The Permian Boom Causing a Natural Gas Bust

The oil industry is cruising. Producers are flocking to many oil rich plays, most notably the Permian Basin, Bakken, and Eagle Ford. Producers in these areas are all looking to exploit multi-zone payouts and gain significant efficiencies with new deep lateral and horizontal wells.

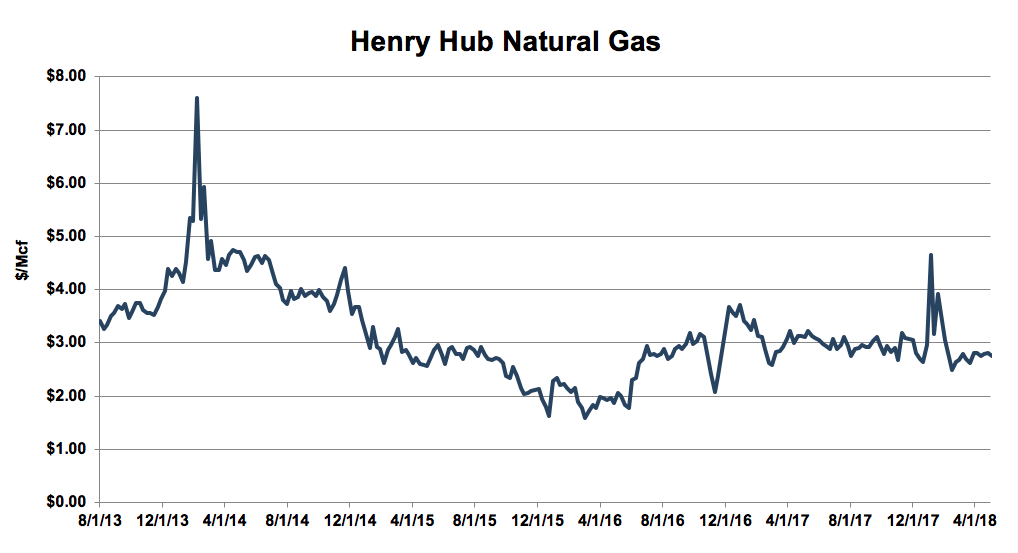

While this strategy is working very well for oil producers, often lost in the oil excitement is the byproduct, additional dry and natural gas liquids. For producers targeting natural gas, this is not good news. The U.S. has significant natural gas. While export demand is approximately 10% to 12% of all domestically produced natural gas, high supply and demand factors have kept prices relatively flat.

The Economics of the Current Price Environment

The articles below address the economics of the current price environment:

- Thank Goodness for Natural Gas Exports (Forbes)

- Demand for Natural Gas is Surging, but Glut Remains (US News and World Report)

- Why U.S. Natural Gas Prices Will Remain Low (Forbes)

While the low prices are favorable for consumers of natural gas, E&P companies are struggling. Producers of natural gas, specifically those operating in areas where crude oil is minimal, such as the Marcellus and Utica, are getting stretched thin, some beyond their ability to recover. Rex Energy Corporation (Rex) is the latest natural gas producer to file for a Chapter 11 orderly reorganization beginning with the sale of assets.

