The June BankWatch featured the first part of a series describing key considerations in the valuation of banks and bank holding companies. While that installment provided a general overview of key concepts, this month we pivot to the analysis of bank financial statements and performance.1 Unlike many privately held, less regulated companies, banks produce reams of financial reports covering every minutia of their operations. For analytical personality types, it’s a dream.

The approach taken to analyze a bank’s performance, though, must recognize depositories’ unique nature, relative to non-financial companies. Differences between banks and non-financial companies include:

Why do banks seek to acquire deposits? First, all earning assets must be funded; otherwise, the balance sheet would fail to balance. Ergo, more deposits allow for more earning assets. Second, retail deposits tend to cost less than other alternative sources of funds. Banks have access to wholesale funding sources, such as brokered deposits and Federal Home Loan Bank advances, but these generally have higher interest rates than retail deposits. Third, retail deposits are stable, due to the relationship existing between the bank and customer. This provides assurance to bank managers, investors, and regulators that a disruption to a wholesale funding source will not trigger a liquidity shortfall. Fourth, deposits provide a vehicle to generate noninterest income, such as service charges or interchange. The strength of a bank’s deposit portfolio, such as the proportion of noninterest-bearing deposits, therefore influences its overall profitability and franchise value.

Capital adequacy requirements have several influences on banks. Most importantly, failing to meet minimum capital ratios leads to severe repercussions, such as limitations on dividends and stricter regulatory oversight, and is (as you may imagine) deleterious to shareholder value. More subtly, capital requirements influence asset pricing decisions and balance sheet structure. That is, if two assets have the same interest rate but different risk weights, the value maximizing bank would seek to hold the asset with the lower risk weight. Stated differently, if a bank targets a specific return on equity, then the bank can accept a lower interest rate on an asset with a smaller risk weight and still achieve its overall return on equity objectives.

We now cover several components of a bank’s balance sheet.

Banks are, by their nature, engaged in liquidity transformation, whereby funds that can be withdrawn on demand (deposits) are converted into illiquid assets (loans). Several alternatives exist to mitigate the risk associated with this liquidity transformation, but one universal approach is maintaining a portfolio of on-balance sheet liquid assets. Additionally, banks maintain securities as a source of earning assets, particularly when loan demand is relatively limited.

Liquid assets generally consist of highly-rated securities issued by the U.S. Treasury, various governmental agencies, and state and local governments, as well as various types of mortgage-backed securities. Relative to loans, banks trade off some yield for the liquidity and credit quality of securities. Key analytical considerations include:

A typical bank generates most of its revenue from interest income generated by the loan portfolio; further, the lending function presents significant risk in the event borrowers fail to perform under the contractual loan terms. While loans are more lucrative than securities from a yield standpoint, the cost of originating and servicing a loan portfolio – such as lender compensation – can be significant. Key analytical considerations include:

Banks maintain reserves against loans that have defaulted or may default in the future. While a new regime for determining the ALLL will be implemented beginning for some banks in 2020, the size of the ALLL under current and future accounting standards generally varies between banks based on (a) portfolio size, (b) portfolio composition, as certain loan types inherently possess greater risk of credit loss, (c) the level of problem or impaired loans, and (d) management’s judgment as to an appropriate ALLL level. Calculating the ALLL necessarily includes some qualitative inputs, such as regarding the outlook for the economy and business conditions, and reasonable bankers can disagree about an appropriate ALLL level. Key analytical considerations regarding the ALLL and overall asset quality include:

As for loans, bank financial statements distinguish several deposit types, such as demand deposits and CDs. It is useful to decompose deposits further into retail (local customers) and wholesale (institutional) deposits. Key analytical considerations include:

Historical changes in equity cannot be understood without an equity roll-forward showing changes due to retained earnings, share sales and redemptions, dividends, and other factors. In our opinion, it is crucial to analyze the bank’s current equity position by reference to management’s business plan, as this will reveal amounts available for use proactively to generate shareholder returns (such as dividends, share repurchases, or acquisitions). Alternatively, the analysis may reveal the necessity of either augmenting equity through a stock offering or curtailing growth objectives.

