January 2024 SAAR

The January 2024 SAAR was 15.0 million units, down 6.9% from last month and roughly flat (down 0.7%) compared to this time last year. Following 17 consecutive months of year-over-year improvements, the January 2024 SAAR ended the streak with a slight decline. Since January is generally a low-sales month, a decline in the SAAR itself does not necessarily dampen expectations for the remainder of 2024.

Unadjusted Sales Data

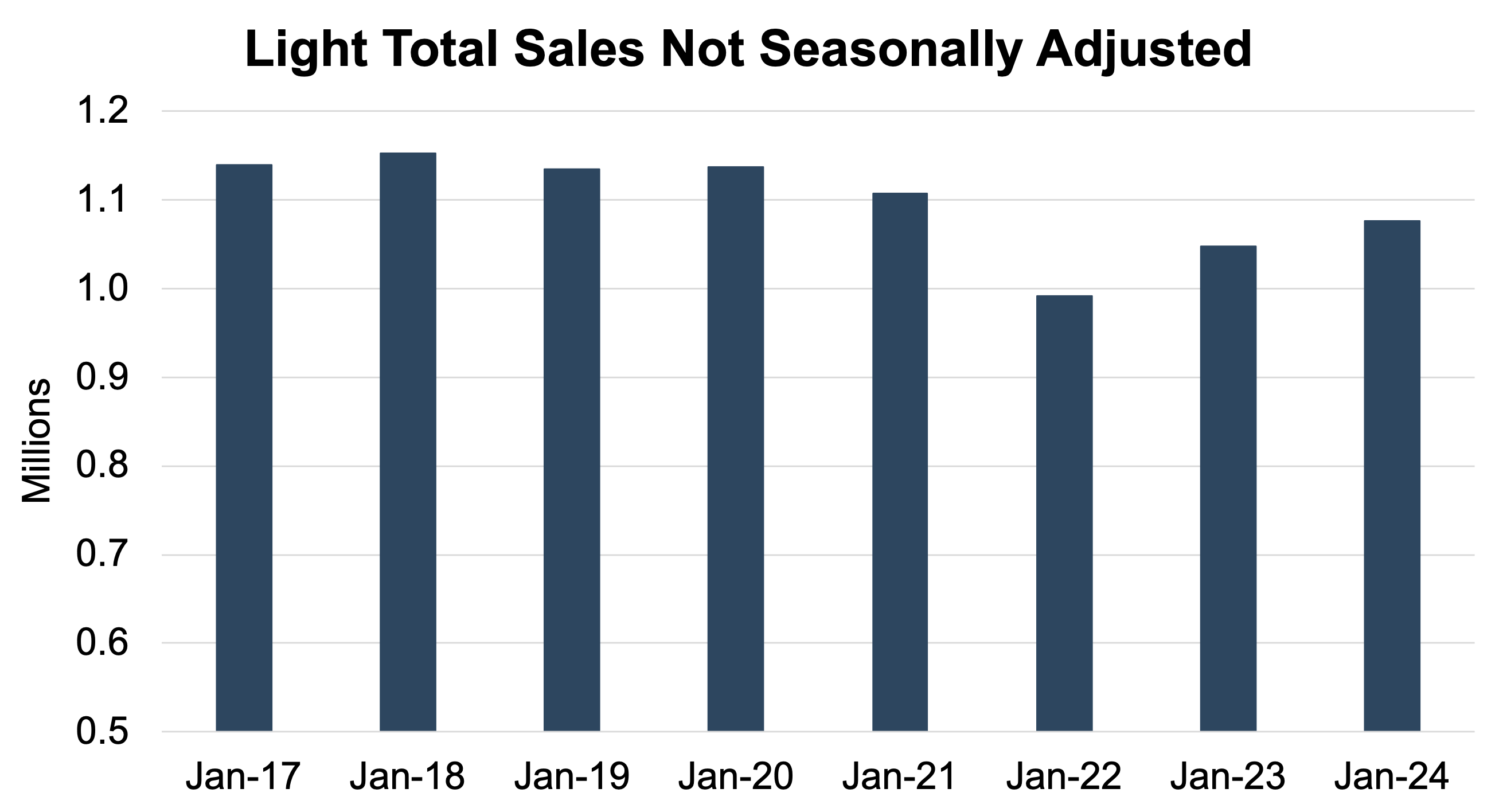

On an unadjusted basis, the industry sold 1.08 million total units in January 2024. From last month, unadjusted sales fell by over 25%. While shocking at first glance, we must note that this decline takes us from December (the highest-selling month) to January (the lowest-selling month); this fall-off is the exact reason the industry tracks volumes on a seasonally adjusted basis. Compared to the last several Januarys, however, this marks the highest January sales since 2021. The chart below shows unadjusted total sales volumes for the last eight Januarys:

