Adapted from the new book Creating Strategic Value Through Financial Technology by Jay D. Wilson, Jr., CFA, ASA, CBA.

In order to understand how FinTech can help community banks create strategic value, let us take a closer look at the issues facing community banks and discuss how FinTech can help improve performance and valuation. This is significant, particularly in the U.S., as community banks compose an important part of the economy, constitute the majority of banks in the U.S. and are collectively the largest providers of certain loan types such as agricultural and small business lending.

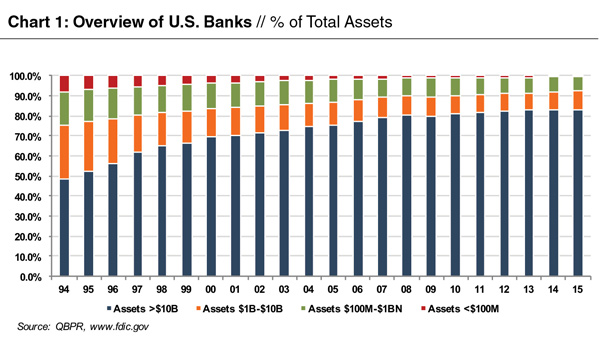

There are nearly 6,000 community banks with 51,000 locations in the U.S. (includes commercial banks, thrifts, and savings institutions). While community banks constitute the vast majority of banks (approximately 90% of U.S. banks have assets below $1 billion), the majority of banking industry assets are controlled by a small number of extremely large banks. These larger banks have acquired assets more quickly than community banks in the last few decades (as shown in Chart 1).

In addition to competition from larger banks and industry headwinds, community bankers are also attempting to assess and respond to the growing threat from the vast array of FinTech companies and startups taking aim at the banking sector. For perspective, a group of community bankers meeting with the FDIC in mid-2016 noted that FinTech poses the largest threat to community banks. One executive indicated that the payment systems “are the scariest” as consumers are already starting to use FinTech applications like Venmo and PayPal to send peer-to-peer payments. Another banker went on to note, “What’s particularly concerning about [the rise of FinTech] for us is the pace of change and the fact that it’s coming so quickly.”

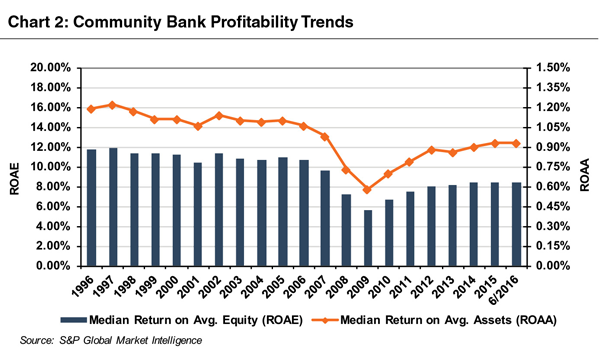

These significant competitive pressures combined with other industry headwinds such as higher regulatory and compliance costs and a historically low interest rate environment have hurt returns on equity (ROEs) for community banks (Chart 2).

While many bankers view FinTech as a significant threat, FinTech also has the potential to assist the community banking sector. FinTech offers the potential to improve the health of community banks by enhancing performance and improving profitability and ROEs back to historical levels.

One way to better understand how FinTech can assist community banks is to understand where the Big Banks are outperforming smaller banks. Big Banks (defined as those with assets greater than $5 billion) have outperformed community banks consistently for many years. In the 20-year period from 1996 to 2016, Big Banks reported a higher return on asset (ROA) than community banks in each period except for 2009 (the depths of the financial crisis). Interestingly though, the source of outperformance is not due to net interest margin, perhaps the most common performance metric that bankers often focus on. Community banks had consistently higher net interest margins than Big Banks in each year over that 20-year period (1996-2016). Rather, the outperformance of the Big Banks can be attributed to their generation of greater non-spread revenues (i.e., non-interest income) and lower non-interest expense (i.e., lower efficiency ratios).

