Valuation Assumptions Influence Auto Dealer Valuation Conclusions

How to Understand the Reasonableness of Individual Assumptions and Conclusions

There are several life events (large and small) that require an owner of an auto dealership to seek a business valuation – estate planning, a potential sale, shareholder dispute/litigation, divorce, death of an owner, etc. Often the owner of the dealership and their advisors may only view a handful of business valuations during their careers. It is not unusual for the valuation conclusions of appraisers to differ significantly, with one significantly lower or higher than the other.

Valuation also involves proving the overall reasonableness of an appraiser’s conclusion.

What is an owner or their advisor to think when significantly different valuation conclusions are present? The answer to the reasonableness of the conclusion lies in the reasonableness of the appraiser’s assumptions. However, valuation is more than “proving” that each and every assumption is reasonable. Valuation also involves proving the overall reasonableness of an appraiser’s conclusion.

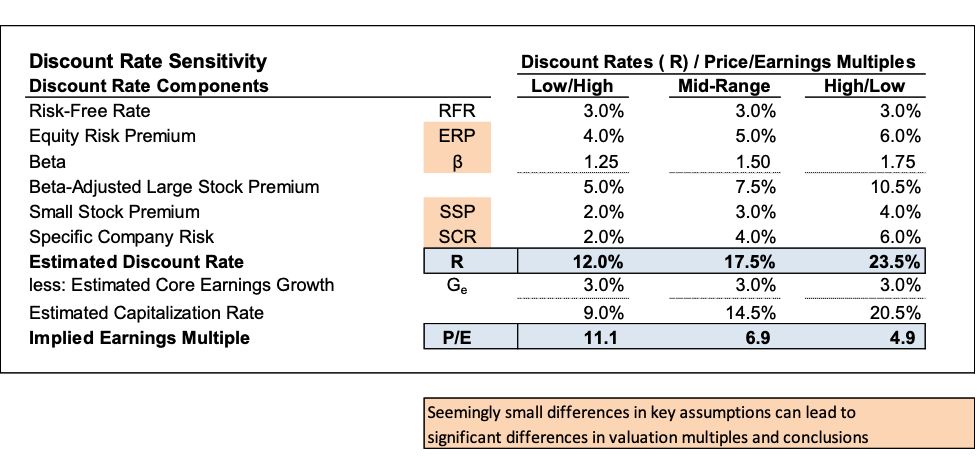

A short example will illustrate this point and then we can address the issue of individual assumptions. In the following example, we see three potential discount rates and resulting price/earnings (“P/E”) multiples. The discount rate or rate of return is a key component in determining the value of an auto dealership under an income approach. While other methods, including Blue Sky multiples are more often used, determining the rate of return applicable to an auto dealership is also an important step in a business valuation.

In the table below, we look at the theoretical assumptions used by appraisers to “build” discount rates. We show differing assumptions regarding four of the components, and none of the differing assumptions seems to be too far from the others. So, we vary what is called the equity risk premium (“ERP”), the beta statistic, which is a measure of riskiness, the small stock premium (“SSP”), and specific company risk (“SCR”).

The left column (showing the low discount rate of 12.0% and a high P/E multiple of 11.1x) would yield the highest valuation conclusion. The right column (showing the high discount rate of 23.5% and the low P/E of 4.9x) would yield a substantially lower conclusion. That range is substantial and results in widely differing conclusions.

In either case, appraisers might have made a seemingly convincing argument that each of their assumptions were reasonable and, therefore, that their conclusions were reasonable. However, the proof is in the pudding. Perhaps, neither the low nor the high examples would yield reasonable conclusions when viewed in light of available market evidence of the particular franchise, and location and profitability of the subject dealership.

So, as we discuss how to understand the reasonableness of individual valuation assumptions in business appraisals of auto dealerships, know also that the valuation conclusions must themselves be proven to be reasonable. That’s why we place a “test of reasonableness” in every Mercer Capital valuation report that reaches a valuation conclusion.

Auto Dealership Valuation Assumptions

Now, we turn to individual assumptions utilized in an auto dealership valuation.

Growth Rates

Growth rates can impact a valuation in several ways. First, growth rates can explain historical or future changes in revenues, earnings, profitability, etc. A long-term growth rate is also a key assumption in determining a discount rate and resulting capitalization rate under the income approach.

A long-term growth rate is also a key assumption in determining a discount rate and resulting capitalization rate under the income approach.

Growth rates, as a measure of historical or future change in performance, should be explained by the events that have occurred or are expected to occur. In other words, an appraiser should be able to explain the specific events that led to a certain growth rate, in terms of total and departmental revenue and profitability. Auto dealerships experiencing large growth rates from one year to the next should be able to explain the trends that led to the large changes, whether it is new customers, new vehicle models being offered, loss/additional of a competitor, or other pertinent factors. Large growth rates for an extended period of time should always be questioned by the appraiser as to their sustainability at those heightened levels. This is particularly true for auto dealers, which as dealer principals know, experience ebbs and flows of the business cycle.

A long-term growth rate is an assumption utilized by all appraisers in a capitalization rate. The long-term growth rate should estimate the annual, sustainable growth that the dealership expects to achieve. Typically, this assumption is based on a long-term inflation factor plus/minus a few percentage points. Be mindful of any very small, negative, or large long-term growth rate assumptions. If confronted with one, what are the specific reasons for those extreme assumptions?

Annualization

In the course of a business valuation, appraisers normally examine the financial performance of the auto dealership for a historical period of around five years, if available. Since business valuations are point-in-time estimates, the date of the valuation may not always coincide with the auto dealership’s annual reporting period.

