If valuation were an Olympic sport, fund managers and valuation specialists would expect to lose some points for the low “degree of difficulty” in their exercises over the past couple years. Buoyant equity markets, broad credit availability, historically low fixed income yields, and benign credit experience each contributed to ideal valuation conditions for private equity managers in 2013 and 2014. A reversal – or even slowing – of this trend would likely increase the scrutiny on fair value measurement for fund managers. In short, portfolio valuation marks are likely to get trickier in 2015.

Equity Valuation

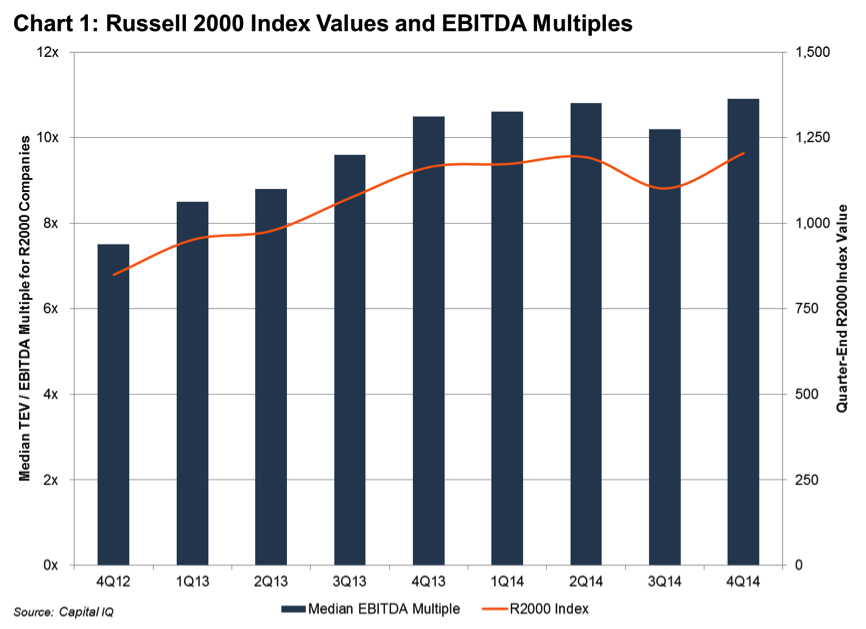

Favorable equity market returns over the past two years have been driven in large part by multiple expansion (a likely consequence of the Fed’s zero-interest rate policy).

The expansion in multiples has been broad-based, with only the energy and telecom sectors seeing multiples contract over the past two years.

The expanding multiples have resulted in little resistance to steadily increasing fair value marks; however, high multiple valuations tend to be more susceptible to earnings misses. Depending on how the market interprets the earnings shortfall, the decrease in value from a failure to hit expectations/budget may be exacerbated by a reduction in the valuation multiple, as the market reassess the risk and/or growth potential of the subject company. Recently published data from FactSet Research (requires subscription) suggests that public stock analysts are pulling back on 1Q15 earnings estimates in response to weakness in the energy sector and the strong dollar.

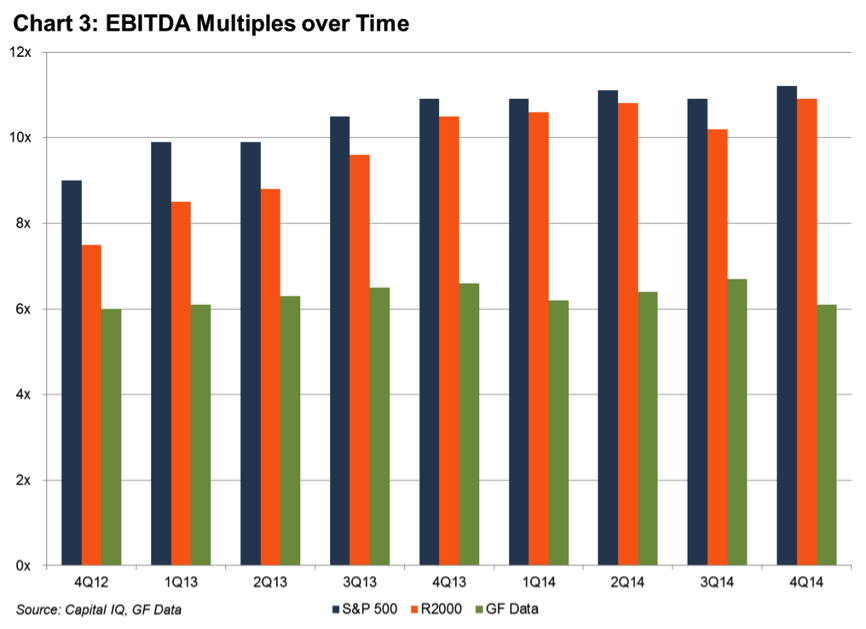

As noted below, smaller middle market deal multiples reported by GF Data tend to be less sensitive to changes in public comps. For such companies (having an enterprise value of less than $250 million), financing conditions (with respect to availability, leverage, and cost) can influence transaction multiples nearly as much as trends in public market multiples.

