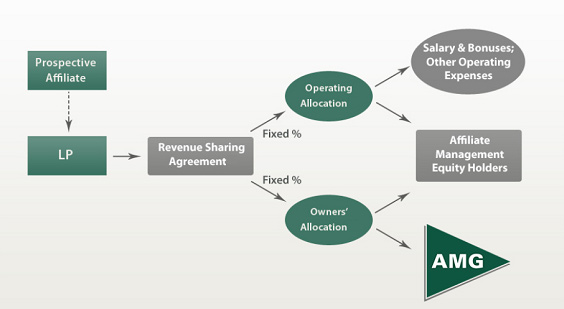

Contingent consideration doesn’t always have to be based on future earnings. Perhaps the most acquisitive business in the RIA space is Affiliated Managers Group, whose investment model includes a revenue sharing agreement whereby the target’s fees are split (at a fixed percentage) into two segments: the operating allocation and the owners’ allocation. The operating allocation covers all operating expenses of the affiliate (target) at the discretion of the target’s management, while the owner’s allocation goes to the firm’s partners and AMG according to their respective ownership interest in the business.

Source: AMG

This structure allows the affiliate to retain operating autonomy while limiting AMG’s exposure to operating leverage because the owners’ allocation is set at a fixed percentage of revenue, not earnings. Since there’s usually some portion of an asset manager’s expense base that is predominantly fixed, earnings are typically more volatile than fee income, so the revenue sharing agreement is a partial hedge against earnings volatility during a Brexit or other black swan event.

Still, the best hedge against a market downturn is a solid profit margin, as we’ve discussed in a prior post. With Brexit coinciding with a quarterly billing cycle for many asset managers, earnings are likely to take a huge hit along with the market. Those RIAs with a robust EBITDA margin will likely stay in the black as opposed to their less profitable counterparts that may be under water until market conditions improve.