Death Week (for Active Management?)

Photo Credit: Memphis CBV

Mercer Capital’s asset management valuation practice is run from our main office in Memphis, Tennessee, and this time of year here means one thing: Death Week. Every year since his death on August 16, 1977, the city of Memphis spends a week memorializing Elvis Presley, the King of Rock and Roll. If you have never been, Death Week is basically seven to ten days of activities in which the Presley faithful arrive from every continent to pay their respects and enjoy what has to be some of the hottest, most humid weather anywhere on the globe.

From all the press lately, you would expect that a similar wake was being held for active management, and with it, much of the RIA community. Elvis is dead, and so too must be active management. We live in the age of auto-tune and robo-advisors, a time when big vocal chords and beating the market have become anachronisms – or are they?

Academics have been testifying as to the shortcomings of active management for decades, and by the time I was studying for the CFA exams (back in the ’90s, as a colleague is quick to remind me), what was then known as AIMR (a midlife identity crisis between its founding as ICFA and what is now known as CFAI) had joined in to “educate” us on the relative virtue of passive investing. Today, ETFs and indexing are common, and in the wealth management community, have done much to streamline asset allocation. For asset management, though, the rise of indexing is the number one threat to the lifeblood of the RIA community: fees.

The RIA business model is, after all, pretty simple; AUM times fee schedule equals revenue, revenue minus labor costs and other more mundane expenses equals margin, and sustainability of margin drives value. If active management fees are threatened, it will ultimately threaten to disinflate valuations in the asset management community.

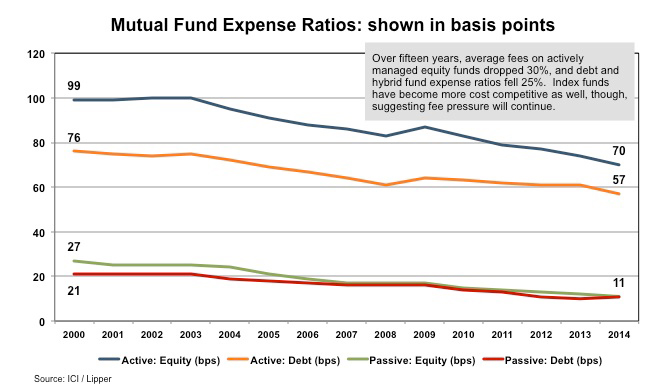

There is cause for concern. A study performed by the Investment Company Institute (or “ICI”) and Lipper showed average mutual fund expenses and fees declining 30% (!) over the past fifteen years, from about 99bps to 70bps in equity funds (read the study at www.icifactbook.org). Bond funds fared only slightly better, dropping 25% from an average 76bps to 57bps over the same period. The trend-line is basically unbroken with not inconsequential declines over the past three to five years.

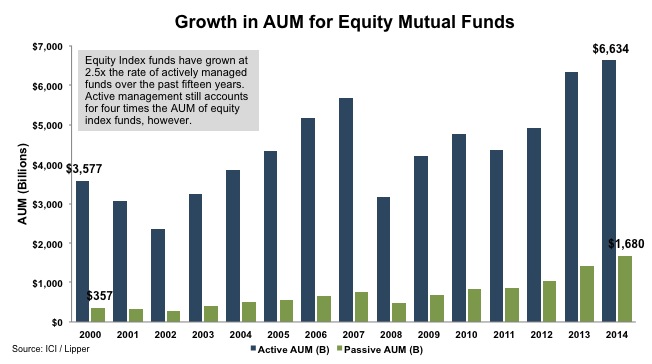

The decline in fees has been stealthy, as active managers haven’t been cutting fees so much as missing out on new assets to manage. During this same timeframe, AUM in equity index funds has increased almost six fold, from $384 billion in 2000 to $2.1 trillion last year. Actively managed funds have reduced fees somewhat: with expense ratios dropping from 106 basis points in 2000 to 86 last year. Some of this can be attributed to the growth in size (and the corresponding efficiencies) created by larger actively managed equity funds, but the competitive threat from equity index funds (with average fees of 11 basis points), has to have kept more than one young manager contemplating a buy-in to his or her RIA up at night.

Anecdotally, our valuation practice at Mercer Capital seems to serve an RIA community that is unaffected by all of this. We routinely ask clients if they are facing fee pressure and/or are contemplating revising fee schedules downward, and we are routinely told “no.”

Institutional clients are reasonably savvy about negotiating fees, but they always have been. High net worth clients just “want to win”, and are willing to pay for the opportunity to do so. Who’s to say they’re wrong? Many commentators have written that active management is more challenging today than ever precisely because of the professionalization of the investment management industry (when everyone is skilled and educated, no one has an advantage). But passive investing could ultimately generate its own demise, as the rise of robo-group-think in the market constrains liquidity in many securities, and creates the kinds of price inefficiencies that favor active management. Passive investing may eventually just be a “style” that falls out of favor.

As the old saying goes in economics, in the long run we’ll all be dead (or at least retired), so this is no time to be sanguine about fee schedules. Investors of all stripes have more options to put their money to work, investment costs are becoming more transparent than ever, and switching is becoming easier. As clients become more sophisticated, the RIA community will become more so as well, defending fees with unique strategies and service offerings, and defending margins with better use of technology and managed staffing costs. But that’s a topic or two for another post.