Recall that COVID did not grip the industry until March 2020, and by 2021, the economic impact appeared to generally be beneficial to dealers. Additionally, it was not until later in 2021 that the full impact of the chip shortage was felt, so 2021 was not materially lower either.

Inventory and Days’ Supply

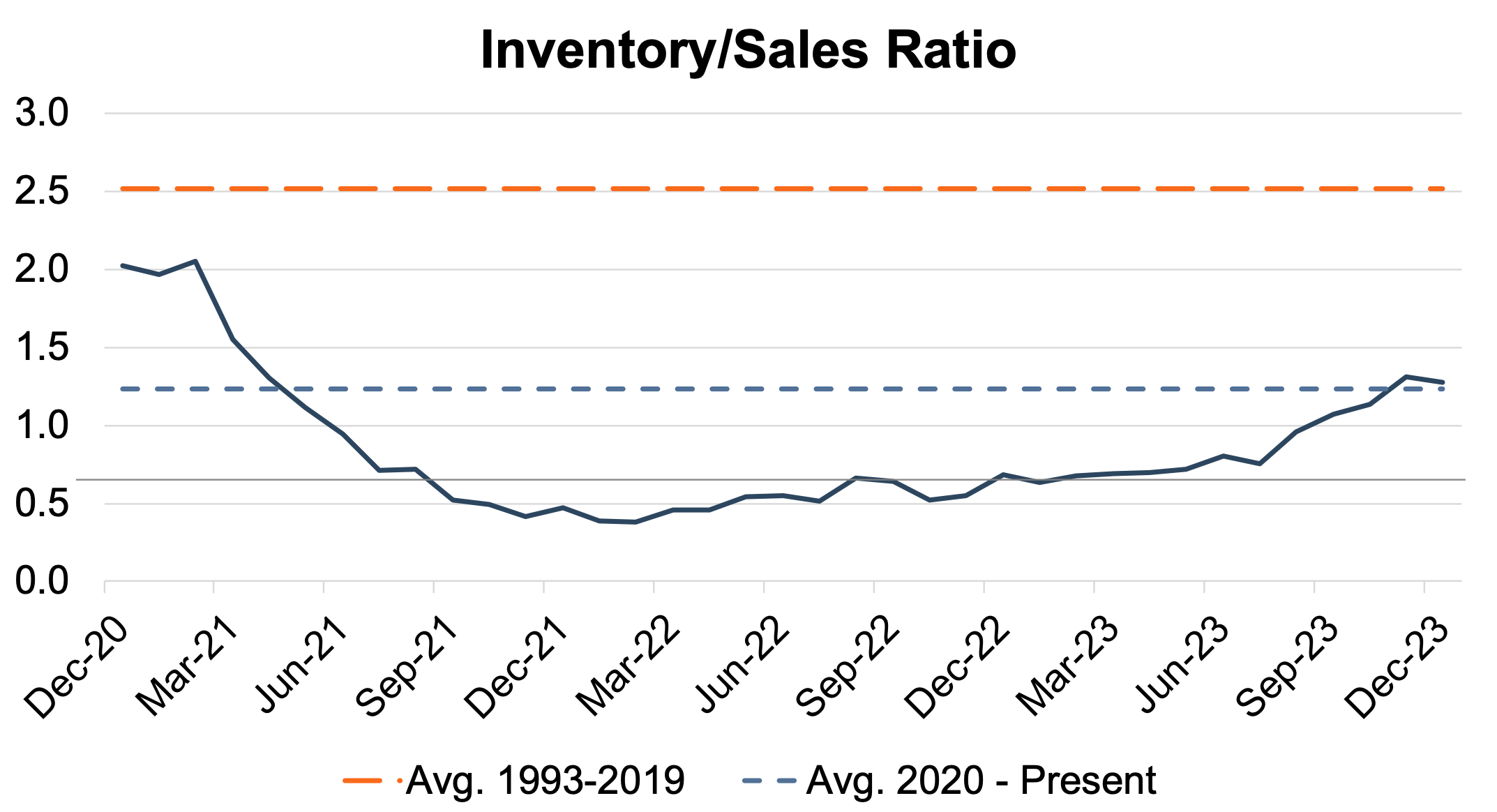

According to the NADA, while new light vehicle inventory saw a modest month-over-month increase of 4.0% from December 2023, a 40.4% year-over-year jump in January 2024 illustrates how far the industry has come over the past year. An inventory-to-sales ratio greater than 1.0x indicates that the seasonally adjusted inventory level at the end of the month was greater than reported sales. In December 2023, the inventory-to-sales ratio was 1.28x, marking the fourth consecutive month above 1.0x. The chart below illustrates the industry’s inventory-to-sales ratio over the last three years.

