Three years ago, I wrote an article about the state of valuations for Appalachian gas companies. I used imagery from Sergio Leone’s classic: The Good, The Bad, and The Ugly as a theme. At the time, bad and ugly dominated over the good. Henry Hub prices were hovering around $2 per mcf. Valuations were depressed, and Appalachian gas producers were struggling. Clint Eastwood would have lost that climactic gunfight if that world had remained.

It has not remained.

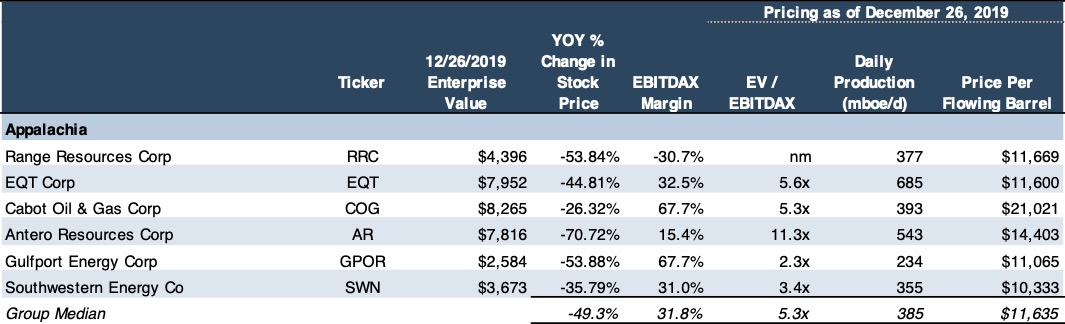

Today’s solid earnings and strong balance sheets are a far cry from what they were then. Stock prices have risen alongside a fresh confidence that $4 and $5 gas prices will be sustainable for a while. Mercer Capital’s sector statistics tell the story. This is an archived snapshot of these producers in 2019:

Source: Capital IQ

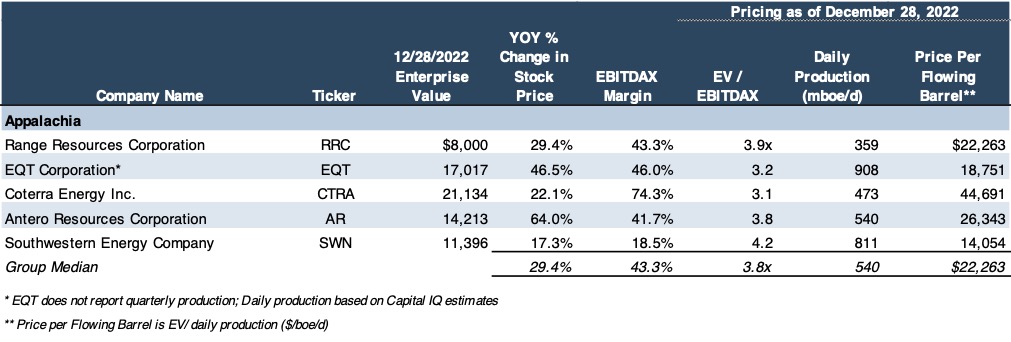

This is now at the end of 2022:

Source: Capital IQ

A lot has changed in the past three years that has strengthened and stabilized stock prices, margins, earnings multiples, and production multiples alike. The Appalachian public comp group saw markedly strong stock price performance over the past year (through December 28th), led by Antero and EQT.

The remaining members of the comp group showed more modest 1-year price increases. Stock prices dipped in mid-September but reversed direction immediately following the sabotage of the Nord Stream pipelines in the Baltic Sea that transport Russian natural gas to northern Europe. Antero and EQT led the way among this group for several reasons. For Antero, one reason appears to have been its lack of hedging for 2023, which has allowed it greater exposure to the uptick in gas prices and also to be aggressive in paying down debt. EQT, on the other hand, does have more near-term hedging ceilings to deal with. However, its strength is in its operational efficiencies, whereby their recent literature demonstrates breakeven operating expenses at $1.37 per mcf. This is among the lowest in the industry and allows them to accumulate cash flow.

In 2020 it looked like the bad and ugly would hang around indefinitely. Within around 70 days of my Appalachian gas article being published, the world was whipsawed between the COVID-19 outbreak and the OPEC+ impasse between Saudi Arabia and Russia. Energy markets went into a tailspin. It looked like the bad and the ugly would continue to reign, and they did, especially for Marcellus gas producers. Incredibly, Henry Hub prices dropped below $2 for much of the first and second quarters of 2020. Entire economies froze in their tracks as they tried to absorb this new reality. Infrastructure along with it, the Atlantic Coast Pipeline was canceled on July 5th. Then the Biden administration came to power, and rhetoric opposing fossil fuels escalated. Producers like Antero, EQT, and Range were running in neutral, fighting to increase production and financial efficiency amid the continuing low-price environment.