For lower middle market equity investments, the greatest valuation challenges in coming quarters are likely to materialize in the event of failure to hit revenue and EBITDA targets or if less liquid credit markets shrink the transaction multiples deal makers can engineer while maintaining target equity returns.

Credit Valuation

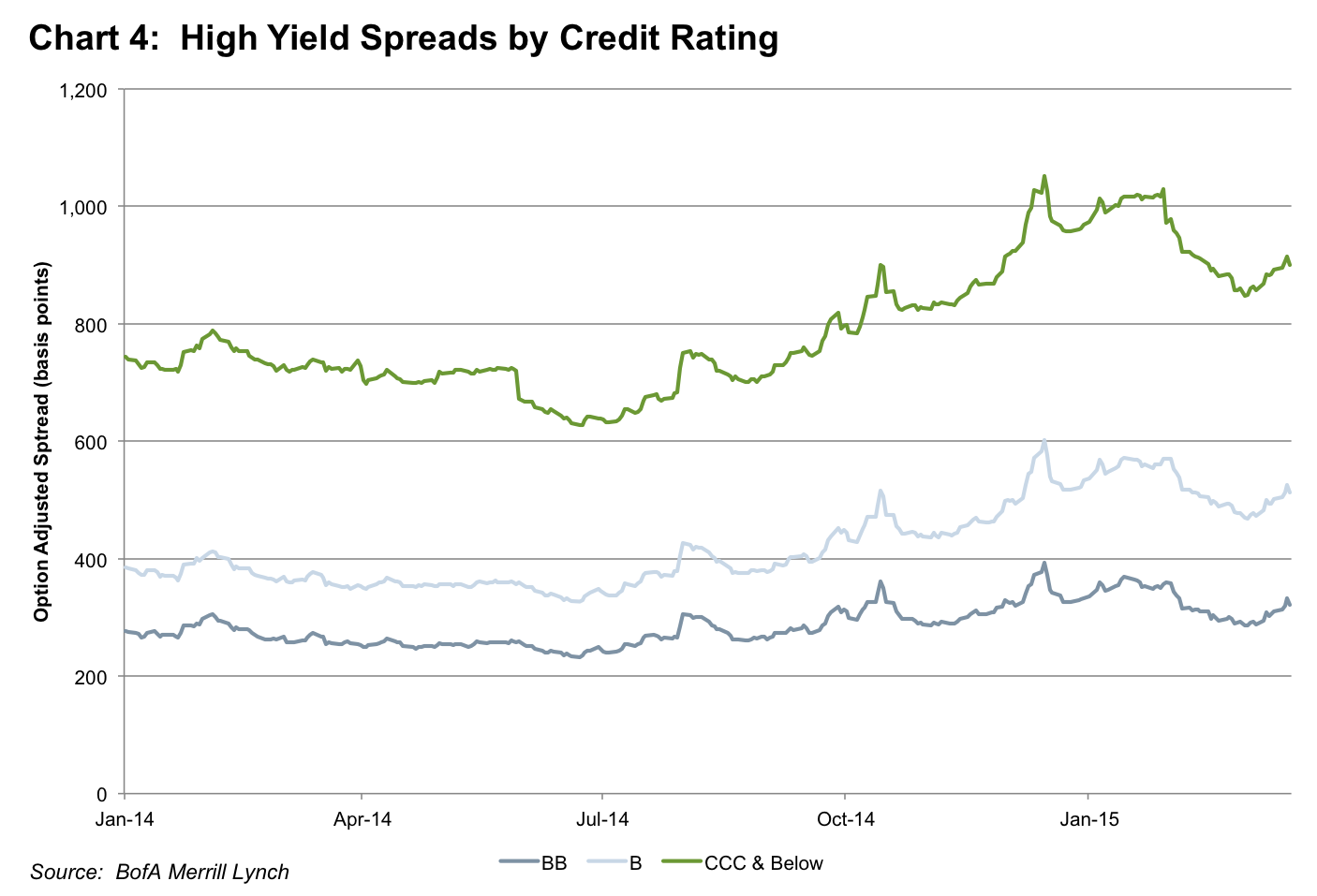

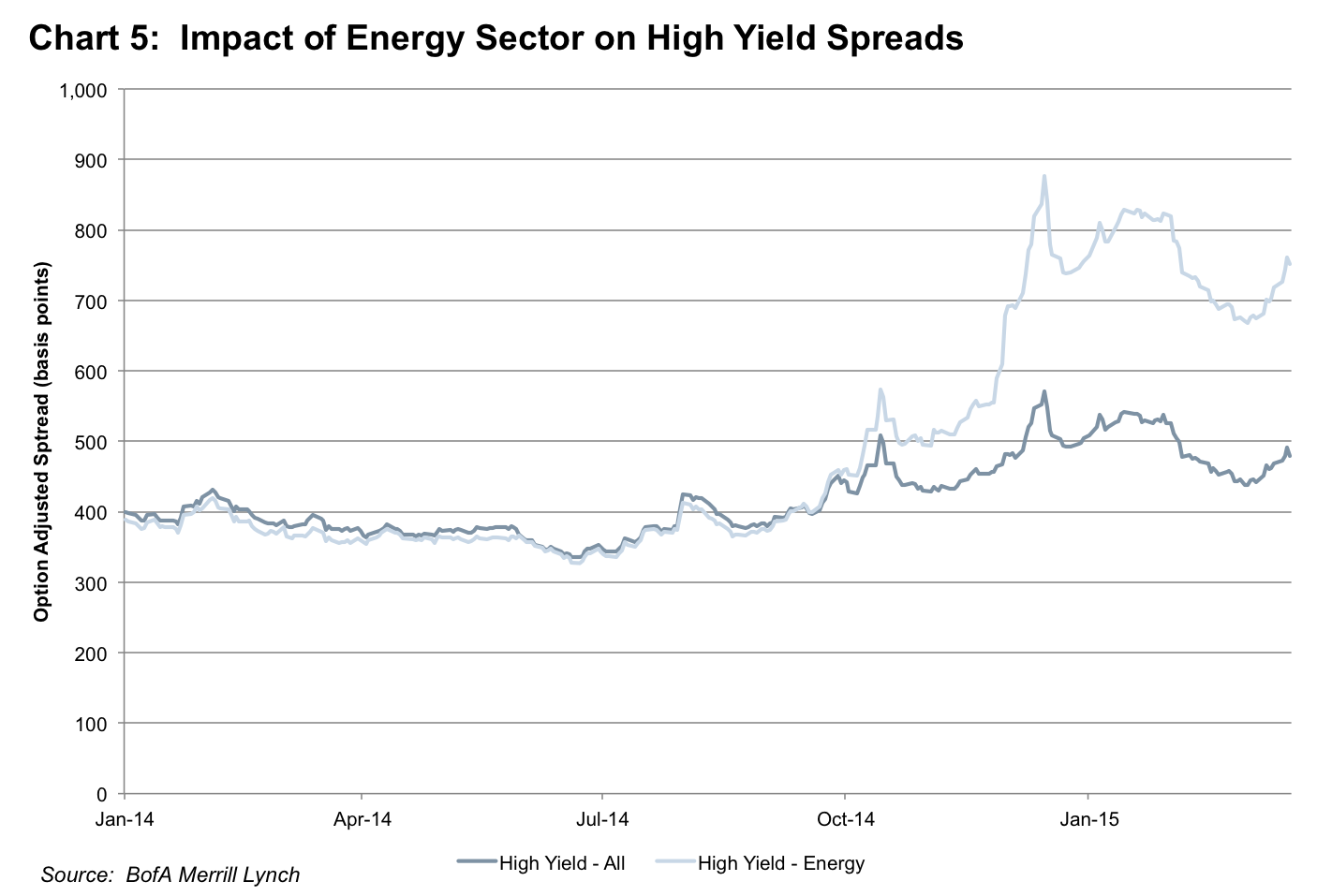

For credit investors, valuations became more complicated in the second half of 2014. The sustained compression in high yield credit spreads dating from mid-2012 came to an end in June 2014 as observed spreads bottomed out across the credit spectrum. Over the second half of the year, spreads widened back to mid-2013 levels.

While a market-wide phenomenon, the spread widening observed in the major indices was exaggerated by the challenging energy sector. Outside the energy sector, the negative impact of wider spreads was muted.