Rex Energy Corporation

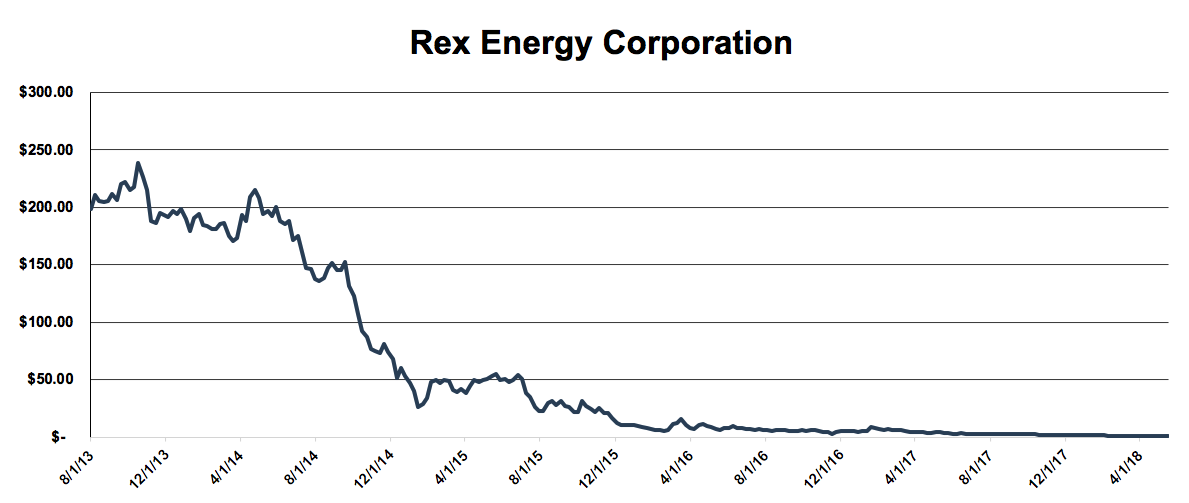

Rex Energy Corporation is an independent E&P company that produces condensate, natural gas liquid (NGL), and natural gas in the Marcellus, Utica, and Burkett Shale. On May 18th, Rex announced that, following its previously announced strategic review, it has decided to begin an orderly sale process for its remaining assets in order to maximize their long-term value and prospects. To facilitate the sale and address its debt obligations, the Company initiated voluntary proceedings under Chapter 11 of the U.S. Bankruptcy Code with support outlined in a Restructuring Support Agreement signed by 100% of its first lien lenders and approximately 72% of its second lien noteholders.

A review of their financial performance over the previous five years indicates declining revenues from lower natural gas prices. Revenue increased from 2013 to 2014, then declined during 2015-2017. This behavior is consistent with commodity price fluctuations. Operating income followed a similar trend which put pressure on the company to use debt to fill the gap. Debt doubled from 2013 through March 2018 and interest expense increased during all years and peaked at $62 million during the LTM March 2018 period. All of this was done hoping natural gas prices would increase to the point Rex could reach profitability. However, Rex ran out of time.

