During the divorce process, a listing of assets and liabilities, often referred to as a marital balance sheet or marital estate, is established for the purpose of dividing assets between the divorcing parties. Some assets are easily valued, such as a brokerage account or retirement, which hold marketable securities with readily available prices. Other assets, such as a business or ownership interest in a business, are not as easily valued and require the expertise of a business appraiser. Upon retaining a valuation or financial expert, together with the family law attorney, it is important to understand and agree upon certain factors that set forth a baseline for the valuation. These may be state specific, such as case precedent and state statute. One of these considerations is the valuation date, which differs from state to state.

Valuation Date Defined

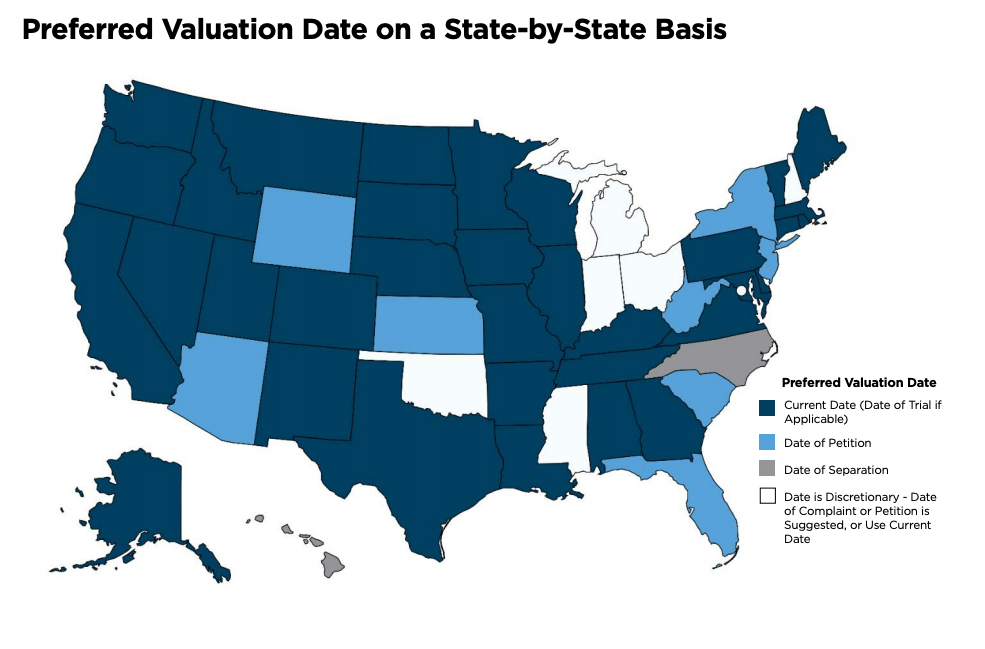

The valuation date represents the point in time at which the business, or business interest(s), is being valued. The majority of states have adopted the use of a current date, usually as close as possible to mediation or trial date. Other states use date of separation or the date the divorce complaint/petition was filed. See the map on page 2 for a preferred valuation date summary by state (note that the summary may be modifiable for recent updates in state precedent). Those states that use date of separation or date of complaint/ petition as the valuation date face a bit of “noise” and complexity when the divorce process becomes lengthy and/or when there are significant impacts to the economy and/or industry in which that business operates. As an example, consider the timeframe from December 31, 2019 to now, Summer 2020, and the economic reverberation of COVID-19. A valuation as of these two dates will look quite different due to changes in actual business performance as well as shifts in future expectations/outlooks for the business and its industry. However, this is not only a consideration for those states which use date of separation or date of petition. This is also an important consideration for matters which have extended over a prolonged period. It is also critical for current matters – we are all aware that much has transpired since December 31, 2019 – as that valuation date may no longer accurately reflect the overall picture of the business, necessitating a secondary valuation, or alternatively, an update to the prior valuation. Let’s take a deeper dive at understanding the importance of valuation date as it relates to the divorce process.

