In our view, Employee Stock Ownership Plans (ESOPs) are an important omission in the current financial environment as a number of companies and banks lack a broader, strategic understanding of the possible roles of ESOPs as a tool to manage a variety of strategic issues facing community banks. Given the strategic challenges facing community banks, we strive to help our clients, as well as the broader industry, fill this gap, and discuss some common questions related to ESOPs in the following article.

We will be glad to discuss your bank’s current situation as well as the role an ESOP can play in detail. If you are interested in learning more about ESOPs, read our book, The ESOP Handbook for Banks: Exploring an Alternative for Liquidity and Capital While Maintaining Independence. In addition, if you would like to speak to a Mercer Capital professional, contact Jay Wilson at 901.685.2120 or wilsonj@mercercapital.com.

For those less familiar with ESOPs, we answer a few basic questions related to ESOPs. For those more familiar with ESOPs, skip to the question entitled “How can an ESOP help the bank deal with strategic issues?”.

ESOPs are a written, defined contribution retirement plan, designed to qualify for some tax-favored treatments under IRC Section 401(a). While similar to a more typical profit-sharing plan, the fundamental difference is that the ESOP must be primarily invested in the stock of the sponsoring company (only S or C corporations). ESOPs can acquire shares through employer contributions (either in cash or existing/newly issued shares) or by borrowing money to purchase stock (existing or newly issued) of the sponsoring company. Once holding shares, the ESOP obtains cash via sponsor contributions, borrowing money, or dividends/distributions on shares held by the ESOP. When an employee exits the plan, the sponsoring company must facilitate the repurchase of the shares, and the ESOP may use cash to purchase shares from the participant. Following repurchase, those shares are then reallocated among the remaining participants.

Similar to other profit-sharing plans, contributions (subject to certain limitations) to the ESOP are tax-deductible to the sponsoring company. The ESOP is treated as a single tax-exempt shareholder. This can be of particular benefit to S corporations, as the earnings attributable to the ESOP’s interest in the sponsoring company are untaxed. The tax liability related to ESOP planholder’s accounts is at the participant level and generally deferred similar to a 401(k) until employees take distributions from the plan.

Both publicly traded and private banks/holding companies (C or S-Corps.) can sponsor ESOPs, but the benefits are often more profound for private institutions that are not as actively traded, as the ESOP can promote a more active market and enhance liquidity more for the privately-held shares.

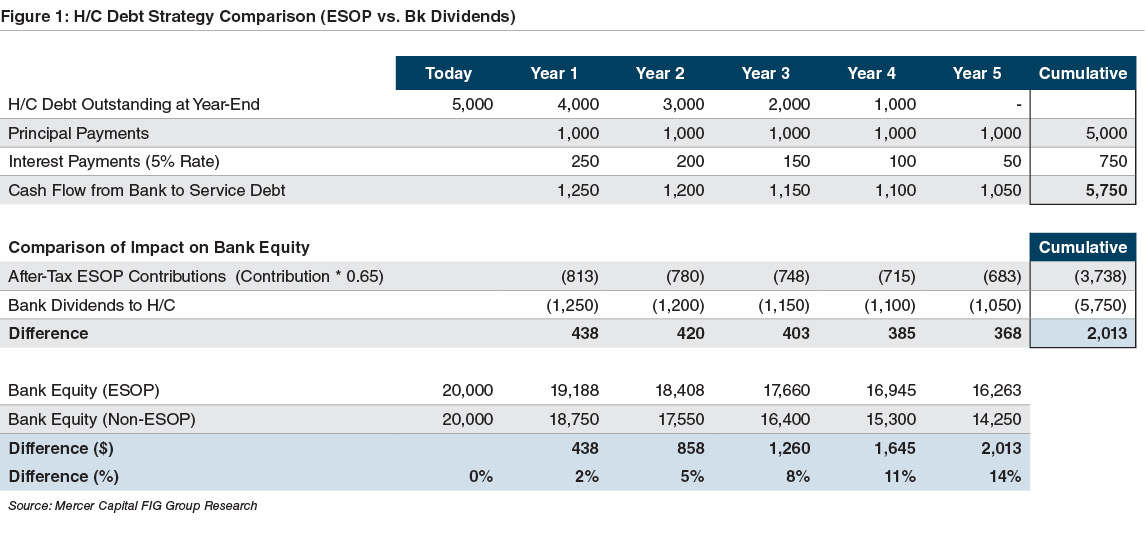

While not suitable in all circumstances, an Employee Stock Ownership Plan may provide assistance in resolving a number of strategic issues facing community banks and can offer benefits to plan participants, existing shareholders, and the sponsor company, including:

For those considering implementing ESOPs, the first step is generally a feasibility study of what the ESOP would actually look like once implemented at your bank. Parts of the study would include determining the value of the company’s shares, the pro-forma implications from the potential transaction/installation, as well as what after-tax proceeds the seller might expect. This will help determine whether the bank should proceed, wait a few years to implement, or move to another strategic option. There are typically a number of parties involved in implementations including among others an appraiser/valuation provider, trustee, attorney or plan designer, and administrative committee.

ESOPs are subject to both tax and benefit law provisions (such as the ERISA act of 1974). Certain negatives associated with them can include:

For existing ESOPs, two recent legal and regulatory developments have brought up important issues for trustees to consider as well.

In 2014, the Supreme Court ruled on the case of Fifth Third Bancorp v. Dudenhoeffer, which involved a public company that matched employee contributions to a 401(k) plan by contributing employer stock to an ESOP that was part of the plan. The ruling states that the standard of prudence applicable to all ERISA fiduciaries also applies to ESOPs, though ESOP fiduciaries are not required to diversify the ESOP’s holdings. The Court ruling was focused on public company ESOPs, but its implications for private company ESOPs are unclear. However, trustees should consider ensuring an investment policy statement is in place for the ESOP, stating that the policy is to invest primarily in employer stock in accordance with the purpose of the Plan; and, if applicable, the policy statement could potentially clarify that employees have diversification options through other benefit plans such as a 401(k) plan.

Scrutiny related to ESOPs, particularly as it relates to certain valuation issues, has increased in recent years, with the DOL bringing a number of cases against trustees and other parties. In the case of Perez, Secretary of the DOL v. GreatBanc Trust Company, there is a process agreement that we encourage ESOP companies and their trustees to review. While the process requirements are only specific to GreatBanc, the case has received a lot of attention in the ESOP community.

In October 2012, The U.S. Department of Labor filed a lawsuit against GreatBanc Trust Co. and Sierra Aluminum Co. in the U.S. District Court for the Central District of California. Among other issues identified in the suit, the DOL alleged that GreatBanc violated the Employee Retirement Income Security Act by breaching its fiduciary duties to the Sierra Aluminum Employee Stock Ownership Plan when it allowed the plan to pay more than fair market value for employer stock in June 2006. The suit also named the ESOP’s sponsor, Sierra Aluminum, as a defendant. The sponsor’s indemnification agreement with GreatBanc allegedly violated ERISA regulations. The suit focuses on the quality of the appraisal on which the trustee relied, particularly on the supportability of the assumptions used in the cash flow projection.

As part of the settlement negotiations, the DOL and GreatBanc have agreed upon a specific set of policies and procedures as trustee of an ESOP. While specific to GreatBanc, the transaction procedures are presumed to be applicable to all Trustees and related appraiser relationships. The process requirements cover the following areas:

In general, the process agreement makes clear that trustees must ensure that ESOP valuations are well documented with thoroughly supported assumptions.

Mercer Capital has been providing ESOP appraisal services for over 25 years and has extensive ESOP experience through providing annual valuations, installation advisory, feasibility studies, financial expert services related to legal disputes, and fairness opinions. Our appraisals are prepared in accordance with the Employee Retirement Income Security Act (“ERISA”), the Department of Labor, and the Internal Revenue Service guidelines, as well as Uniform Standards of Professional Appraisal Practice (“USPAP”). We are active members of The ESOP Association and the National Center for Employee Ownership (NCEO). Our professionals have been frequent speakers on topics related to ESOP valuation throughout our 32-year history. Mercer Capital professionals also co-authored the publication, The ESOP Handbook for Banks (2011), which provides insight into key ESOP-related issues affecting banking organizations.

For additional ESOP resources, view our whitepapers Insights on ESOPs and Choosing a New ESOP Appraiser.

1 Contribution of S ESOPs to participants’ retirement security: Prepared for Employee-Owned S Corporations of America March 2015) Report can be accessed at: http://www.efesonline.org/LIBRARY/2015/EY_ESCA_S_ESOP_retirement_ security_analysis_2015.pdf.