This article summarizes Mercer Capital’s whitepaper, Valuing a Business for Estate Planning Purposes During a Transaction, which addresses the complex intersection of business valuations and estate planning when M&A processes are underway.

Estate planning for business owners becomes much more complicated when a merger or acquisition process is underway. IRS guidance suggests requirements that business valuations for transfer tax purposes must consider all knowable facts as of the valuation date—including pending transaction processes. This creates both opportunities and risks for estate planners working with clients who own businesses actively engaged in sale discussions.

The challenge lies in determining how much weight to assign to potential deal proceeds versus traditional standalone valuations at different stages of the M&A process. While early-stage processes may warrant minimal consideration of transaction value, later stages with formal offers require greater weighting of expected proceeds. Understanding the nuances of an engagement of this type is essential for avoiding costly mistakes and ensuring credible valuations that optimize estate planning outcomes.

The intersection of business transactions and estate planning presents one of the most complex challenges in wealth transfer strategies. When business owners—whose enterprises often represent the majority of their wealth—simultaneously pursue exit opportunities and engage in estate planning, the valuation considerations become particularly intricate and consequential.

In Chief Counsel Advice 202152018 (“CCA 202152018”), the IRS addressed two issues in the context of a business owner who funded a GRAT during an active sale process. First, it considered whether hypothetical willing buyers and sellers would take into account a pending merger when valuing stock for gift tax purposes. The Service answered affirmatively: under the fair market value standard, known or knowable facts—including an ongoing sale process and offers already received—must be incorporated into valuation. Second, the IRS considered whether the donor retained a “qualified annuity interest” under §2702 when the GRAT was funded using a stale §409A appraisal that ignored the pending merger. The Service held that the retained interest failed to qualify, treating the entire transfer to the GRAT as a taxable gift.

The facts of the case reveal a pattern of valuation inconsistencies. The taxpayer used a seven-month-old §409A appraisal—prepared for deferred compensation purposes, not transfer tax purposes—to support the GRAT funding, even though multiple offers had already been received at higher prices. Shortly thereafter, however, the same taxpayer funded a charitable remainder trust using a contemporaneous qualified appraisal that reflected the higher offer price. This inconsistency, coupled with reliance on an outdated and contextually inappropriate appraisal, invited IRS scrutiny and resulted in the Service’s determination that the GRAT was fatally flawed.

While CCAs do not carry precedential weight, they are instructive of how the IRS is likely to approach similar fact patterns. CCA 202152018 signals heightened IRS vigilance where GRATs or other transfer tax strategies are executed amidst an ongoing or foreseeable liquidity event. It highlights the necessity of contemporaneous, purpose-appropriate appraisals that consider all relevant facts at the valuation date. Failure to do so risks not only valuation adjustments but also possible disqualification of retained interests under §2702, leading to the result of treating the entire transfer as a taxable gift.

To properly value businesses during transaction processes, estate planners must understand the typical stages of mergers and acquisitions. The process generally unfolds through six distinct phases, each presenting different levels of transaction certainty and information availability.

During the planning phase, when owners hire M&A advisors and organize information, there may be little quantifiable expectation of proceeds. However, once confidential information memorandums are distributed to potential buyers, expectations around selling prices become clearer. As the process progresses through qualification phases with indications of interest, buyer selection with letters of intent, due diligence, and final negotiations, the probability of completion and the certainty of proceed size generally increase.

The critical insight for estate planners is that valuation weight should shift toward transaction proceeds as deal certainty increases. A business in early marketing phases might warrant only modest consideration of potential proceeds, while a company with binding letters of intent is more likely to merit substantial weighting of expected transaction value.

Understanding transaction success rates provides crucial context for valuation decisions. In a McKinsey & Company analysis of over 2,500 large deals valued above €1 billion, approximately 10.5% of deals were canceled, with larger transactions facing higher failure risks. Deals exceeding €10 billion experienced cancellation rates above 20%, while those under €5 billion maintained consistent 10% annual cancellation rates.

In this analysis, industry factors significantly impacted success probability. Energy and financial sector deals showed the lowest cancellation rates at around 7%, while consumer discretionary and communications services faced higher failure rates of 13% and 19% respectively. Nearly 75% of canceled deals failed due to price expectations, regulatory concerns, or political issues.

However, these statistics apply primarily to publicly announced transactions, making them most relevant for closely held companies in later deal stages. Earlier-phase failures often remain private, suggesting estate planners should shift weight toward no-sale scenarios when businesses are in preliminary transaction stages.

Several factors influence deal completion probability and should inform valuation weightings. Expected deal timelines matter significantly—longer processes face higher failure rates. Deal structure complexity creates additional risk, as mixed cash-and-stock transactions prove less successful than simpler all-cash or all-stock arrangements.