2020 was spent stuck in the proverbial mud. However, beneath the surface, some structural and fundamental shifts were starting to take place. First, production growth slowed. This was not only in response to temporary demand drops from the economic shocks of COVID. It was also a response to tight debt markets pulling back on the sector’s exposure. Capex was harder to get funded. The market’s message was clear: make the most of what you have now. The era of shale growth was ending, and the era of production efficiency and moderation was taking shape. This dynamic coincided with the past 40 years of steady growth (known by some as the period of Great Moderation) that was ending. The new world would be shaped by production constraints.

Second, industry began to onshore again in the U.S. Over decades past, industrial investment flowed out of the U.S. mostly due to lower labor costs elsewhere. Low-cost gas has upturned that equation. Over $200 billion is being spent on new and expanded U.S. chemical-related factories that use gas as a raw material for making chemicals, more than offsetting higher labor costs. Tens of billions more started going into steelmaking and other manufacturing plants seeking lower-cost electricity. Companies ranging from BAE Systems to Samsung to John Deere began shifting back onshore to the U.S. Every major car maker shifted plans to spend billions in the U.S. to build E.V. factories.

Thirdly, around the same time, another shift was happening. Executive compensation moved more in line with investors. Management incentives moved further away from production incentives and more towards financial performance and capital efficiency metrics. While prices were still hovering around $2 per mcf, equity investors demanded changes and wanted cash flow statements to “shift priorities,” so to speak. LNG export capability was coming online, and equity investors wanted to be ready for it. Otherwise, 2021 slugged along with these dynamics churning in the background, oftentimes very quietly. Gas prices started to drift upward, and business, airline, and driving activities all picked up.

