M&A activity in the RIA industry, which had been trailing 2023 levels for much of 2024, experienced a dramatic surge in October. This spike set a new record for monthly deal volume and brought year-to-date transaction figures through November in line with 2023’s pace. Fidelity’s November 2024 Wealth Management M&A Transaction Report listed 206 deals through November, which approximates the 207 deals executed during the same period in 2023.

Recent analysis from DeVoe & Company highlights a convergence of factors driving a surge in M&A activity within the RIA industry: a rising stock market that has bolstered valuations combined with lower interest rates that have reduced borrowing costs have created a favorable environment for dealmaking.

![]()

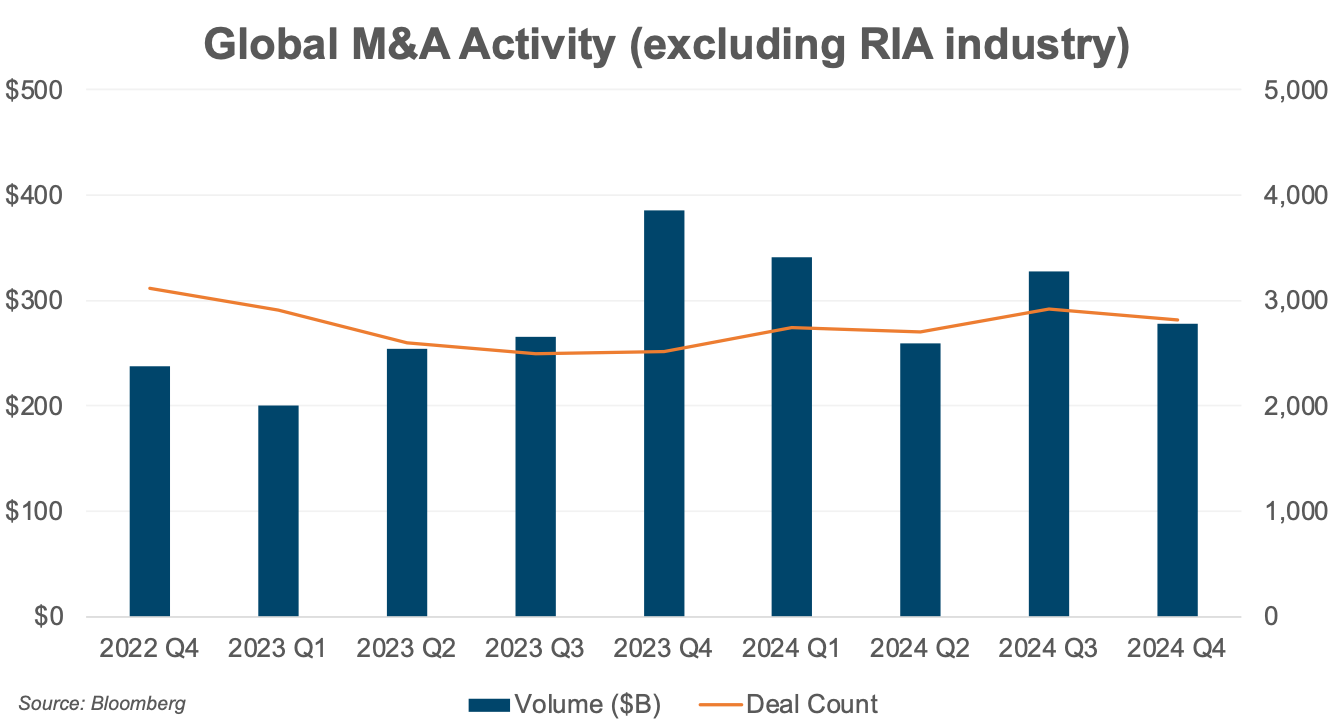

Despite the resurgence in RIA transactions in the fourth quarter, the industry’s overall deal activity still lags behind the broader M&A market. The number of M&A transactions for all industries (excluding the RIA industry) increased by 6% year-over-year (per Bloomberg), compared to the M&A activity in the RIA industry, which remained flat over the same period.  Although a similar number of deals were completed in 2024 as in 2023, there was a significant uptick in total transacted AUM during 2024. As of November 2024, total transacted AUM reached $650.0 billion—a 162% increase from the same period in 2023. The average AUM per transaction during the first eleven months of 2024 was $3.2 billion, a 163% increase over the prior year. The increase in deal size has been an encouraging sign, given the rise in the cost of capital over the past two years. The growth in deal size resulted from the completion of several significant transactions during 2024, coupled with the overall increase in AUM levels due to market performance.

