One of the perennial controversies in business valuation is the estimation of so-called control premiums. Following the closing of the comment period on the Appraisal Foundation’s white paper on the topic, control premiums were back in the news last week with announced acquisition of Keurig Green Mountain by JAB Holdings. The transaction’s $92 per share purchase price rewarded investors with a 78% premium to the previous closing price. Compared to the often-cited range of benchmark control premiums between 30% and 40%, the JAB offer is an outlier. As such, what can we learn about control premiums by examining the proposed Keurig transaction a bit more closely?

Who is Keurig?

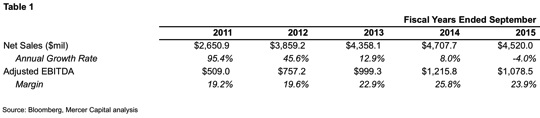

Keurig sells specialty coffee, coffeemakers, teas and other beverages in the United States and Canada. The Company’s single-serve coffee makers are found on the countertops of over 20 million households, and the corresponding K-Cup coffee pods occupy significant shelf space in grocery and department stores. Historical financial results for Keurig are summarized in Table 1.

Revenues grew rapidly during the early part of the decade as the Company’s installed base of brewers expanded. Growth moderated in fiscal 2013 and 2014 before actually turning negative in 2015. The Company began paying a quarterly dividend in January 2014. Introduced in 2015, Keurig’s heralded cold-brew system for carbonated soft drinks was not well-received by the market.

Establishing a Baseline Set of Market Participant Expectations

The primary message of the Appraisal Foundation white paper is that buyers do not offer premiums simply for the sake of gaining control, but rather, because through exercising the prerogatives of control, those buyers expect to generate economic benefits (in the form of enhanced cash flows and growth, or a lower cost of capital). As a preliminary step to assessing the potential economic benefits available to a market participant for a controlling interest in a company, it is helpful to establish a baseline cash flow forecast and WACC that conforms to the pre-transaction, “foundation” value of the business.

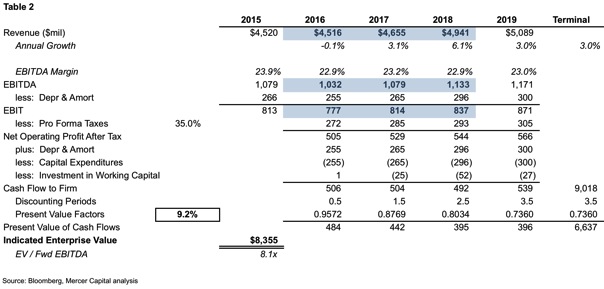

The analysis in Table 2 is based on market-consensus earnings estimates obtained from Bloomberg.

Prior to the transaction, Keurig’s stock price represented an enterprise value of approximately $8.4 billion, or 8.1x forecast fiscal 2016 EBITDA. Given the market consensus earnings forecast through 2018 (and a series of generally benign assumptions regarding other cash flow items and long-term growth), the market price implied a WACC of approximately 9.2%.

Assessing Changes to Cash Flow, Risk, and Growth

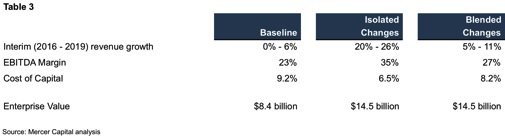

The JAB Holdings offer corresponds to an enterprise value of approximately $14.5 billion, or 14.0x forward EBITDA. Using the analysis in Table 1 as a base, we examined the implied adjustments to near-term revenue growth, EBITDA margin, and cost of capital that, individually, would generate an enterprise value equal to that implied by the JAB Holdings offer. Finally, we evaluated a composite set of changes to each factor that, in concert, generate a $14.5 billion enterprise value. The results of the analysis are summarized in Table 3.

