What Donald Trump’s Presidency Means to the Investment Management Industry

1971 Plymouth Satellite Wagon, similar to the one Carol Brady drove in The Brady Bunch (wagonation.com)

No doubt, 2016 will be remembered for two major left-tailed events – Brexit and the election of Donald Trump as President of the United States. In hindsight, the former should have been a clear suggestion of the latter, but even though some political wonks pointed that out, most of us were caught flat footed on both occasions.

I won’t devote this blogpost to a market outlook – there are plenty of those out there written by people more knowledgeable than I. The purpose of this blog is to consider the implications of the election for the investment management industry, which is no easy feat. The Trump campaign was generally heavy on rhetoric and light on policy details. The investment management industry rarely came up, other than when Trump suggested that he would advocate taxing carried interest returns as ordinary income. He never mentioned, for example, the DOL’s Fiduciary Rule, which is set to phase in three months after the inauguration.

The clearest indication of what a Trump presidency means to financial services, so far, appears to be its impact on the banking industry. The promise of a steepening yield curve and a pullback in portions of Dodd-Frank have sent bank valuations soaring since the election. If core banking is to become more profitable, banks will either a) be content with their basic operations and stop exploring diversification like asset management, or, b) feel comfortable enough with the outlook of their main business to look for avenues to diversify, like asset management.

The Certainty of Uncertainty (about Trump)

The striking thing about President-elect Trump is how little we know about him, despite the fact that he has been a very public figure for decades. He’s never held elected office, so he has no voting record. In the past, he’s been friendly and unfriendly with both political parties, and he ran his campaign in such a way that, despite being the Republican nominee, he has little, if any, debt to the Republican Party. This either empowers him to be pragmatic, or makes him a loose cannon.

We can expect Trump to be pro-growth, even if the price is spiraling deficits and inflation. He is, after all, primarily a real estate developer. Making money in real estate requires risk-taking financed by outsized leverage to create binary outcomes: profits or bankruptcy. After a career in that industry, and having been brought up in it by a father who practiced a similar craft, he’s unlikely to change his world view. Trump likely won’t be concerned about the consumer price index, either. Inflation doesn’t scare people who have appreciating hard assets on one side of their balance sheet and a fixed amount of debt on the other. This perspective is likely to create a lot of conflict with congressional Republicans, which will probably bother them more than Trump. Whatever comes of it, it is very unlikely that the President-elect will prove to be fiscally conservative.

Trump is also unlikely to prove to be socially conservative. He has spent his entire adult life in Midtown Manhattan, not exactly the sanctum sanctorum of the Moral Majority. Social issues, again, are not a subject of this blog, but because he has no stake in that soil, President Trump can use social issues as bargaining chips to entice legislators from both parties to support his agenda, once he clarifies what that agenda is. Because he is not an ideologue, President Trump will probably reveal his agenda one day at a time, which will be as fascinating to watch as it is maddening to invest around.

If these early indications prove correct, the looming Trump Presidency will be hard on segments of the fixed income community, and favorable to pro-volatility segments of the equity management world. Asset correlations are probably going to be much lower. All this suggests that active management will be back in style. It’s amazing sometimes what it takes to make a trend-line roll over.

What We Do Know (about Nationalism)

Exit polls strongly suggest that Trump was elected on a nationalist agenda. At the moment, the GOP thinks it controls the White House, and the Democrats feel disempowered. The truth appears to be more nuanced, as Trump fashioned his message around a careful (and, it turns out, accurate) reading of public sentiment rather than polls or party platforms.

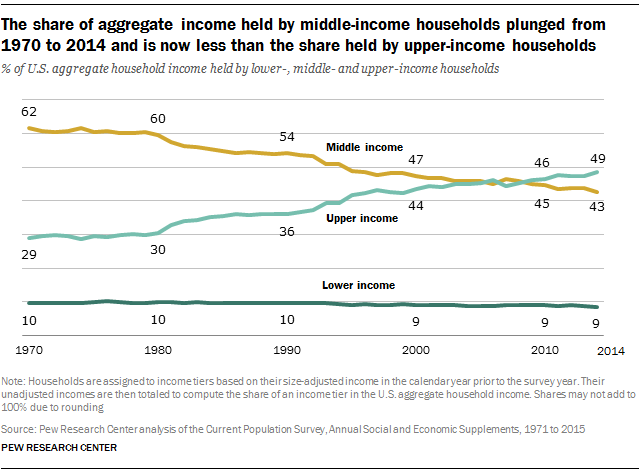

Much of Trump’s support comes from middle class voters whose standards of living have either not improved or have declined over the past thirty to forty years. At the same time, wealthy America has become much more so, and that disparity fueled resentment that led to this election outcome. There is ample research to suggest middle class America feels left out of both parties’ agenda. The Pew Research Center has done an exhaustive amount of study on the distribution of income and wealth in America. One such dataset notes that upper income households in America (those earning twice the median household income) now enjoy a greater share of aggregate U.S. household income than middle income households (defined as those earnings between two-thirds and double median household income). In the early 1970s, when U.S. middle class life was being celebrated by television shows like The Brady Bunch, middle income households collectively earned twice the amount of national income commanded by upper income households.