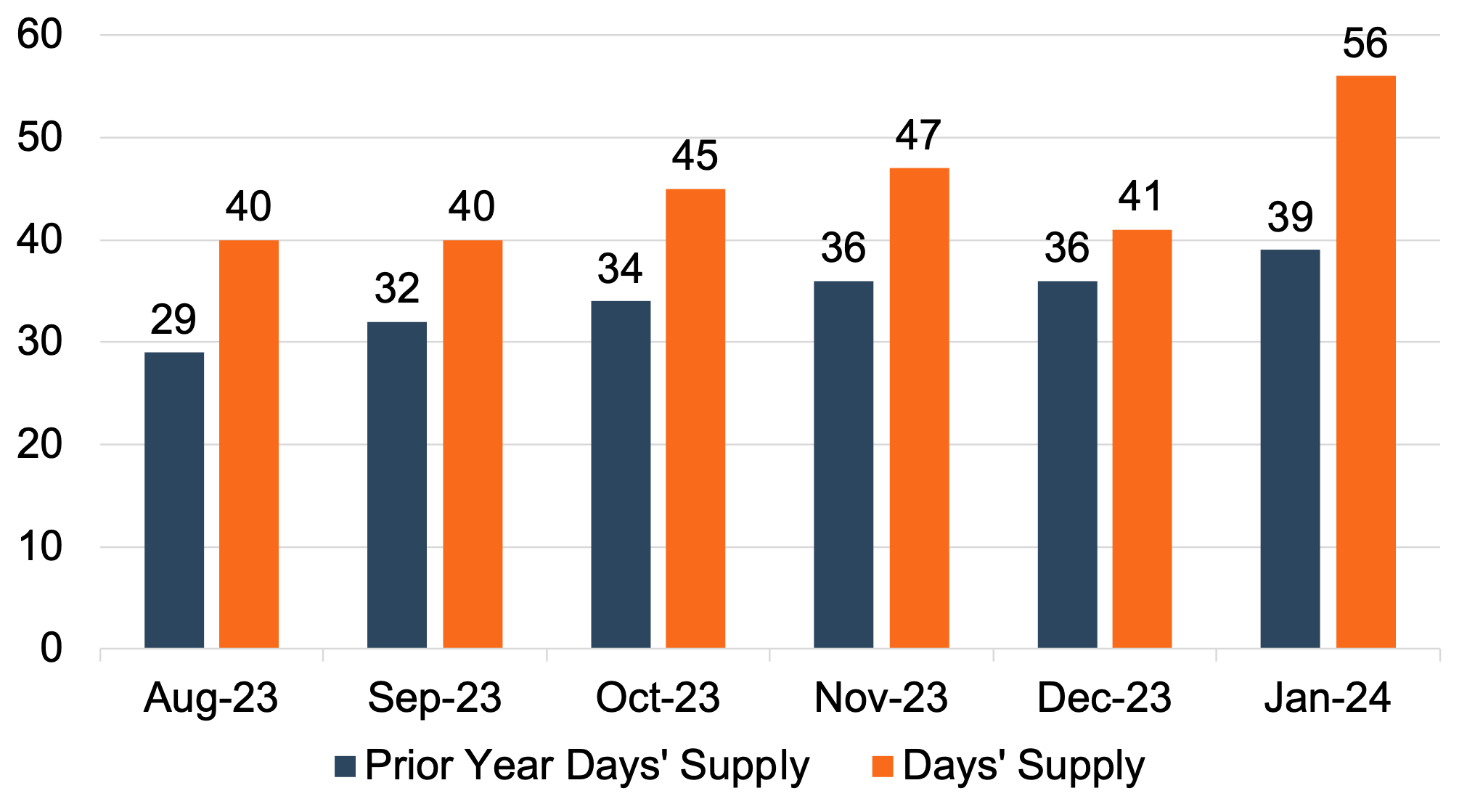

Days’ Supply, another window into the relationship between auto sales and inventory, has generally increased over the last year. In January 2024, Days’ Supply increased to 56 from 41 in December 2023. While there is a chance Days’ Supply will drop below 50 in the coming months, the January level of Days’ Supply, together with the recovering inventory-to-sales ratio, may indicate a return to pre-pandemic inventory levels. The chart below gives a closer look at Days’ Supply for U.S. Light Vehicles over the past six months (per Wards Intelligence):

We find the jump in Days’ Supply notable because since the chip shortage, public auto executives have been discussing the potential for a new normal in Days’ Supply and that OEMs may have learned that the ecosystem can be more profitable with fewer vehicles on the lot. While January may turn out to be an anomaly, it’s decidedly against the idea that inventories at low levels are the “new normal.”

We find the jump in Days’ Supply notable because since the chip shortage, public auto executives have been discussing the potential for a new normal in Days’ Supply and that OEMs may have learned that the ecosystem can be more profitable with fewer vehicles on the lot. While January may turn out to be an anomaly, it’s decidedly against the idea that inventories at low levels are the “new normal.”

Thomas King, president of data and analytics at J.D. Power, made the following comments on January’s inventory and dealer profit levels:

“While retailers continue to pre-sell vehicles, rising inventory is enabling more shoppers to buy directly off of dealer lots. In January, 32.7% of vehicles are projected to sell within 10 days of their arrival at the dealership, which is down from the peak of 58% in March 2022. The average time that a new vehicle spends in the dealer’s possession before being sold is expected to be 40 days, up 13 days from a year ago.”

Transaction Prices

Mr. King also discussed the downward trend in average transaction prices for new vehicles in January:

“Average new-vehicle retail transaction price is declining mostly due to shifts to smaller and more affordable segments that have increased in availability. Transaction prices in January are trending towards $45,106, down $1,636—or 3.5%—from January 2023. However, even with the decline in average transaction prices, consumers are on track to spend nearly $37 billion on new vehicles this month—the third highest on record for the month of January just 2% lower than January 2023.”

