FinTech companies are the emerging and hyped sector of the financial services industry. Looking at FinTech’s recent activity, people can see that many of these companies begin as start-ups and a few exciting years later, are able to raise millions of dollars in hopes of becoming the next “unicorn” – an industry term describing a tech company valued at a billion dollars or more. While this business trajectory may seem simple and attractive, FinTech companies usually have a highly complex structure made up of many investors of different origins, including venture, corporate, and/or private equity, all with different preferences and capital structures.

Valuing a FinTech company can be very complicated and difficult, but carries important significance for employees, investors, and stakeholders for the company. While all FinTech companies have large differences, including what niche (payments, solutions, technologies, etc.) they operate in or what stage of development the company is in, understanding the value of a FinTech company is critically important. More specifically, within the FinTech industry, an exciting niche termed InsurTech is emerging and threatening to change the traditional state of the insurance industry.

InsurTech Niche

InsurTech is a fast growing niche that operates in a massive global insurance industry with premium revenues of about $5 trillion annually. InsurTech is the term applied to many companies that are using technology to disrupt the traditional insurance industry landscape. InsurTech has high growth prospects and the potential for InsurTech to innovate and disrupt remains large. Funding for InsurTech companies in recent years has spiked, especially for early-stage companies. Incumbents in the insurance industry have been slow to adopt disruptive, high-growth InsurTech, partly because insurance is so massive and has been around for such a long time. Additionally, many traditional insurance companies can benefit from InsurTech solutions that serve to enhance customer satisfaction and improve the efficiency of operations by leveraging technology and enhancing the delivery of certain insurance offerings and solutions through digital channels.

Technology and innovation have disrupted many other long-established industries, such as the impact of medical technology in the healthcare industry. Insurance players, who maintain legacy systems believe that established customer connections will reduce the threat of InsurTech. However, this may not be the best strategy because insurance is often purchased begrudgingly. The historically strained relationship between customers and carriers is a rather vulnerable point along the insurance value chain. InsurTech companies can offer innovative technology that creates more touchpoints for customers and reduces many customer pain points.

Market Considerations

Understanding how well a given InsurTech company is doing within this FinTech niche is one of the most important factors in determining its value. Market dynamics such as market size, potential market available, and growth prospects are important to understand. A valuation will consider absolute market value, existing competitors, and existing incumbents. The regulatory environment is another important consideration when valuing an InsurTech company. Financial services, such as banks and insurance companies, are heavily regulated, so understanding the rules and regulations is necessary for developing an accurate valuation.

Like other FinTech niches, certain solutions within InsurTech are relatively new and have the potential to disrupt the entire insurance industry. Since many industry incumbents have been slow to adopt this new technology, the range of this innovation has yet to be fully felt and rules/regulations have yet to change. While regulatory stability may seem favorable now, concrete rules and regulations are complex and can be hard to predict as regulators react to rising InsurTech involvement. Understanding these complexities is important to valuing InsurTech companies, as these regulations could help or hinder an InsurTech’s growth potential.

Company Considerations

When valuing a startup, quantitative information (financial and operating history) is limited; therefore, qualitative information can be extremely important in determining a company’s value. The quality and experience of the management team can be important. Knowledge of the insurance industry including understanding customer preferences, technology integration, the competitive and regulatory environments can enhance an InsurTech’s company value.

An InsurTech company’s ownership of intellectual property and other intangible assets, like strategic partnerships, all else equal, should be considered and could increase a company’s value, assuming they are in place and well documented. When in place and demonstrated, intangibles are an important qualitative consideration.