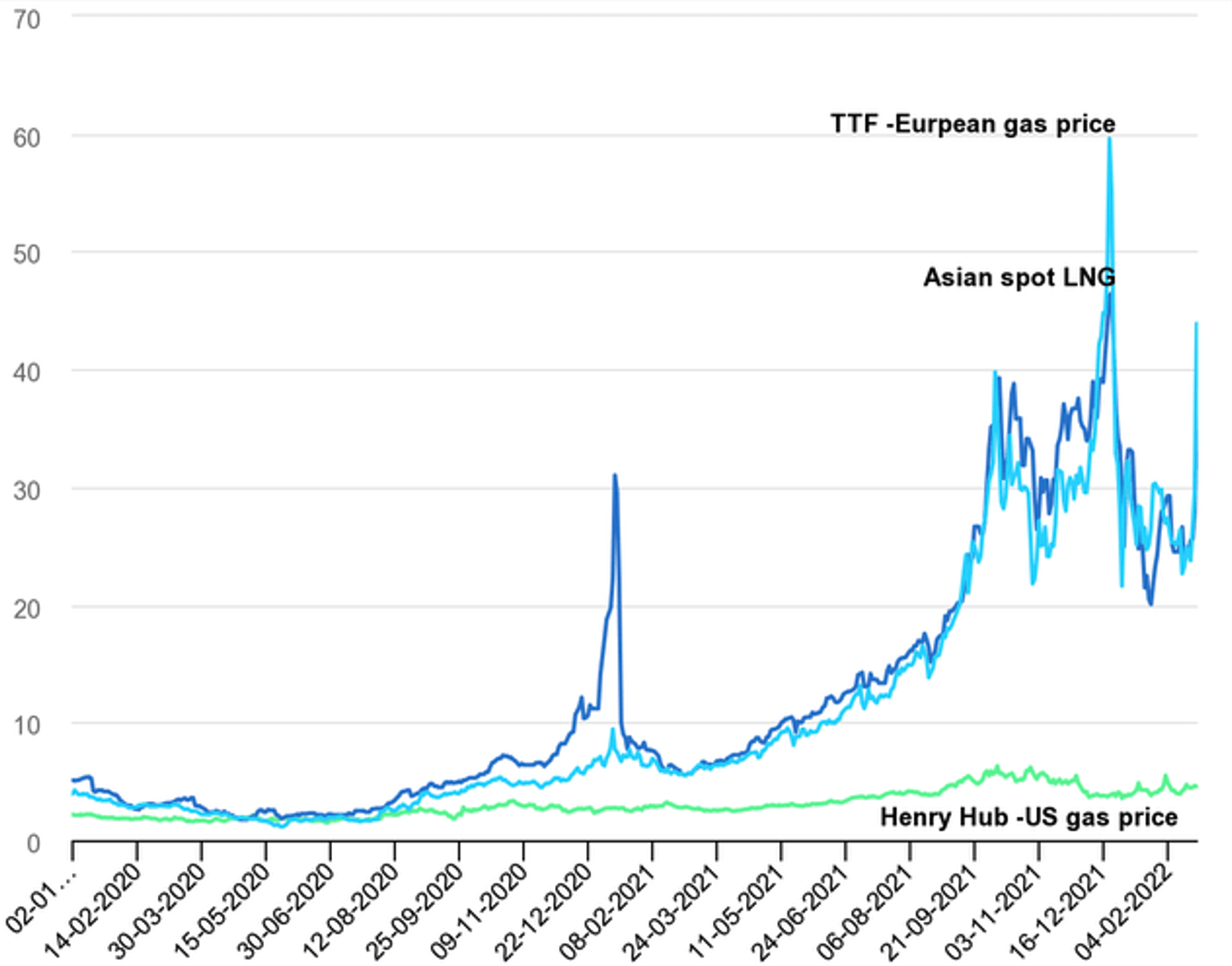

One very interesting market dynamic, however, was the rising overseas gas prices compared to Henry Hub, which widened as the year went along. By the end of 2021, the table had been set for 2022’s resurgence.

Source: International Energy Agency

The Present

Although the Russian invasion of Ukraine has been the headliner, other trends and frameworks were being set up in the second half of 2021. Europe realized it had made a grave mistake that would need to be partially fixed with Appalachian natural gas.

Now, in Europe, prices remain incredibly high, particularly for early next year. When the cold weather finally hits, concerns remain that Europe could quickly burn through its gas reserves, potentially leading to extreme tightness in supplies after Christmas. Gas at around €115 per megawatt hour is equivalent to almost $180 per barrel in oil terms. Contracts for January have been above $230 per barrel equivalent.

In addition, Europe has exhausted almost every available gas source, from increased LNG imports to asking Norway to maximize production for months. At this point, there is little in the way of supply additions expected globally until the middle of this decade. The E.U. will boost its ability to import LNG through floating terminals in Germany and the Netherlands, but they’ll be competing for the same limited supply pool. And without Russian gas, the E.U. will need even more LNG over the next 12 months.

Germany finished constructing its first import terminal for LNG, a crucial milestone in its efforts to end its energy dependency on Russia. However, Europe could still face a 30bn cubic-meter shortfall during next summer’s critical storage refilling period if Russia halts all pipeline deliveries and Chinese demand for liquefied natural gas increases as it lifts coronavirus restrictions, according to the International Energy Agency.

The U.S. will supply some of that LNG when more export facilities are built. One important event in March 2023 will be the reopening of the Freeport LNG terminal, which has been closed for several months due to an accident there. In standard times that terminal handles around 15% of U.S. LNG exports.

That leaves hidden demand to fill that had not been apparent until this year. Last Friday, Russian Deputy Prime Minister Alexander Novak told state television that Russia may cut oil production by 5%-7% in early 2023 in response to the price cap imposed by Western countries on its crude oil and refined products. This is bound to have a ripple effect. U.S. natural gas prices have been above $4 per mcf all year and above $5 per mcf since March, with a few brief spikes above $9. Appalachian Basin pricing is also tightening closer to NYMEX futures.