On the used vehicle side, sales increased from December 2023 but experienced a year-over-year decline. According to J.D. Power, the January average used-vehicle price of $28,100 is down 2.4% from a year ago. Falling transaction prices are also impacting trade-in values, which are down approximately 11% from last year. As inventory levels continue to rise, we will likely see the average transaction price continue to moderate throughout 2024.

Generally, increasing inventory and declining transaction prices have also hindered per-unit dealer profit. Mr. King discusses factors affecting dealer profits below:

“The increase in new-vehicle supply is resulting in declining per unit dealer profits, but those profits continue to exceed pre-pandemic levels. The total retailer profit per unit—which includes vehicles gross plus finance and insurance income—is expected to be $2,817 in January, down 28.5% from January 2023. The primary factor behind the profit decline is the reduced number of vehicles selling above the manufacturer’s suggested retail price (MSRP). Thus far in January, only 18.5% of new vehicles have been sold above MSRP, which is down from 33.1% in January 2023.”

Incentive Spending

According to J.D. Power, average incentive spending per unit in January is expected to hit $2,346, up approximately 74% from one year ago. Incentive spending as a percentage of the average MSRP is expected to reach 4.8%, reflecting an increase of 2.0 percentage points from January 2023. While incentive spending remains elevated in January, it is important to note that these are average figures, and some markets and vehicle make/models are still transacting closer to (or above) MSRP.

February 2024 Outlook

Mercer Capital expects the February 2024 SAAR to come in around 15 million. As the industry continues to see expanding inventory levels, the average transaction price has continued to fall. While lower per-unit profitability is something to watch, we believe it is reasonable to expect OEMs to prioritize their own profitability, meaning higher volumes and more incentives.

Mercer Capital provides business valuation and financial advisory services, and our auto team helps dealers, their partners, and family members understand the value of their business. Contact a member of the Mercer Capital auto dealer team today to learn more about the value of your dealership.