The computation of regulatory capital metrics can be obtained from a bank’s regulatory filings. Relative to shareholders’ equity, regulatory capital calculations: (a) exclude most intangible assets and certain deferred tax assets, and (b) include certain types of preferred stock and debt, as well as the ALLL, up to certain limits.

There are six primary components of the bank’s income statement:

The previous analysis of the balance sheet foreshadowed this net interest income discussion with one important omission – the external interest rate environment. While banks attempt to mitigate the effect on performance of uncontrollable factors like market interest rates, some influence is unavoidable. For example, steeper yield curves generally are more accommodative to net interest income, while banks struggle with flat or inverted yield curves.

Another critical financial metric is the net interest margin (“NIM”), measured as the yield on all earning assets minus the cost of funding those assets (or net interest income divided by earning assets). The NIM and net interest income are influenced by the following:

The sensitivity of net interest income to uncontrollable forces – i.e., market interest rates – makes noninterest income attractive to bankers and investors. Banks generate noninterest income from a panoply of sources, including:

Some sources of revenue can be even more sensitive to the interest rate environment than net interest income, such as income from residential mortgage originations. Yet other sources have their own linkages to uncontrollable market factors, such as revenues from wealth management activities tied to the market value of account assets.

Expanding noninterest income is a holy grail in the banking industry, given limited capital requirements, revenue diversification benefits, and its ability to mitigate interest rate risk while avoiding credit risk. However, many banks’ fee income dreams have foundered on the rocks of reality for several reasons. First, achieving scale is difficult. Second, cross-sales of fee income products to banking customers are challenging. Third, significant cultural differences exist between, say, wealth management and banking operations. A fulsome financial analysis considers the opportunities, challenges, and risks presented by noninterest income.

In a mature business like banking, expense control always remains a priority.

We covered this income statement component previously with respect to the ALLL.

Banks generally report effective tax rates (or actual income tax expense divided by pre-tax income) below their marginal tax rates. This primarily reflects banks’ tax-exempt investments, such as municipal bonds; bank-owned life insurance income; and vehicles that provide for tax credits, like New Market Tax Credits. It is important to note that state tax regimes may differ for banks and non-banks. For example, some states assess taxes on deposits or equity, rather than income, and such taxes are not reported as income tax expense.

As the preceding discussion suggests, many levers exist to achieve shareholder returns. One bank can operate with lean expenses, but pay higher deposit interest rates (diminishing its NIM) and deemphasize noninterest income. Another bank may pursue a true retail banking model with low cost deposits and higher fee income, offset by the attendant operating costs. There is not necessarily a single correct strategy. Different market niches have divergent needs, and management teams have varying areas of expertise. However, we still can compare the returns on equity (or net income divided by shareholders’ equity) generated by different banks to assess their relative performance.

