Earlier this year, we considered the impact of the Tax Cuts and Jobs Act of 2017 (“TCJA”) on purchase price allocations. In this article, we turn our focus to the impact of the TCJA on goodwill impairment testing. Changes to the tax code will affect both the qualitative assessment (often referred to as Step Zero) and quantitative impairment test.

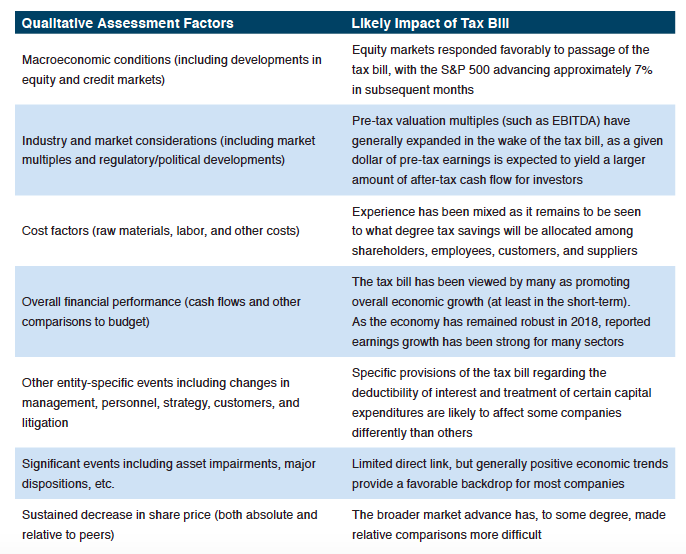

Companies preparing a qualitative assessment are required to assess “relevant events and circumstances” to evaluate whether it is more likely than not that goodwill is impaired. ASC 350 includes a list of eight such potential events and circumstances.

The same features which, on balance, have made it more likely that reporting units will garner a favorable qualitative assessment also contribute to the fair value of reporting units under the quantitative assessment.

The Tax Cuts and Jobs Act of 2017 is a material factor to be considered in both qualitative and quantitative assessments of goodwill impairment in 2018. While the provisions are not uniformly favorable to higher valuations, the balance of factors suggests that goodwill impairments will be less likely in the coming impairment cycle. To discuss how the new tax regime affects your company’s goodwill impairment more specifically, please give one of our professionals a call.

Originally appeared in Mercer Capital’s Financial Reporting Update: Goodwill Impairment