While FinTech can benefit community banks in a number of areas, FinTech offers some specific solutions where community banks have historically underperformed: non-interest income and efficiency. To enhance non-interest income, community banks may consider a number of FinTech innovations in niches like payments, insurance, and wealth management. Since many community banks have minimal personnel and legacy systems in these areas, they may be more apt to try a new FinTech platform in these niches. For example, a partnership with a robo-advisor might be viewed more favorably by a community bank as it represents a new source of potential revenue, another service to offer their customers and it will not cannibalize their existing trust or wealth management staff since they have minimal existing wealth management personnel.

FinTech can also enhance efficiency ratios and reduce expenses for community banks. Branch networks are the largest cost of community banks and serving customers through digital banking costs significantly less than traditional in-branch services and interactions with customers. For example, branch networks make up approximately 47% of banks’ operating costs and 54% of that branch expenditure goes to staffing. Conversely, the cost of ATM and online-based transactions are less than 10% of the cost of paper-based branch transactions in which tellers are involved. In addition to the benefits from customers shifting to digital transactions, community banks can utilize FinTech to assist with lowering regulatory/compliance costs by leveraging “reg-tech” solutions.

To illustrate the potential financial impact of transitioning customers to digital transactions for community banks, let’s assume that a mobile transaction saves the bank approximately $3.85 per branch transaction. If we assume that FinTech Community Bank has 20,000 deposit accounts and each account shifts two transactions per month to mobile from in-person branch visits, the bank would save approximately $150 thousand per month and approximately $1.8 million annually. These enhanced earnings would serve to enhance efficiency and improve shareholder returns and the bank’s valuation.

Moving beyond non-interest income and efficiency ratios, FinTech also offers a number of other potential benefits for community banks. FinTech can be used to help community banks compete against Big Banks more effectively by minimizing the impact of scale as more customers carry their branch in their pocket. By leveraging FinTech solutions, smaller banks can more easily compete against a large bank’s footprint digitally via the web or a mobile device. FinTech also offers many community banks an opportunity to enhance loan portfolio diversification and regain some market share after years of losing ground in certain segments (such as consumer, mortgage, auto, and student).

FinTech can also provide an additional touch point to improve customer retention and preference. While data is limited, some studies have shown that customer loyalty (i.e., retention) is higher for those customers that use mobile offerings and digital banking (online and mobile) is increasingly preferred by customers. While digital is clearly growing among customer preference, data has also shown that digital-only customers can be less engaged, loyal, and profitable than those who interact with the bank through a combination of interactions across multiple channels (digital, branches, etc.). So community banks that rely more heavily on their branch networks should find it beneficial to add digital services to complement their traditional offerings in order to enhance customer retention and preference.

As technological advances continue to penetrate the banking industry, community banks will need to leverage technology in order to more effectively market to and serve small businesses and consumers in an evolving environment. Community banks will likely increasingly rely on a model that makes widespread use of ATM’s, the Internet, mobile apps and algorithm driven decision making, enabling them to deliver their services to customers in a streamlined and efficient manner.

Our world is changing quickly. FinTech can represent an opportunity for community banks. Understanding how FinTech will impact your institution and your response is critical today. Many community banks are actively surveying the FinTech landscape and pursuing a strategy to improve their digital footprint and services through partnerships with FinTech companies. Our new book, Creating Strategic Value Through Financial Technology, can help those banks considering their FinTech strategy as it provides information on the FinTech landscape and provides an overview of a few prominent FinTech niches (payments, wealthtech, insurtech, and banktech), case studies of successful (and unsuccessful FinTech companies), as well as an overview of some key ways to value FinTech companies and assess value creation when structuring FinTech acquisitions, investments, and/or partnerships.

Whatever your strategy, understanding how FinTech fits in and adapting to the current environment is incumbent upon any institution that seeks to compete effectively and Mercer Capital will be glad to assist. We have successfully worked with both traditional financial incumbents (banks, insurance, wealth managers) as well as FinTech companies in a number of strategic planning and valuation projects over the years.

This article originally appeared in Mercer Capital’s Bank Watch, April 2017.