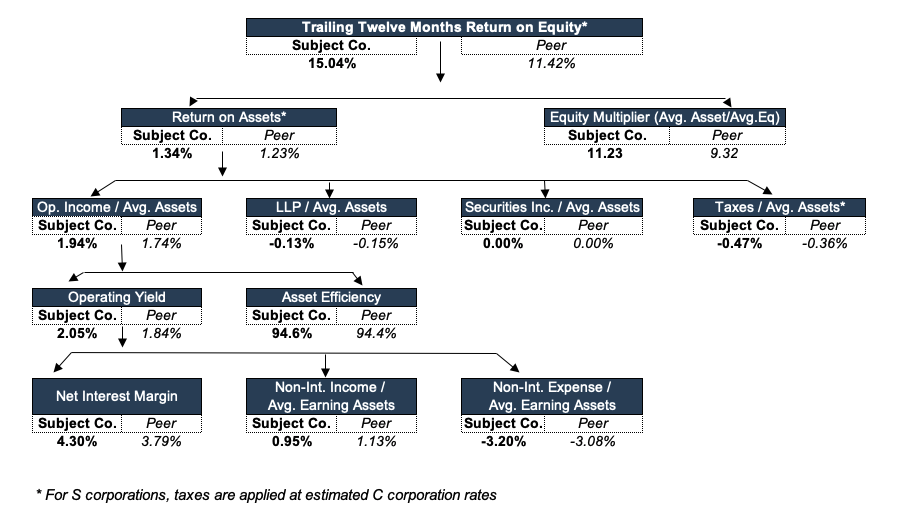

The figure below presents one way to decompose a bank’s return on equity relative to its peer group. This bank generates a higher return on equity than its peer group due to (a) a higher net interest margin, (b) a slightly lower loan loss provision, and (c) higher leverage (shown as the “equity multiplier” in the table).

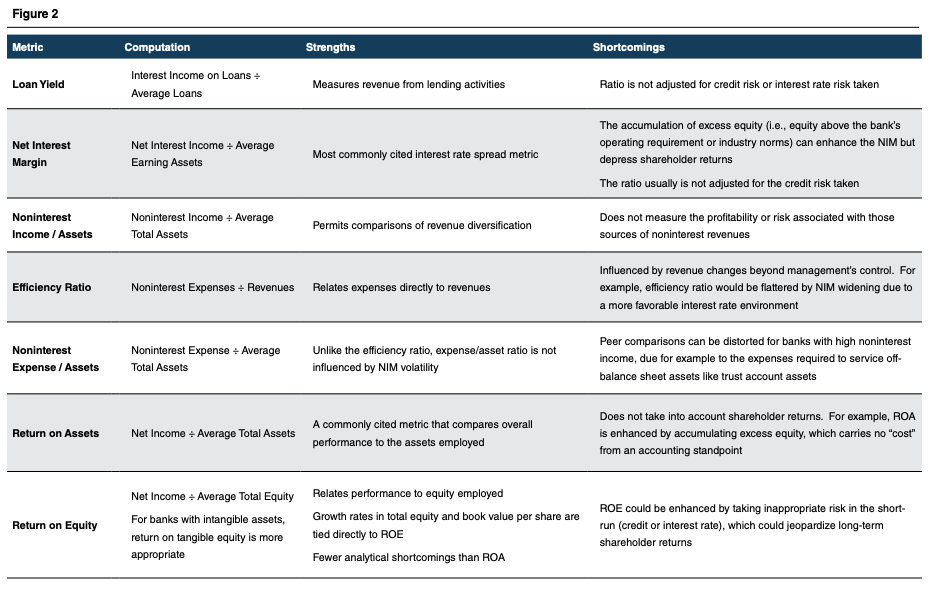

The figure below cites several common income statement metrics used by investors, as well as their strengths and shortcomings.

Banks file quarterly Call Reports, which are the launching pad for our templated financial analyses. Depending on asset size, bank holding companies file consolidated financial statements with the Federal Reserve. All bank holding companies, small and large, file parent company only financial statements, although the frequency differs. Other potentially relevant sources of information include:

A rigorous examination of the bank’s financial performance, both relative to its history and a relevant peer group and with due consideration of appropriate risk factors, provides a solid foundation for a valuation analysis. As we observed in June’s BankWatch, value is dependent upon a given bank’s growth opportunities and risk factors, both of which can be revealed using the techniques described in this article.

1 Given the variety of business models employed by banks, this article is inherently general. Some factors described herein will be more or less relevant (or even not relevant) to a specific bank, while it is quite possible that, for the sake of brevity, we altogether avoided mention of other factors relevant to a specific bank. Readers should therefore conduct their own analysis of a specific bank, taking into account its specific characteristics.

Originally published in Bank Watch, August 2019.