Monday Morning Quarterback: Edelman sells for $800 million (!)

Last week brought the news that PE firm Hellman & Friedman had acquired Lee Equity Partners‘s controlling interest in mega wealth manager Edelman Financial. Edelman is headed by radio-show personality Ric Edelman, and manages about $15 billion for over 28,000 clients. While terms of the deal were not officially disclosed, the Wall Street Journal reported the transaction valued Edelman at a number north of $800 million, a nice pickup from Edelman’s going private deal in 2012, which transacted the company at $263 million. The financial press was practically hyperventilating over the price last week, but a little analysis on the number reveals pricing that is more normal than most would imagine.

Breathe normally

The headline optics of the deal are eye-popping. An $800+ million price is more than triple the transaction value only three years ago, and further implies a price to AUM multiple of over 5% (!). The financial press that immediately followed the announcement ballyhooed the deal as proof that RIAs were hot properties fetching premium pricing and that we could expect more of the same. Count us as being a little more measured in our perception of the deal. While we’re not going to describe the Edelman deal as a “meh” transaction, the firm’s underlying fundamentals are likely far more responsible for the price than an overheated market. Indeed, our analysis suggests Edelman’s pricing was fairly normal. Here are a few reasons to be happy, but not ecstatic, about the Edelman sale:

Edelman is a growth machine

When Edelman went private three years ago, the company reported assets under management of about $8 billion. It’s almost twice that today. While a 30% CAGR in AUM has no doubt been assisted by bull market tailwinds, most of Edelman’s growth has been from growing its investment advisor base and, correspondingly, the number of clients.

Past growth explains the change in valuation from the 2012 going private transaction to the current deal, but Edelman is showing signs of continued growth as well, increasing the number of investment advisors by about 20% this year. RIAs can’t always count on the market to grow the top line, but if a marketing platform is there to add clients, value will accrue.

Edelman fetches premium fees

The real reason Edelman commanded such a high multiple of AUM is the firm’s superior ability to extract fees per dollar of AUM.

Investment management fee schedules are all over the map, with robo-advisors clocking in at around 25-40 basis points, and wealth managers often sticking between 100 and 125 basis points. Historical disclosures suggest that Edelman commands big fees for what they do. In their last public filing (Q2 2012), Edelman boasted investment management fees of over $32 million. Using that quarter as a proxy for an annual run rate of almost $130 million, Edelman was earning realized fees of 160 basis points on AUM of $8 billion. Even assuming that has been dialed back some by market forces puts Edelman’s investment management fee base today at something on the order of $225 million.

Add this to the Company’s other revenue streams (which probably haven’t scaled up to the same extent in the past three years), and we would estimate Edelman’s revenue today to be on the order of $300 million. That’s no threat to Schwab, but in the independent RIA space it suggests that Edelman has defied certain laws of gravity for wealth managers that have plagued other shops at much lower levels of performance. No doubt the scale of Edelman, the pricing power of their services in the market place, and the potential to grow further attracted a strong multiple.

As a caveat to this, higher than market fee schedules are at risk of being “normalized” and doubtless this influenced the valuation of Edelman. That said, it is likely they have been successful at maintaining their value to customers in the marketplace so far.

Edelman has revenue sustainability

Ric Edelman built his firm as a radio personality dispensing advice and gathering assets. His advisor network was excellent at client conversion and retention, and that formula has held up. The cult of personality firm, which we have written about in other posts, has drawbacks. Some still suggest that the firm’s dependence on Edelman at the helm is a risk. We do not entirely disagree, but note that with 28,000 clients investing on average $536 thousand with Edelman, the firm has a solid lock on the mass-affluent investor market.

Client demographics are a big factor in the value of investment managers, and while it’s easier to service a few huge clients, if they leave they take firm value with them. The great thing about larger wealth managers like Edelman is that there is client diversification and product diversification, such that revenue is highly sustainable going forward.

For a PE manager looking for investment return opportunities in what seems to increasingly be a low return environment, Edelman offers a higher quality coupon than most. We know that better coupons pay lower yields, which in Edelman’s case suggests a multiple at the high end of the range.

Edelman probably has a solid margin

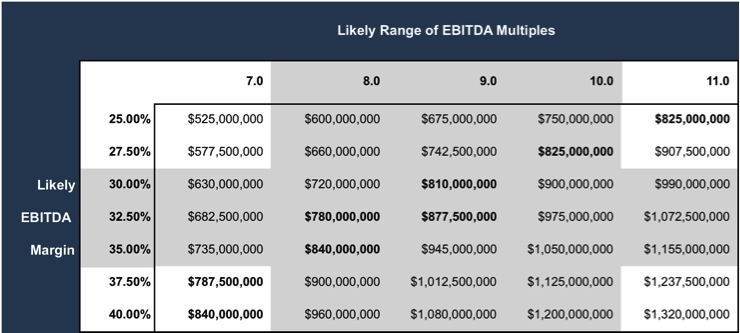

Since Edelman has been private for three years, we don’t have a lot of margin visibility, but we can look back to 2012 and see what we can normalize to get there, especially if it’s consistent with industry norms. Our analysis of Edelman’s run rate at the time of the going private transaction suggests an EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) margin on the order of 30% to 35%. That’s strong, but not out of range with similar firms in the wealth management space. Edelman may have achieved some margin leverage with the growth it has experienced over the past three years, but probably not much. Thus Edelman’s margin provided an optimal circumstance for the valuation multiple, with solid profit performance that does not need “repair” from a new owner, but also not so high as to risk being unsustainable.

Edelman likely got a good, but not extraordinary, multiple

Put it all together and the Edelman transaction looks fairly normal. Assuming an EBITDA margin at or just about 30%, consistent with the level of profitability the company reported before the 2012 going private transaction, HF paid a high single digit multiple of EBITDA.

The deal multiple was likely upward biased by the growth pattern and trajectory of the company, and the risk mitigation afforded by a diverse client base and large scale. Weighing down the multiple was likely some lingering concern over the dependence on Ric Edelman as the spiritual guru of the organization, concern over the sustainability of the firm’s fee schedule, and some angst in general over the direction of capital markets. As solid as this pricing was, we wonder if Edelman couldn’t have fetched closer to $1 billion a year ago when folks believed the market had more room to run.

But that’s neither here nor there. Kudos to Edelman and Lee Equity Partners for a solid return on their three year investment in the company, and to Hellman & Freidman for acquiring a great franchise at a reasonable price such that their investors can also profit. All in all, an increasingly rare event in the PE universe.