Excuse Me, Flo?

Inflows and Outflows Drive Disparity in Performance between Different Classes of Asset Managers

Immediately before ordering the Soup Du Jour and duping Sea Bass into picking up his lunch tab, Jim Carrey’s character in Dumb and Dumber, Lloyd Christmas, rudely accosts his waitress at the Truk-Stop Diner with this inexplicable reference to the early 1980s sitcom starring Polly Holliday as Florence Jean “Flo” Castleberry. Decades after the movie’s release in 1994, the market seems to be postulating the same question in pricing RIAs.

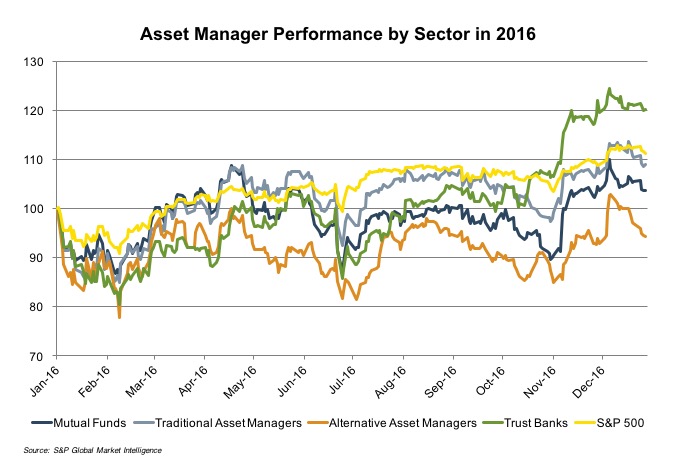

Breaking out the recent performance of various classes of asset managers, we see those sectors that are least dependent on active management (trust banks and traditional managers) as clearly outperforming those more reliant on investment returns (alternative asset managers and mutual funds). While there are other factors at work (a steepening yield curve and hedge fund scandals to name a few), this disparity is largely attributable to investment performance and the impact it has on asset flows.

We touched upon this topic in last week’s post, and basically AUM gains (the primary driver of revenue and profitability for an RIA) are attributable to one or two sources – market gains or client inflows (net of outflows). Since one can’t rely on stocks to always go up, asset flows are a more reliable gauge of an RIA’s sustainable performance regardless of market conditions. As shown above, there is a strong correlation between publicly traded RIAs and the market, so the disparity in performance between the various classes of asset managers is largely attributable to net asset flows. Subpar investment performance and the recent flight to passive products have plagued alternative asset managers and mutual funds, but benefited index providers with more competitive fees.

The market has taken notice and continues to bid up the valuations of passive managers with positive inflows. Part of this outperformance may also be due to the anticipation of more favorable regulation (e.g. the Fiduciary Rule) surrounding passive investors over active management. Stephen Tu, Senior Analyst at Moody’s Investor Service, says, “Under the new regulation, advisors are expected to ensure investments are in the best interests of their clients, rather than merely suitable for them. In practice, it will become more difficult for advisors to place their clients into higher-cost and more complex investment products. Selling low-fee index products, on the other hand, will eliminate many apparent conflicts of interest and minimize fiduciary risk.” In response, many traditional active managers like Janus Capital, Legg Mason, and Franklin Resources have begun offering passive products to take advantage of the prevailing trend.

Despite the high fees and underperformance, we’re not characterizing mutual fund and alternative asset investing as dumb and dumber. The reality is that many active managers do outperform their benchmarks and justify their fees. A proven track record of alpha generation will likely continue to attract assets from institutional clients even if fees aren’t competitive to an ETF that tracks a given benchmark or asset class.

It’s just that beating the market on a consistent basis is a near impossible feat, so most active managers are struggling to keep pace with the rise of passive products that offer a cheaper and more reliable alternative. Much like Harry and Lloyd’s rapid accumulation and subsequent squandering of other people’s money, active managers must improve their performance or lower their fees to avoid a similar fate.