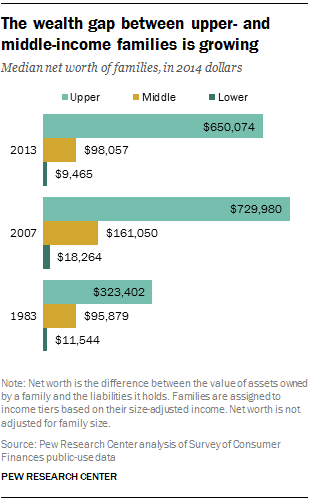

The trends in household wealth in the U.S. have been even more striking. The same Pew Research report looks at the median net worth of U.S. households since 1983 – not going back quite as far as the income portion of their study. In 1983, the median net worth of high income families was a little over three times that of middle income families. Fast forward 30 years to 2013, and that disparity doubled, to six and a half times. During that time, the median net worth of middle income families barely changed when adjusted for inflation, but the wealth of upper income households doubled. Also note that the credit crisis seems to have exacerbated this disparity; upper income households had a median net worth of approximately four times that of middle income households in 2007.

Further, as has been widely reported elsewhere, the increase in wealth concentration is greatest at the upper end. In an oft-cited study published last year by Berkeley professors Emmanuel Saez and Gabriel Zucman, the top one tenth of one percent of U.S. households held between 7% and 8% of household wealth in the 1970s. Less than forty years later, that share had tripled, with the wealthiest U.S. households owning around 22% of aggregate U.S. household wealth.

Middle income Americans may not read a lot of economic studies, but they sense they’ve been left behind by a changing economy; the data just confirms it. The 117 episodes of The Brady Bunch covered a wide variety of topics, but I don’t remember Mike and Carol Brady reviewing their wealth manager’s account statements and discussing whether or not they were GIPS compliant.

Needless to say, the growth of household income and wealth on the right-tail has been a boon to the RIA industry. Mean reversion might not be as generous to asset management. Assuming mean reversion, either the middle class is going to accumulate a lot of investible assets, or the wealthiest Americans are somehow going to become less so. The current nationalist fervor may be a cause of that, or may be just a barometer.

What We’ll Be Watching

In any event, it is difficult to imagine the election of a wealthy New York real estate developer leading to middle income families enjoying a greater share of national income and household wealth, but there are other possibilities that could cause wealth and income trendlines to mean-revert:

- Declining value of financial assets – Rising inflation and rising interest rates could result in a decline in fixed income and equity valuations, compressing the value of the primary wealth assets held by upper income households. This is obviously not bullish for RIAs.

- Rising interest rates – In a rising rate environment, borrowers are relatively better off, because fixed cost borrowing is, over time, below market. Symmetrically, lenders (those who save money and invest in interest bearing assets) are achieving returns that are chronically below market. Obviously, upper income households tend to be lenders, and middle income households tend to be borrowers.

- Increasing value of housing – All asset values are relative, and homes make up a greater proportion of household net worth for middle income families than upper income families. If housing appreciates (outside of the major U.S. markets where it already has), then wealth redistribution will improve.

- Taxes – Unlikely in a Trump administration, but higher taxes would probably fall disproportionately on upper income households. Again, this would not be bullish for the investment management industry.

- Inflation – Inflation is more likely to help wage earners than investors in many financial assets, and thus would cause some long standing economic trends to change.

The election of Donald Trump may forestall some of these changes while accelerating others, and the advent of new investment platforms like robo-advisors may help maintain industry revenues and margins if economics improve for middle income households relative to more wealthy Americans. What is difficult to debate, however, is that the RIA space has enjoyed a tailwind from certain economic trends over the past three or four decades that may not persist.

RIA Market is Favorable, so Far

As all readers of this blog know, when the election results started coming in differently than most expected, equity futures and global markets plummeted, and then recovered and rallied. Publicly traded investment management firms have seen significant increases in valuation since Election Day, with many up between 10% and 20%, so these notes about the potential challenges of economic nationalism don’t appear to be widely held.

All in all, though, with a Trump presidency the RIA community is faced with more unknowns than knowns, and despite what the president-elect said in his campaign, governing is very different than campaigning. The market’s performance so far suggests that most investors were relieved we once again had a peaceful transfer of power, and – whatever fight is coming – at least we’re in the fight.