The number and quality of bidders affect completion likelihood. Multiple interested parties provide fallback options, though this dynamic can shift if secondary bidders lose interest. More sophisticated bidders, such as private equity firms or strategic acquirers with dedicated M&A teams, typically conduct more thorough early evaluation but also identify issues that might derail transactions.

External factors including economic conditions, political stability, and regulatory environment all influence completion probability. Companies with clean financial records, predictable cash flows, and minimal discretionary items in recent results face higher completion probabilities due to reduced due diligence risks.

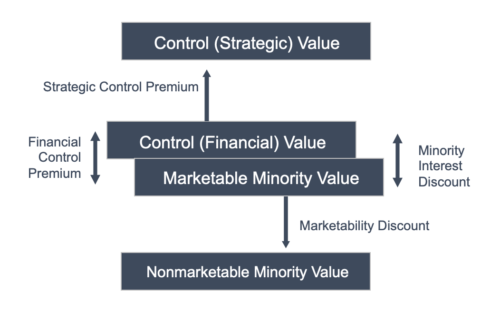

Business owners and their professional advisors are occasionally perplexed by the fact that their shares can have more than one value. This multiplicity of values is not a conjuring trick on the part of business valuation experts, but simply reflects the economic fact that different markets, different investors, and different expectations necessarily lead to different values.

Business valuation experts use the term “level of value” to refer to these differing perspectives. As shown in the figure below, there are three basic “levels” of value for a business.

Estate planning transfers typically involve minority interests valued at the nonmarketable minority level, which may incorporate discounts for lack of control and marketability. In contrast, M&A transactions occur at control levels and may include strategic premiums for synergies.

This creates significant value gaps. A business with $100 per share marketable minority value might be valued at $65 per share for estate planning purposes after appropriate discounts. However, strategic buyers might pay $130 per share, creating a substantial differential between transfer values and transaction proceeds.

Expected transaction proceeds require careful analysis beyond headline multiples. Deal terms may include earn-outs, contingent payments, or non-cash consideration that should be risk-adjusted and converted to cash equivalency. The proposed transaction could trigger corporate-level taxes that would need to be considered in valuing an equity interest. A transaction appearing to price at 12x EBITDA might only deliver 9x value on a cash-equivalent basis after considering payment timing, corporate taxes, and performance risks.

Estate planners working with businesses in transaction processes should expect valuation frameworks that appropriately weight no-sale scenarios against expected proceeds based on process stage and specific circumstances.

As transaction processes progress through marketing phases with distributed information memorandums, modest weighting of expected proceeds becomes appropriate, though determining precise allocations requires careful analysis of company-specific factors and buyer interest levels.

Once formal indications of interest are received, increasing weight is likely to shift toward transaction proceeds, with the specific allocation depending on offer quality, buyer sophistication, and deal structure. By the time binding letters of intent are executed, substantial weighting of expected proceeds is typically warranted, though some consideration of failure scenarios remains appropriate until closing occurs.

The IRS guidance emphasizes that valuations should ideally use valuation dates matching transfer dates and consider all knowable facts. Using outdated appraisals prepared for other purposes creates significant compliance risks, particularly when those appraisals ignore ongoing transaction processes. Business appraisers should document their consideration of transaction processes and provide clear rationale for their weighting decisions.

Understanding these dynamics enables more effective estate planning strategies. Business owners contemplating both exit strategies and wealth transfer can time their planning to optimize valuations while maintaining compliance. Earlier transfers in transaction processes may capture lower valuations, though this must be balanced against deal completion risks and the potential for significant value increases.

The complexity of these valuations underscores the importance of engaging qualified professionals who understand both IRS transfer tax requirements and M&A market dynamics. Estate planners need valuation specialists who can navigate the technical requirements while providing credible opinions that optimize client outcomes.

The intersection of business transactions and estate planning presents both opportunities and pitfalls for wealth transfer strategies.

Success in this complex environment requires understanding M&A process stages, deal success factors, valuation methodologies, and compliance requirements. Estate planners who understand these concepts can help business owners navigate simultaneous exit and wealth transfer strategies while avoiding the costly mistakes that have drawn IRS scrutiny.

The stakes are significant—business interests often represent the majority of owner wealth, making proper valuation essential for effective estate planning. With careful planning, appropriate professional guidance, and an understanding of regulatory guidance, these complex situations can be managed successfully to achieve both transaction and estate planning objectives.

With 40+ years of transfer tax valuation and M&A experience, Mercer Capital understands the complexities that arise when business transactions intersect with estate planning objectives. Our team of credentialed professionals has worked with numerous clients through these challenging scenarios, providing the expertise necessary for these engagements.

For estate planners seeking experienced partners who can navigate the intricate requirements of valuing businesses during active transaction processes, Mercer Capital offers the depth of experience and technical proficiency that these engagements demand.