Carried Interest Explained

What is carried interest? It is the profits interest that a private equity, venture capital, or hedge fund principal receives if the fund exceeds certain performance benchmarks. Carried interest can also be referred to as performance allocation, incentive allocation, or promote interest in the case of real estate funds. Separately, fund principals also receive income and potential distributions from management fees and direct investments in the fund.

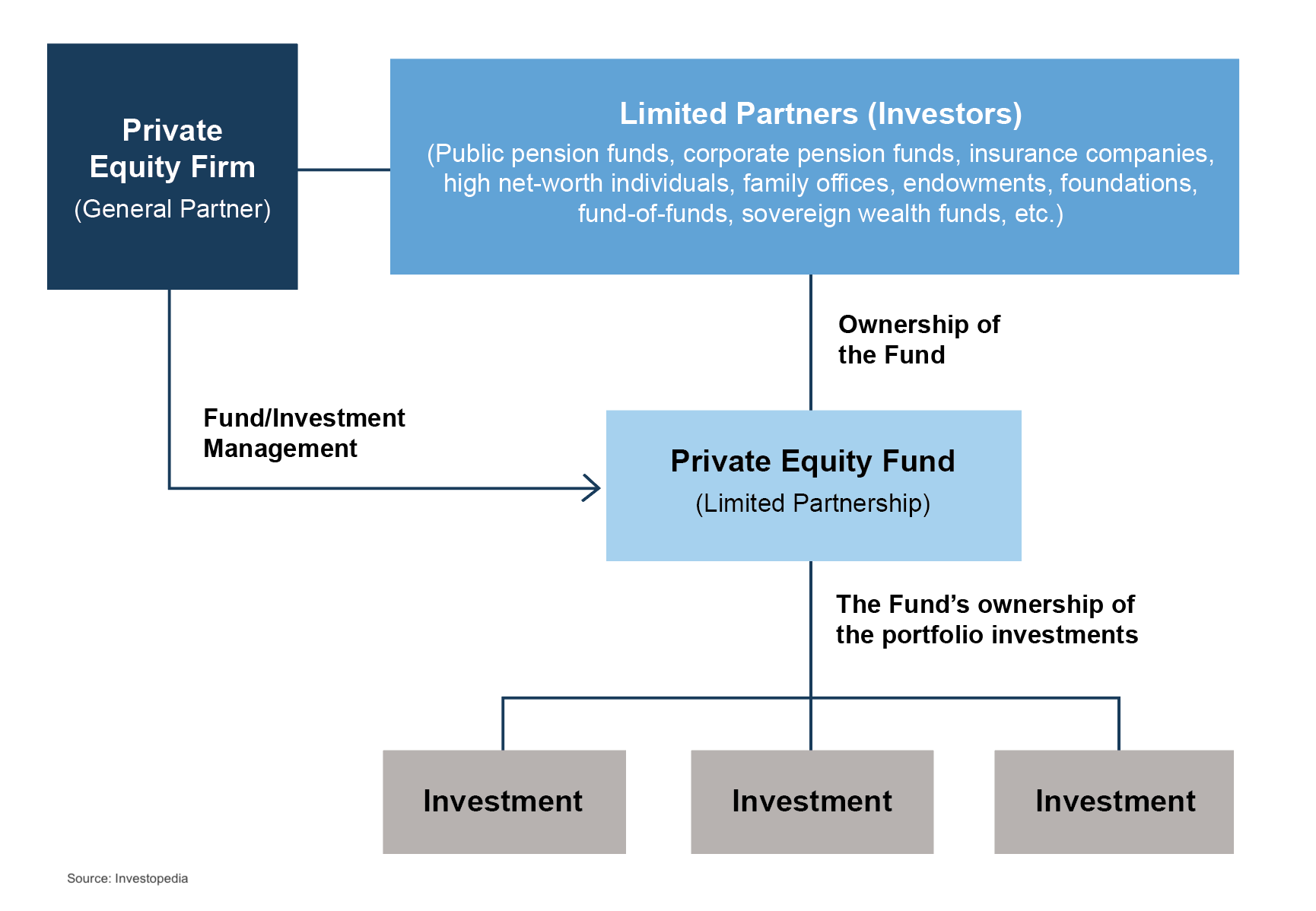

Fund Structures and Carried Interest Allocation

A basic private equity fund structure is shown below. Typically, the fund principals form a general partner entity and a management company entity. The principals then raise capital from limited partners and make investments over the term of the fund. The management company receives management fees, often around 2% per year, for investment management services provided. The general partner entity typically invests alongside the limited partners and would receive its pro-rata share of returns along with the limited partners. If the fund exceeds certain benchmarks, the general partner would also receive carried interest, often around 20% of fund returns beyond the benchmark.

It is important to note that private equity fund structures come in many forms, from basic to complex. Even though this article is focused primarily on private equity funds, similar concepts apply to certain hedge funds and venture capital funds.

Navigating Uncertainty and Valuation Challenges

Uncertainty exists regarding the fund’s performance, typically more so earlier in the fund’s life. When the fund entities are formed, and before capital is raised, there is also uncertainty regarding how much capital will be raised. These uncertainties result in lower values for the fund entities at inception. The fund entity values will increase throughout the life of the fund if the fund is able to successfully raise capital and achieve investment returns beyond the benchmark to generate carried interest cash flows.

At inception, the values of the fund entities will be relatively low, particularly the value of potential carried interest. As the fund raises capital and then begins to make investments, the values of the fund entities will change, potentially significantly.

Challenges in Valuing Interests in Fund Entities

A appraisal prepared by a qualified appraiser with prerequisite experience is paramount when determining the value of fund entity interests given the complexity involved. In addition to fund structure, other items that require appraiser familiarity with carried interest include the following:

- Fundraising: For new funds, what is the fund’s target size? And will the fund offer special terms for early investors or for a large “anchor” investor? For funds already operating, how much capital has been raised and how much additional capital does the fund expect to raise? And are there different classes of investors with different terms?

- Fund investment strategy: For new funds, what types of investments will the fund make in terms of asset classes, industries, size of interests, number of investments, etc.? How will the fund’s investments shape expected returns for the fund? What is the expected holding period for the fund’s investments? Will capital from the sales of investments be reinvested? Will the fund use leverage? And for funds already operating, what types of investments does the fund hold? What have the returns been to date? What is the outlook for the fund’s investments in terms of future returns and remaining holding periods?

- Fund terms: How is the management fee calculated and how often will it be assessed? Who will pay for fund expenses? Is there a general partner catch-up after the hurdle is reached? Are distributions made on a deal-by-deal basis, or on a cumulative basis? Can the general partner waive management fees associated with their direct investments in the fund? And for funds already operating, has any carried interest been accrued yet?

Funds already operating can be more complicated to value than new funds. In addition to understanding all of these items, the fund’s performance to date has to be reconciled with expectations going forward.

TIP: For new funds, the Private Placement Memorandum will typically be a good starting point to answer many of these questions. Additionally, governing documents for the limited partnership, the general partnership, the management company, and any other entities related to the fund will be useful. For existing funds, financial statements for each of the entities are needed to value the entities, in addition to the information needed for new funds.

Conclusion

In conclusion, valuing fund entities, including carried interest, in newly formed or existing funds requires a complex and thorough analysis. It is essential to work with qualified appraisers familiar with the complexities of fund structures, tax regulations, and local matrimonial law statutes to ensure optimal outcomes. Engaging with experienced advisors can increase the likelihood of an equitable outcome in divorce.

The professionals at Mercer Capital have experience in the valuation of carried interests. For more information or to discuss a valuation issue, feel free to contact us.