If there were no adjustments to market consensus expectations regarding EBITDA margin and cost of capital, JAB would need to anticipate incremental near-term revenue growth of 20% to justify the acquisition premium. Likewise, if revenue growth and cost of capital assumptions were unchanged, projected EBITDA margins would need to climb to 35% from the baseline level of 23%. While those isolated changes may strain credibility, the rightmost column summarizes the impact of smaller changes to each of the three primary value drivers. There are myriad combinations that would yield the same enterprise value; the noted adjustments represent a combination that is likely to be more representative of actual buyer expectations than any of the isolated adjustments identified in the middle column.

Market Participants

The analysis in Table 3 reflects the terms of the JAB Holdings acquisition offer. Some background on JAB Holdings provides additional perspective on the offer. Acquirers are often identified as either “financial” (private equity) or “strategic” (competitors, customers, or suppliers). As described in this profile from BloombergBusiness earlier this year, JAB seems to share traits of both acquirer types. Owned by the Reimann family of Germany, JAB has invested in a number of consumer brand businesses, and began acquiring various global coffee assets in 2012, including Senseo, the coffee business of Mondelez, Caribou Coffee, and roaster/retailer Peet’s [also premium “third-wave” micro-assets Stumptown and Intelligentsia]. Given this profile, the combination of incremental revenue growth, enhanced margins, and lower capital costs noted in Table 2 makes sense. The profile linked above includes a quote from JAB’s chairman Bart Becht summarizing the firm’s recipe for investing success: “We bought consumer-goods businesses from companies for which it wasn’t the primary interest. You could make a lot of changes and have a big impact.” Translated into fair value idiom, they focus on expected changes to cash flow, risk, and growth. Acquisition premiums are outputs of their process, not inputs that determine what price to pay. JAB Capital is in many respects the platonic ideal of a market participant for controlling interests in businesses.

Premium in Context

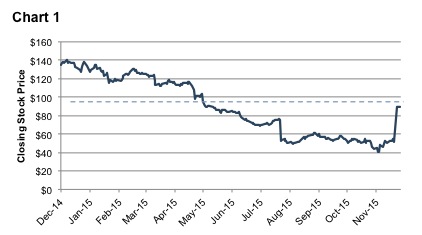

Does the foregoing suggest that – in measuring fair value for reporting units – acquisition premiums on the order of 75% are always reasonable? Of course not. Just as Keurig’s ubiquitous single-serve coffee pods are designed to deliver a tailored beverage experience, the facts and circumstances surrounding every fair value measurement will be unique. As Chart 1 illustrates, although the announced transaction price represented a substantial premium to the prior day’s trading price, the transaction price represents a 65% discount to the Company’s share price at the beginning of the year.

The stock price chart underscores the unique attributes of Keurig. While a declining stock price does not by itself support a large acquisition premium, a stock’s trading history may provide some support for the overall reasonableness of the inputs used to derive fair value from the perspective of a market participant acquiring control of a business. For Keurig, the decreasing stock price through 2015 had been a boon to short sellers, who learned that one motivated acquirer can quickly erase paper profits on short trades. In any event, the task of a fair value specialist is to thoroughly investigate the unique attributes of a subject business enterprise and carefully identify what factors may cause a market participant to pay an acquisition premium.

In the end, a fair value measurement is probably not all that different from a cup of coffee – the final product can only be as good as the inputs.

Mr. Harms is a member of the Appraisal Foundation’s working group on control premiums. The views expressed in this blog post are his own and do not reflect those of other working group members or the Appraisal Foundation.

Related Links

- What’s the Control Premium?

- In the Eye of the Beholder: Increasing SEC Scrutiny of Public Company Fair Value Marks

- Yes, Virginia, the Cost of Capital Really Is Low

Mercer Capital’s Financial Reporting Blog

Mercer Capital monitors the latest financial reporting news relevant to CFOs and financial managers. The Financial Reporting Blog is updated weekly. Follow us on Twitter at @MercerFairValue.