Dealerships should be able to provide factory financial statements for the year-to-date period coinciding with the valuation date for the current and preceding year. A business appraiser can compile a trailing twelve month (“TTM”) financial statement from those two interim factory statements and the most recent 13th month year-end factory statement. A TTM financial statement allows an appraiser to examine a full-year business cycle and is not as influenced by seasonality or cyclicality of operations and performance during partial fiscal years. The balance sheet may still reflect some seasonality or cyclicality.

Be cautious of appraisers that annualize a short portion of a fiscal year to estimate an annual result. This practice could result in inflating or deflating expected results if there is significant seasonality or cyclicality present. At the very least, the annualized results should be compared with historical and expected future results in terms of implied margins and growth.

Dealer principals are well aware of monthly volumes of light vehicles sold in the U.S. that are annualized and referred to as “SAAR.” Due to the number of selling days and the inherent seasonality throughout the calendar year, properly determining the TTM financials should reduce the need to consider a complex formula such as that employed in the calculation of SAAR that almost certainly is not used if an appraiser simply annualizes by scaling up a stub period to 12 months.

Litigation Recession

“Litigation recession” is a term to describe a phenomenon that sometimes occurs when an owner portrays doom and gloom in their industry and for the current and future financial performance of the dealership. As with other assumptions, an appraiser should not blindly accept this outlook.

A quality appraiser will compare the performance of the dealership against its historical trends, future outlook, and the condition of the industry and economy, among other factors. Be cautious of an appraisal where the current year or ongoing expectations are substantially lower, or higher for that matter, than historical performance without a tangible explanation as to why.

Industry Conditions

Most formal business valuations should include a narrative describing the current and expected future conditions of the auto dealer industry. An important discussion is how those factors specifically affect the dealership being valued. There could be reasons why the dealership’s market is experiencing things differently than the national industry. Industry conditions can provide qualitative reasons why and how the quantitative numbers for the dealership are changing. Look carefully at business valuations that do not discuss industry conditions or those where the industry conditions are contrary to the dealership’s trends. Current valuations in 2020 should include a discussion of the local industry conditions and their impact on a dealership’s performance as the effects of the pandemic have varied across states and regions.

Valuation Techniques Specific to the Auto Dealer Industry

As we have previously written, the valuation methods utilized in the auto dealer industry are unique and include an asset-based approach, an income approach, and a modified market approach incorporating concepts of Blue Sky value. It may be difficult for a layperson reviewing a business valuation to know whether the methods employed are general or industry-specific techniques. An auto dealer or their advisor should ask the appraiser how much experience they have performing valuations in the auto dealer industry.

Risk Factors

Risk factors are all of the qualitative and quantitative factors that affect the expected future performance of the auto dealership. Simply put, a business valuation combines the expected financial performance of the dealership (earnings and growth) and its risk factors. Risk factors show up as part of the discount rate utilized in the income approach of the business valuation.

Like growth rates, there is no textbook that lists the appropriate risk factors for the auto dealer industry. However, there is a reasonable range for this assumption.

Be careful of appraisers that have an extreme figure for risk factors. Make sure there is a clear explanation for the lowered or heightened risk. Otherwise, this is an easy area to influence a lower or higher valuation of the dealership.

Blue Sky Multiples

Another typical component of an auto dealer valuation is the use of Blue Sky multiples and the reflection of the concluded value as a measure of Blue Sky. As we have discussed, there are several national business brokers that publish these multiples quarterly by the manufacturer. Be wary of appraisers that do not reference Blue Sky multiples or explain their concluded values as a measure of Blue Sky. Also, be wary of appraisers that apply Blue Sky multiples to used vehicles or other metrics that are not widely recognized by the auto dealer industry.

Another critique could be the range of Blue Sky multiples examined and how they are applied to the subject dealership. Take note of an appraiser that applies the extreme bottom or top end of the range of multiples, or perhaps even a multiple not in the range. Be prepared to discuss the multiple selected or implied and how the dealership compares to the range of multiples in terms of the local market (location and urban vs. rural), level of competition, historical profitability, etc.

… we believe Blue Sky multiples are very helpful, at least for explaining value.

In our review of appraisals performed by other firms, particularly those without considerable auto dealer experience, we see Blue Sky multiples either won’t be rigorously analyzed or may not even be mentioned. While this may not be a red flag to a layperson, we believe Blue Sky multiples are very helpful, at least for explaining value. To confirm the reasonableness of an appraisal that does not mention Blue Sky multiples, dealer principals can calculate it themselves. Blue Sky value is measured/calculated as the excess equity value over the tangible net assets of the dealership. If the implied multiple from an appraisal is unreasonable in the context of multiples seen for the relevant franchise(s), the overall reasonableness of the conclusion should be questioned.

Time Periods Considered

Earlier we stated that a typical appraiser examines the prior five years of the dealership’s financial performance, if available. Be cautious of appraisers that simply choose to use a small sample size, i.e. the latest year’s results, as an estimate of the dealership’s ongoing earnings potential. The number of years examined should be discussed and an explanation as to why certain years were considered or not considered should be offered.

Some industries, like the auto dealer industry, have multi-year cycles, not just annually (further evidence of the importance of a discussion of industry conditions and consideration of recognized industry-specific techniques in the appraisal).

The examination of one year or a few years (instead of five years) can result in a much higher or lower valuation conclusion. If this is the case, it should be explained.

Conclusion

Business valuations of auto dealerships are a technical analysis of methodologies used to arrive at a conclusion of value for the subject dealership. It can be difficult for an auto dealer or their advisors to understand the impact of certain individual assumptions and whether or not those assumptions are reasonable. In addition to a review of individual assumptions, the valuation conclusion should be reasonable.

Mercer Capital performs numerous business valuations of auto dealers annually for a variety of purposes. Contact a professional at Mercer Capital to discuss your next business valuation.