Q2 2019 Asset Manager M&A Trends

Asset and Wealth Manager M&A Keeping Pace with 2018’s Record Levels

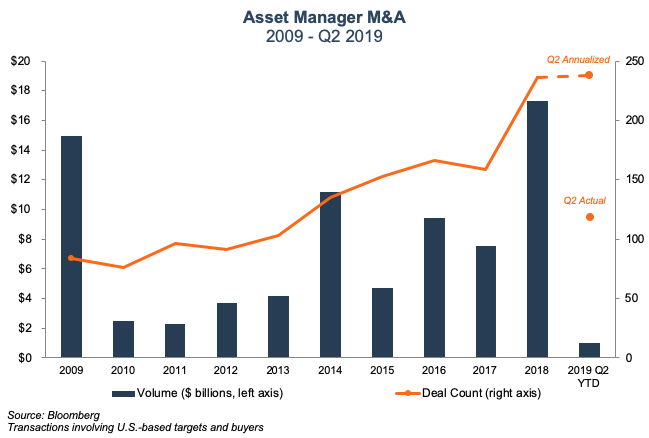

Through the first half of 2019, asset and wealth manager M&A has kept pace with 2018, which was the busiest year for sector M&A over the last decade. M&A activity in the back half of 2019 is poised to continue at a rapid pace as business fundamentals and consolidation pressures continue to drive deal activity. Several trends, which have driven the uptick in sector M&A in recent years, have continued into 2019, including increasing activity by RIA aggregators and rising cost pressures.

Total deal count during the first half of the year is on pace to slightly exceed 2018’s record levels. Reported deal value during the first half of 2019 was down significantly, although the quarterly data tends to be lumpy and many deals have undisclosed pricing.

Acquisitions by (and of) RIA consolidators continue to be a theme for the sector. The largest deal of the second quarter was Goldman Sachs’s $750 million acquisition of RIA consolidator, United Capital Partners. The deal is a notable bid to enter the mass-affluent wealth management market for Goldman Sachs. For the rest of the industry, Goldman’s entrance into the RIA consolidator space is yet another headline that illustrates the broad investor interest in the consolidator model.

If there was any doubt of that fact, just a few weeks ago it was reported that Mercer Advisors (no relation), an RIA consolidator managing $16 billion, is up for sale by its PE backer, Genstar Capital. Mercer could fetch an estimated $700 million price tag, putting it in a similar size bracket as the United Capital acquisition.

These RIA aggregators have been active acquirers in the space themselves, with Mercer Advisors and United Capital Advisors each acquiring multiple RIAs during 2018 and the first half of 2019.

The wealth management consolidator Focus Financial Partners (FOCS) has also been active since its July 2018 IPO, although acquisitions slowed during the second quarter of 2019. Focus announced a total of eight transactions during the second quarter, most of which were smaller sub-acquisitions by partner firms, except for the acquisition of William, Jones & Associates, a New York-based RIA managing $7 billion.

The prospect of using buyer resources to facilitate their own M&A may be a key motivation.

Sub-acquisitions by Focus Financial’s partner firms and other firms owned by RIA consolidators are a growing M&A driver for the industry. These acquisitions are typically much smaller and are facilitated by the balance sheet and M&A experience of the consolidators. For some RIAs acquired by consolidators, the prospect of using buyer resources to facilitate their own M&A may be a key motivation for joining the consolidator in the first place. For the consolidators themselves, these deals offer a way to drive growth and extend their reach into the smaller RIA market in a way that is scalable and doesn’t involve going there directly.

Consolidation Rationales

The underpinnings of the M&A trend we’ve seen in the sector include the lack of internal succession planning at many RIAs and the increasing importance of scale against a backdrop of rising costs and declining fees. While these factors are nothing new, sector M&A has historically been less than we might expect given the consolidation pressures the industry faces.

Consolidating RIAs, which are typically something close to “owner-operated” businesses, is no easy task. The risks include cultural incompatibility, lack of management incentive, and a size-impeding alpha generation. Many RIA consolidators structure deals to mitigate these problems by providing management with a continued interest in the economics of the acquired firm, while allowing it to retain its own branding and culture. Other acquires take a more involved approach, unifying branding and presenting a homogeneous front to clients in an approach that may offer more synergies, but may carry more risks as well.

Market Impact

In 2019, equity markets have largely recovered and trended upwards.

Deal activity in 2018 was strong despite the volatile market conditions that emerged in the back half of the year. So far in 2019, equity markets have largely recovered and trended upwards. Publicly traded asset managers have lagged the broader market so far in 2019, suggesting that investor sentiment for the sector has waned after the volatility seen at year-end 2018.

M&A Outlook

Consolidation pressures in the industry are largely the result of secular trends. On the revenue side, realized fees continue to decrease as funds flow from active to passive. On the cost side, an evolving regulatory environment threatens increasing technology and compliance costs. The continuation of these trends will pressure RIAs to seek scale, which will in turn drive further M&A activity.

With over 11,000 RIAs currently operating in the U.S., the industry is still very fragmented and ripe for consolidation. Given the uncertainty of asset flows in the sector, we expect firms to continue to seek bolt-on acquisitions that offer scale and known cost savings from back office efficiencies. Expanding distribution footprints and product offerings will also continue to be a key acquisition rationale as firms struggle with organic growth and margin compression. An aging ownership base is another impetus. The recent market volatility will also be a key consideration for both sellers and buyers in 2019.