2017 Was Especially Kind to the RIA Community

Favorable market conditions over the last year have lifted RIA market caps to all-time highs yet again as AUM balances continue to climb with the major indices. Market gains have apparently trumped fee compression, fund outflows, regulatory overhang, rising costs, and a host of other industry headwinds that have dominated the headlines in recent years. This doesn’t necessarily mean the press is wrong about some of the problems facing the industry (admittedly, we’ve blogged about many of them), but it may be missing (or at least not reporting on) the real story. The combination of market appreciation and operating leverage have precipitated significant improvements in profitability since the Financial Crisis, eliciting a favorable response from investors despite everything we’ve been reading (and writing) about the industry.

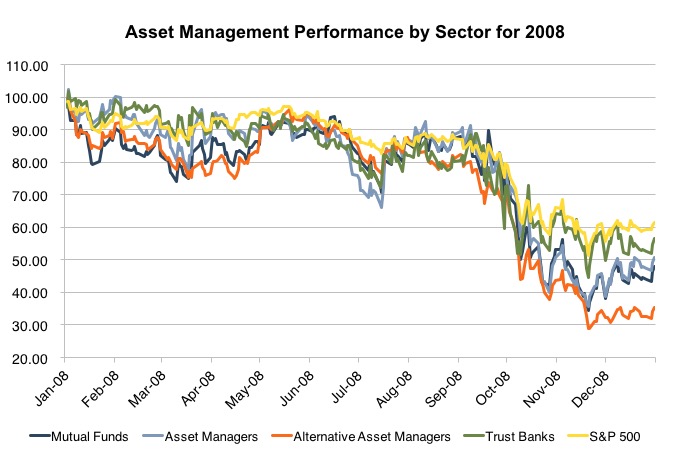

The only problem is that market movements and operating leverage are a doubled edged sword. Upward or downward trends in the broader market tend to have a magnified effect on the stock prices of asset managers. While 2017 has been a great year for the S&P 500 and an even better year for most categories of RIAs, the reverse can also be true: a bad year for the market can mean an even worse year for asset managers. Historically, corrections and bear markets have led to more precipitous declines in profitability due to the presence of fixed expenses in most RIA’s capital structure. We use 2008 as an example of how the market for asset manager stocks reacts to downturns:

Taking a closer look at last year’s pricing reveals that trust bank stocks have generally underperformed other classes of asset managers. This performance comes despite a steadily rising yield curve, which portends higher NIM spreads and reinvestment income. Our trust bank index gained 17% over the last year, in line with the S&P 500 but below most other categories of asset managers that tend to react more favorably to rising market conditions.

Taking a closer look at last year’s pricing reveals that trust bank stocks have generally underperformed other classes of asset managers. This performance comes despite a steadily rising yield curve, which portends higher NIM spreads and reinvestment income. Our trust bank index gained 17% over the last year, in line with the S&P 500 but below most other categories of asset managers that tend to react more favorably to rising market conditions.

Traditional asset managers ended the year up 33%, outperforming the S&P 500 and most other categories of asset managers. Publicly traded alternative asset managers also performed well during 2017, although most of the sector’s gains occurred during the first half of the year. Alternative asset managers are still reeling from poor investment returns over the last decade. The value-added proposition (alpha net of fees) has been virtually non-existent for many hedge funds and PE firms over this period despite the sector’s recent gains.

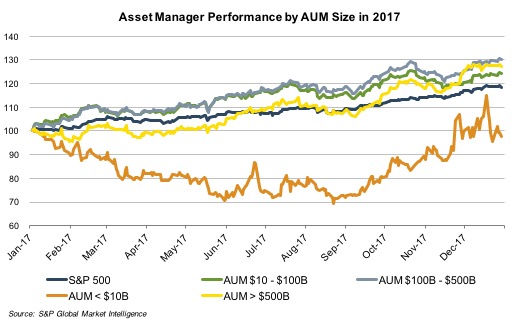

The RIA size graph seems to imply that smaller RIAs have bounced back in the fourth quarter after being down nearly 30% at the end of the third quarter. The reality, though, is that this segment is the least diversified (only two components, Hennessy Advisors and US Global Investors, both of which are thinly traded) and certainly not a good representation of how RIAs with under $10 billion in AUM are actually performing. Specifically, Hennessy has performed poorly throughout 2017 due in part to recent sub-par investment performance from its Cornerstone Growth Fund. Hennessey’s poor performance was more than offset by US Global Investors, which was up nearly 100% in the fourth quarter alone due to its strategic investment in HIVE Blockchain Technologies, a company which mines bitcoin (although just having blockchain in the name likely would have been enough). So while most of our clients fall under this size category, we can definitively say that these businesses (in aggregate) haven’t followed the pricing trends suggested by this graph. Other sizes of publicly traded asset managers have all outperformed the market over this period, with the $100 to $500 billion AUM group seeing the largest gains.

Market Outlook

The outlook for these businesses is similarly market driven – though it does vary by sector. Trust banks are more susceptible to changes in interest rates and yield curve positioning. Alternative asset managers tend to be more idiosyncratic but still influenced by investor sentiment regarding their hard-to-value assets. Mutual funds and traditional asset managers are more vulnerable to trends in active and passive investing. All are poised for another great year in 2018 as long as the market holds up in the coming months.

Mercer Capital’s RIA Valuation Insights Blog

The RIA Valuation Insights Blog presents a weekly update on issues important to the Asset Management Industry. Follow us on Twitter @RIA_Mercer.