Other Marcellus and Utica Operators

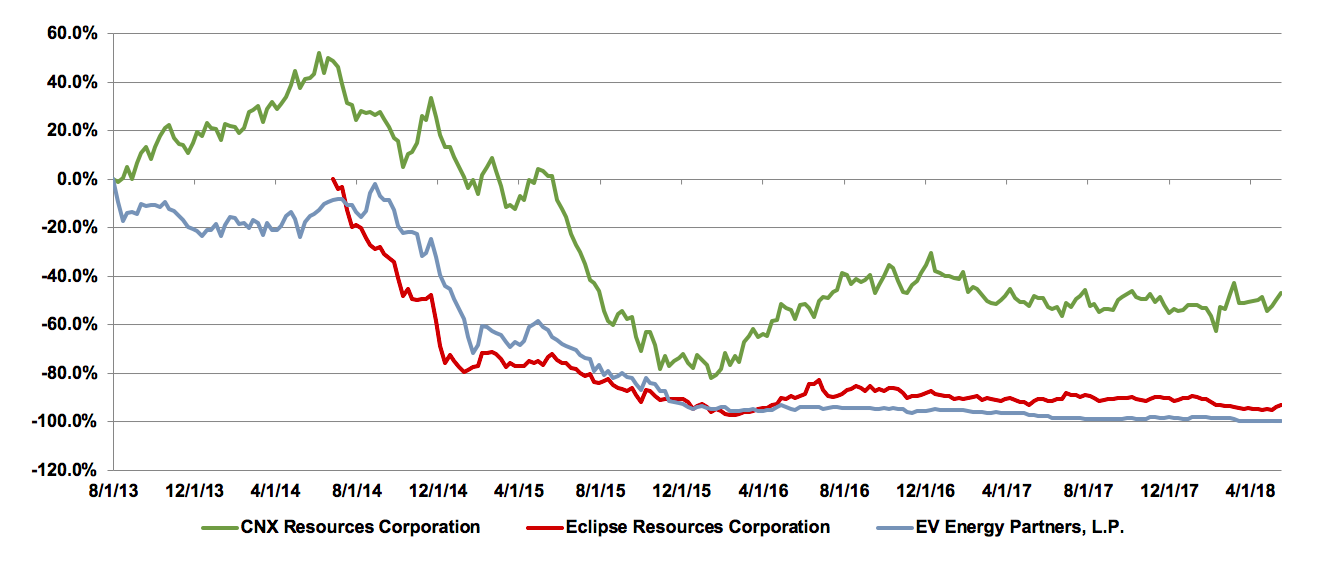

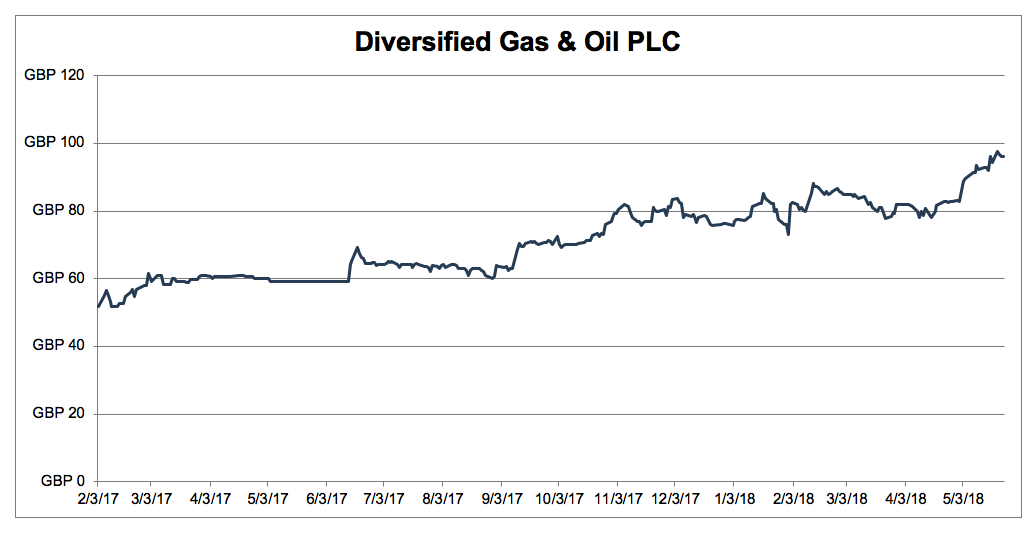

Rex is not the only Marcellus and Utica operator with this trend. CNX Resources, Eclipse Resources and EV Energy Partners all have stock charts with similar trends. Diversified Gas and Oil is the only publicly traded Marcellus and Utica focused producer with a stock price trend bucking the macro environment. They are also relatively new to the publicly traded scene, having been publicly traded for less than two year.

CNX Resources, Eclipse Resources and EV Energy Partners have seen price declines on the order of 50% to 100% since mid-2014. Eclipse Resources, for example, experienced a rapid fall in its stock price after raising $818 million in a U.S. initial public offering. Its stock price has fallen by nearly 100% and last month Eclipse announced that they were evaluating different options to maximize company value such as engaging in accretive acquisitions or sale of the company.

The performance of all the E&P companies named above is shown below.

Descriptions of each company are included below per their respective 10Ks.

- CNX Resources Corporation, an independent oil and natural gas company, explores for, develops, and produces natural gas in the Appalachian Basin. As of December 31, 2017, it had 7.6 trillion cubic feet equivalent of proved natural gas reserves. The company also owns, operates, and develops natural gas gathering and other midstream energy assets in the Marcellus Shale in Pennsylvania and West Virginia. The company was formerly known as CONSOL Energy Inc. and changed its name to CNX Resources Corporation in November 2017.

- Eclipse Resources Corporation, an independent exploration and production company, acquires and develops oil and natural gas properties in the Appalachian Basin. The company holds interests in the Utica Shale and Marcellus Shale areas.

- EV Energy Partners, L.P., through its subsidiaries, engages in the acquisition, development, and production of oil and natural gas properties in the United States. Its properties are located in the Barnett Shale; the San Juan Basin; the Appalachian Basin; Michigan; Central Texas; the Monroe Field in Northern Louisiana; the Mid–Continent areas in Oklahoma, Texas, Arkansas, Kansas, and Louisiana; and the Permian Basin.

- Diversified Gas & Oil PLC engages in the production of natural gas and crude oil in the Appalachian Basin of the United States. It has interests in the oil and gas properties in Pennsylvania, Ohio, and West Virginia. As shown below, it has not experienced the same declines in price as many of the other producers in the region.

Conclusion

While these macro issues have been impacting the industry for years, many investors have expected supply to fall to the point of creating higher prices. As this Wall Street Journal article points out, many investors had to adjust their investment time horizon. Investments made during 2014 and 2015 have not been exited by hedge funds like Fir Tree due to lower than expected public demand. Fir Tree’s energy investment strategy included purchasing the debt of failing companies only to flip it into a controlling equity position in the “emerged from bankruptcy” company. While they have been somewhat successful in this strategy, their holding periods are longer than originally planned. It appears investor’s are salivating for more companies like Amazon and less for companies like Sandridge Energy. While the headlines are focused on Permian Basin winners, the rest of the oil and gas market is not as cheery. The mixed bag of winners and losers makes the industry tricky to operate within.

We have assisted many clients with various valuation needs in the upstream oil and gas space in the Marcellus and Utica areas, other conventional and unconventional plays in North America and around the world. Contact Mercer Capital to discuss your needs in confidence and learn more about how we can help you succeed.