Although a similar number of deals were completed in 2024 as in 2023, there was a significant uptick in total transacted AUM during 2024. As of November 2024, total transacted AUM reached $650.0 billion—a 162% increase from the same period in 2023. The average AUM per transaction during the first eleven months of 2024 was $3.2 billion, a 163% increase over the prior year. The increase in deal size has been an encouraging sign, given the rise in the cost of capital over the past two years. The growth in deal size resulted from the completion of several significant transactions during 2024, coupled with the overall increase in AUM levels due to market performance.

Another contributor to the increase in deal size has been RIAs partnering with private equity firms. According to Fidelity’s November 2024 Wealth Management M&A Transaction Report, private equity backing was involved in all of the M&A transactions reported in November. Noteworthy transactions backed by private equity in the fourth quarter include Pathstone’s acquisition of Hall Capital Partners. Hall Capital Partners is a leading independent investment and wealth management firm specializing in serving ultra-high-net-worth clients and has over $45 billion in assets under management. Pathstone, backed by Kelso & Co. and Lovell Minnick Partners, secured additional capital from both firms to fund the Hall Capital acquisition. The prevalence of serial acquirers and aggregators has continued in the RIA M&A market.

In recent years, the professionalization of the buyer market and the entrance of outside capital have driven demand and increased competition for deals. Serial acquirers and aggregators have increasingly contributed to deal volume, supported by dedicated deal teams and access to capital. Such firms accounted for approximately 69% of transactions through November of 2024. Focus Financial Partners, Beacon Pointe Advisors, Mercer Advisors, and Waverly Advisors all completed multiple deals in the fourth quarter of 2024.

Deal activity has also been supported by the supply side of the M&A equation, as the impetus to sell is often based on more than market timing. Sellers often look to solve succession issues, improve quality of life, and access organic growth strategies. Such deal rationales are not sensitive to the market environment and will likely continue to fuel the M&A pipeline even during market downturns.

Another potential catalyst for M&A activity is the Federal Reserve’s decision to cut interest rates. In September, the Fed implemented a 50-basis-point rate cut, followed by two additional cuts of 25 basis points each in November and December. This marks a shift after two and a half years of rate increases, which contributed to a slowdown in deal volume during that period. With expectations of further rate cuts ahead, cheaper capital would likely encourage more deal activity in the RIA M&A market. As capital becomes more accessible and consolidation trends continue, the RIA market could experience renewed momentum heading into 2025.

What Does This Mean for Your RIA?

For RIAs planning to grow through strategic acquisitions: Pricing for RIAs has trended upwards in recent years, leaving you more exposed to underperformance. Structural developments in the industry and the proliferation of capital availability and acquirer models will likely continue to support higher multiples than the industry has seen in the past. That said, a long-term investment horizon is the greatest hedge against valuation risks. Short-term volatility aside, RIAs continue to be the ultimate growth and yield strategy for strategic buyers looking to grow their practice or investors capable of long-term holding periods. RIAs will likely continue to benefit from higher profitability and growth than their broker-dealer counterparts and other diversified financial institutions.

For RIAs considering internal transactions: We’re often engaged to address valuation issues in internal transaction scenarios, where valuation considerations are top of mind. Internal transactions don’t occur in a vacuum, and the same factors driving consolidation and M&A activity have also influenced valuations in internal transactions. As valuations have increased, financing in internal transactions has become a crucial secondary consideration where buyers (usually next-gen management) lack the ability or willingness to purchase a substantial portion of the business outright. As the RIA industry has grown, so too has the number of external capital providers who will finance internal transactions. A seller-financed note has traditionally been one of the primary ways to transition ownership to the next generation of owners (and, in some instances, may still be the best option). Still, increasing bank financing and other external capital options can provide selling partners with more immediate liquidity and potentially offer the next-gen cheaper financing costs.

If you are an RIA considering selling: Whatever the market conditions are when you go to sell, it is essential to have a clear vision of your firm, its value, and what kind of partner you want before you go to market. As the RIA industry has grown, a broad spectrum of buyer profiles has emerged to accommodate different seller motivations and allow for varying levels of autonomy post-transaction. A strategic buyer will likely be interested in acquiring a controlling position in your firm and integrating a significant portion of the business to create scale. At the other end of the spectrum, a sale to a patient capital provider can allow your firm to retain its independence and continue operating with minimal outside interference. Given the wide range of buyer models, picking the right buyer type to align with your goals and motivations is a critical decision that can significantly impact personal and career satisfaction after the transaction closes.

About Mercer Capital

We are a valuation firm that is organized according to industry specialization. Our Investment Management Team provides valuation, transaction, litigation, and consulting services to a client base consisting of asset managers, wealth managers, independent trust companies, broker-dealers, PE firms and alternative managers, and related investment consultancies.