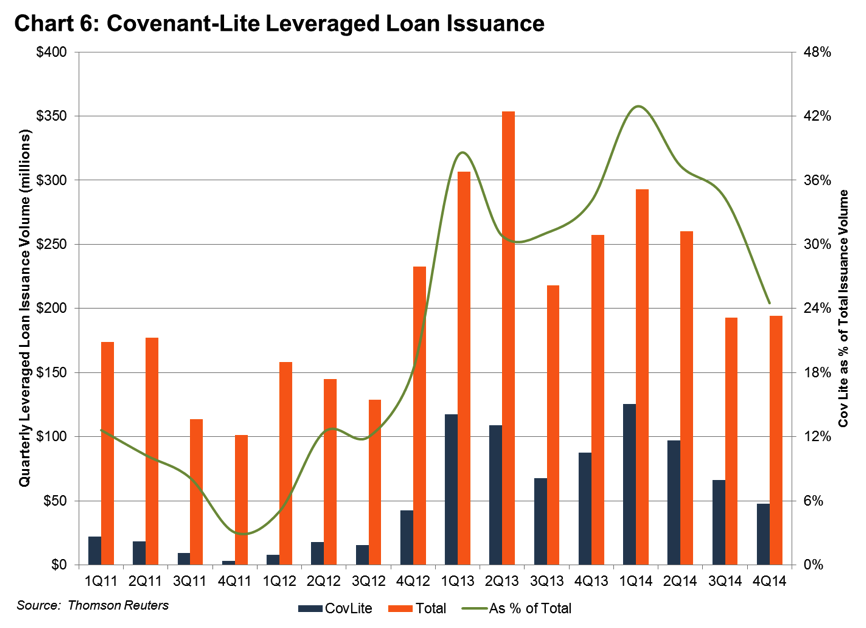

Beyond changing market sentiment evident in yield spreads, the principal cause of material adjustment to fair value marks for credit investments is changes in the likelihood of default or other credit impairment. Traditionally, credit investors have relied on loan covenants with borrowers to enhance the protection of their capital and to function as an early-warning system in the event of deteriorating operating fundamentals on the part of borrowers. As in the last credit cycle, abundant liquidity has granted borrowers the opportunity to negotiate more favorable (from the borrowers’ perspective) covenant terms. According to data in Thomson Reuter’s Leveraged Loan Monthly, so-called “covenant-lite” loans comprised over 35% of total leveraged loan issuance in 2014 (and a similar proportion in the first two months of 2015).

The publicly-traded business development companies, or BDCs, provide an open window on fair value marks for middle market credit investors. The BDCs are noteworthy on at least two accounts: (1) their portfolio marks are disclosed each quarter on an asset-by-asset basis, and (2) the credits they underwrite (high single-digit to low double-digit coupon senior and subordinated loans to middle market companies) are likely candidates to serve as the proverbial coal-mine canaries in the event credit experience deteriorates. Though many BDC management teams remain sanguine in the credit outlook for their respective portfolios, some cracks are beginning to emerge. Triangle Capital (TCAP) is a $1 billion BDC with a lending portfolio consisting of approximately 100 middle market borrowers. On their recent 4Q14 earnings conference call, TCAP management noted an uptick in their nonaccrual rate to 5.8%, a level described as “slightly higher than our long-term average nonaccrual rate of approximately 4%.” Whether the trends manifest in TCAP’s portfolio turn out to be representative of the broader credit universe remains to be seen, but at a minimum, it serves as a reminder that the Fed’s accommodative monetary policy and the multi-year economic recovery have not eradicated credit risk. Relatively attractive coupons are cold comfort if principal is not returned.

Implications for Fair Value Marks in 2015

For both equity and credit funds, there are indications that the “easy” portfolio valuations of the past two years may come to an end in 2015. Those who were around in the 2007-2010 period recall how challenging portfolio marks can be when equity markets fall, credit performance falters, or liquidity evaporates. Of course, we have no idea whether any of those conditions will materialize in 2015, but eventually, determining fair value marks will become more difficult. And not surprisingly, the scrutiny attendant upon such marks from judges (i.e., regulators, investors, and auditors) will be highest when the “degree of difficulty” is also high.

Related Links

- Credit Marks, Asset Yields and Dividend Capacity Are Going to Get More Scrutiny

- Credit Spread Blues & Portfolio Valuation Marks

- Valuation Best Practices for Venture Capital Funds

- Valuation Best Practices for Alternative Investment Funds

Mercer Capital’s Financial Reporting Blog

Mercer Capital monitors the latest financial reporting news relevant to CFOs and financial managers. The Financial Reporting Blog is updated weekly. Follow us on Twitter at @MercerFairValue.