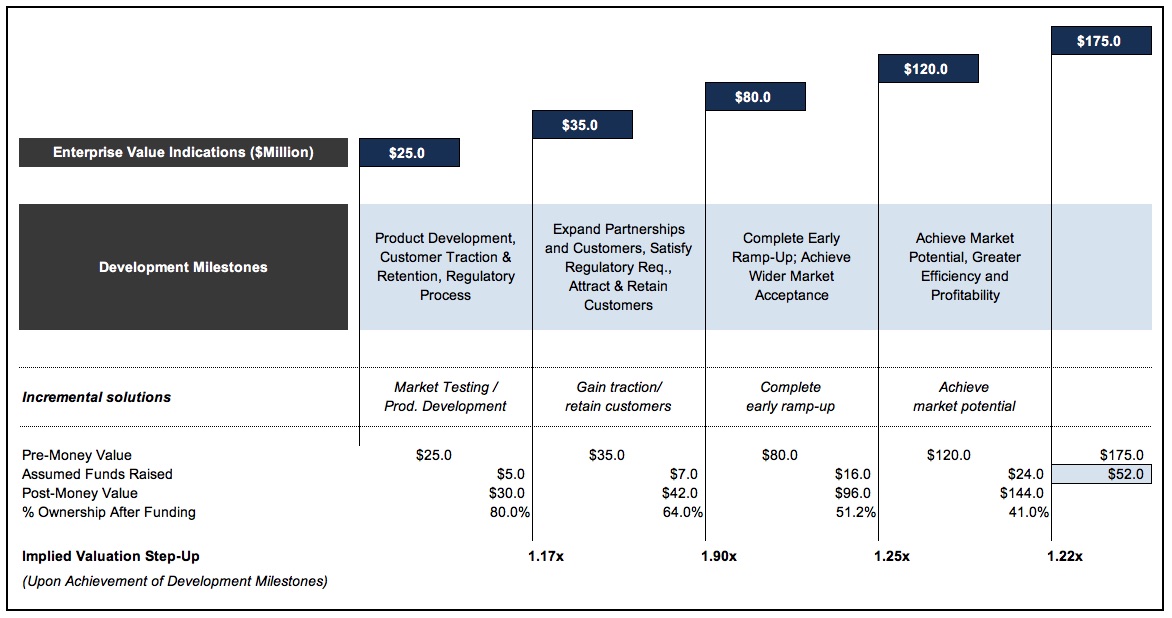

The stage of development of a FinTech company can also impact its value. Companies typically set milestones and track their own progress, and meeting these milestones might affect their valuation. Milestones usually include initial round financing, proof of concept, regulatory approval, obtaining a significant partner, and more.

Milestones are important to set and track as the more milestones a startup meets, the less uncertainty exists and the more value is created. For example, an InsurTech company with established technology, increased customer touchpoints, and the potential to increase revenues will be more valuable to a potential acquirer than a newer startup. In addition, meeting later stage milestones often provide greater value than meeting early stage milestones. When the valuation considers future funding rounds and the potential dilution from additional capital raises, a staged financing model is often prepared and the valuation will vary at different stages as shown below.

Valuation Approaches

As InsurTech companies enhance business operations and reduce costs, valuations for these companies will become more important. There are three common approaches to determining business value: asset approach, income approach, and market approach. Each valuation approach is typically considered and then weighted accordingly to provide an indicated value or a range of value for the company, and ultimately, the specific interest or share class of the company.

The Asset Approach

The asset approach determines the value of a business by examining the cost that would be incurred by the relevant party to reassemble the company’s assets and liabilities. This approach is generally inappropriate for technology startups as they are generally not capital intensive businesses until the company has completed funding rounds. However, it can be instructive to consider the potential costs and time that the company has undertaken in order to develop proprietary technology and other intangibles.

The Market Approach

The market approach determines the value of a company by utilizing valuation metrics from transactions in comparable companies or historical transactions in the company. Consideration of valuation metrics can provide meaningful indications for startups that have completed multiple funding rounds, but can be complicated by different preferences and rights with different share classes.

Regardless of complications, share prices can provide helpful valuation anchors to test the valuation range. Market data of publicly traded companies and acquisitions can be helpful in determining key valuation inputs for InsurTech companies. For early-stage companies, market metrics can provide valuable insight into potential valuations and financial performance once the InsurTech company matures. For already mature enterprises, recent financial performance can be compiled to serve as a valuable benchmarking tool.

Investors can discern how the market might value an InsurTech company based on pricing information from comparable InsurTech companies or recent acquisitions of comparable InsurTech companies.

The Income Approach

The income approach can also provide a meaningful indication of value for a FinTech company. This relies on considerations for the business’ expected cash flows, risk, and growth prospects.

The most common income approach method is the discount cash flow (DCF) method, which determines value based upon the present value of the expected cash flows for the enterprise. The DCF method projects the expected profitability of a company over a discrete period and prices the profitability using an expected rate of return, or a discount rate. The combination of present values of forecasted cash flows provides the indication of value for a specific set of assumptions.

For startup InsurTech companies, cash flow forecasts are often characterized by a period of operating losses, capital needs, and expected payoffs as profitability improves or some exit event, like an acquisition, occurs. Additionally, investors and analysts often consider multiple scenarios for early-stage companies both in terms of cash flows and exit outcomes (IPO, sale to a strategic or financial buyer, etc.), which can lead to the use of a probability weighted expected return model (PWERM) for valuation.

Putting it Together

Given their complexity, multiple valuation approaches and methods are often considered to provide lenses through which to assess value of InsurTech and FinTech companies and generate tests of reasonableness against which different indications of value can be evaluated.It is important to note that these different methods are not expected to align perfectly. Value indicators from the market approach can be rather volatile and investors often think longer-term. More enduring indicators from value can often come from income approaches, such as DCF models.

Valuation of an InsurTech company can be vital to measure realistic growth, to plan progression, and to secure employee and investor interest. Given the complexities in valuing private FinTech and InsurTech companies and the ability for the market/regulatory environment to shift quickly, it is important to have a valuation expert who can adequately assess the value of the company and understand the prevalent market trends.