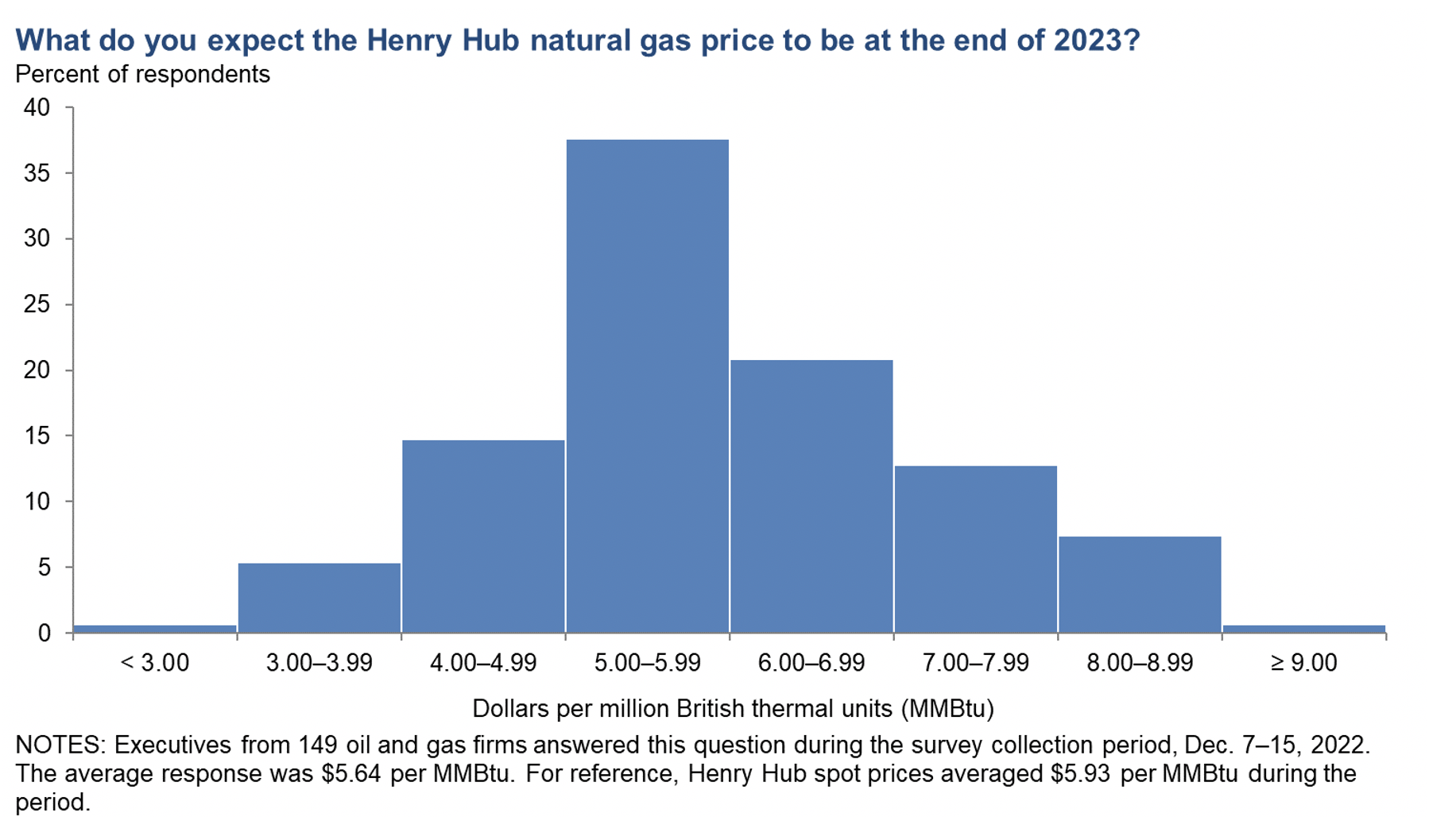

There have been modest increases in rigs and drilling from both E&Ps and contractors, but this is mainly in the high single or low double-digit variety. This is being done amid confidence that price increases this past year won’t be temporary:

Source: Federal Reserve Bank of Dallas: Energy Information Administration

Appalachian production held steady in 2022 despite historically high commodity price volatility driven by the Russian-Ukraine war, the sabotage of the Nord Stream pipelines, and rising LNG exports to Europe to stave-off potential winter heating shortages. On an interesting note, valuations for the publics are remarkably tight. Price-to-earnings ratios are between 5.0 – 5.5x, with the exception of EQT. Other metrics have risen and are healthier than they were, but P/E ratios are the tightest. Earnings are king right now.

The Future

Europe is going to de-industrialize, and thus energy demand will diminish as they move heavier towards a service economy. The E.U. made a mistake relying on Russia and not diversifying. Now they are paying the price for it. The world got complacent about cheap oil and gas due partly to the shale revolution.

Now supply markets are on edge. Saudi Aramco CEO Amin Nasser warned recently that LNG gas supply is a “hiccup” away from exposing how fraught the markets really are and that “there is no spare capacity available on the market.” These are all long-term contracts. So, it’s a much bigger issue for gas and LNG than crude. Solar, wind, and other renewables are not ready, yet, to shoulder a bigger portion of the energy requirement.” Charif Souki, Executive Chairman of the Board at Tellurian, thinks $4-5 mcf gas should be here to stay, with plenty of the commodity at this price. The main problem will be the infrastructure to transport it.

There are risks. No business is without these, and putting aside the risk of Putin causing a world war, the primary one is a glut of gas hitting the world market. Qatar is a huge supplier and is investing heavily to produce more. They signed a big contract to supply Germany with LNG. Since that gas only starts to flow in 2026, it is no threat in the near term and is only a small part of German and global needs. Domestically, all the drilling for oil at high prices this past year (adding over 100 rigs) has produced a lot of associated gas. East Daley Capital Analytics forecasts 4.6 Bcf/d from now to the end of 2023. However, East Daley is bullish on LNG in the long haul for Europe and the rest of the world.

The current Appalachian rig count is at a level beyond that needed for production volume maintenance, so there would seem to be at least some potential for Henry Hub price reductions going into 2023. However, the demand for new natural gas supplies to Europe provides a countervailing wind to any potential downward movement in natural gas prices. In the end, the natural gas markets seem to be amid a series of events that promise continued supply and demand shifts with no certainty as to where the market will go in 2023.

In the meantime, the cautious efficiency is paying off for Appalachian gas producers, and with the wounds from 2019-2020 healing, the future looks very good indeed.

Originally appeared on Forbes.com.