Why Does the Valuation Date Matter?

Laws differ state to state regarding valuation date and standard of value (generally fair market value or fair value). There are other nuances related to the business valuation for divorce process, such as premise of value which is often a going-concern value as opposed to a liquidation value. After the standard of value, premise of value, and the valuation date have been established, the business appraiser must then incorporate relevant known and knowable facts and circumstances at the date of valuation when determining a valuation conclusion. These facts and trends are reflected in historical financial performance, anticipated future operations, and industry/economic conditions and can fluctuate depending on the date of valuation.

Using our prior example, the conditions of Summer 2020 are vastly different than year-end 2019 due to COVID-19. For many businesses, actual performance financial performance in 2020 has been materially different than what was expected for 2020 during December 2019 budgeting processes. The current environment has made the facts and circumstances in anticipated future budget(s), both short-term and long-term, even more meaningful. The income approach reflects the present value of all future cash flows. So, even if a business is performing at lower levels today, that may not necessarily be a permanent impact, particularly if rebound is anticipated. Thus, that value today may be impacted by a short-term decrease in earnings; however, an anticipated future rebound will also impact the valuation today. It must be pointed out that it would be incorrect to consider the impact of COVID-19 for a valuation date prior to approximately March 2020, as the economic impact of the pandemic was not reasonably known or knowable prior to that date. Therefore, the valuation date is meaningful and a significant consideration in any valuation process, and especially in current conditions. A state that typically requires a date of separation may consider consensus among parties to update to a more recent date as much has changed between then and now.

How Have Valuations Been Affected by COVID-19?

Valuations of any privately held company involve the understanding and consideration of many factors. We try to avoid absolutes in valuations such as always and never. The true answer to the question of how have valuations of privately held companies been affected by the coronavirus is “It Depends.”

- It depends on what industry the business operates in and how that industry has been impacted (whether negatively or positively) by COVID-19 conditions.

- It depends on where the subject company is geographically as we are seeing timing impacts from openings/closures differ throughout the country and globally.

- It depends on what markets the subject company serves. As we have seen and are continuing to see across the country, the stay-at-home restrictions have varied greatly from state to state and certain areas have been more severely affected than other. Certain industries, such as airlines, hospitality, retail, and restaurants, have been far more impacted than other industries.

As a general benchmark, the overall performance of the stock market from the beginning of 2020 until now can serve as a guide. The stock market has been volatile since the March global impact from COVID-19 began to unfold. Specific indicators of each subject company, such as actual performance and the economic/industry conditions relative to their geographic footprint, also govern the impact of any potential change in valuation.

Valuation Date Considerations for Lengthy Processes

The valuation date for purposes of business valuation for marital dissolution is an important issue, even in times without the current COVID-19 conditions. Consider matters that extend into multiple years from time of separation to time of divorce decree. Has the value of the business changed during this time? If the answer is yes, or maybe, another consideration for some clients may be related to the cost of another valuation. However, the importance of an accurate and timely valuation should far outweigh the concerns of additional expense to update a conclusion. It is important to discuss these elements with your expert as the process may depend on the length of time which has transpired since the original valuation and the facts and circumstances of the business/economy/industry. Your expert will be able to determine if an acceptable update may be simply updating prior calculations; however, if much has changed, such as expectations for the future performance of the business, the approach may involve a secondary valuation using a current date of valuation. Another consideration to keep in mind: depending on jurisdiction, state law may deem the value of the business after separation but before divorce as separate property. If this is the case, two valuation dates are necessary.

Concluding Thoughts

The litigation environment is complex and already rife with doom and gloom expectations. We have previously written about the phenomenon referred to as divorce recession in family law engagements. Understanding the valuation date of an asset valuation, such as a privately held business, for marital dissolution is an important consideration, especially for matters which have extended over a lengthy time and those that may be impacted by significant global events such as COVID-19. Speak to your valuation expert when these matters arise. The already complex process of business valuation becomes even more complex with the passing of time and also in the midst of economic uncertainty.