During the first Trump administration, the Tax Cuts and Jobs Act (“TCJA”) introduced substantial modifications to the tax code, including significant reductions to estate tax liabilities. These reductions, however, were designed to sunset at the end of 2025, and addressing the expiring provisions became a priority for the current Trump administration. These were addressed in the One Big Beautiful Bill Act (“OBBBA”), an extensive legislative package touching on a variety of tax and spending policies. After a series of late-stage amendments, the OBBBA passed both chambers of Congress and was signed into law on July 4.

In this issue of Value Matters, we examine the OBBBA’s provisions from a valuation perspective, focusing on implications pertinent to tax and estate planning professionals.

One of the key determinants of value of an interest in a company – be it a family-owned operating company or a real estate holding company – is the cash flow generated by the company and available to the shareholders for either distribution or reinvestment. The cash flow generated by a company directly impacts its valuation and the level of distributions made to shareholders impacts the magnitude of discounts applicable to nonmarketable minority interests in companies.

The OBBBA directly impacts cash flows in several key ways.

The exclusion permitted related to sales of Qualified Small Business Stock (“QSBS”) has also been expanded. For qualified five-year holdings, 100% of the capital gains up to $15 million is exempted from capital gains taxes. The exclusion cap is indexed to inflation beginning in 2026.

The OBBBA also introduced partial exclusions for QSBS shares held for shorter holding periods – 50% of gains are exempted for three-year holdings and 75% of gains are exempted for four-year holdings.

The QSBS rules apply only to C corporations in non-service industries (for example, tech or retail) but can be advantageous to those planning to transfer shares across generations.

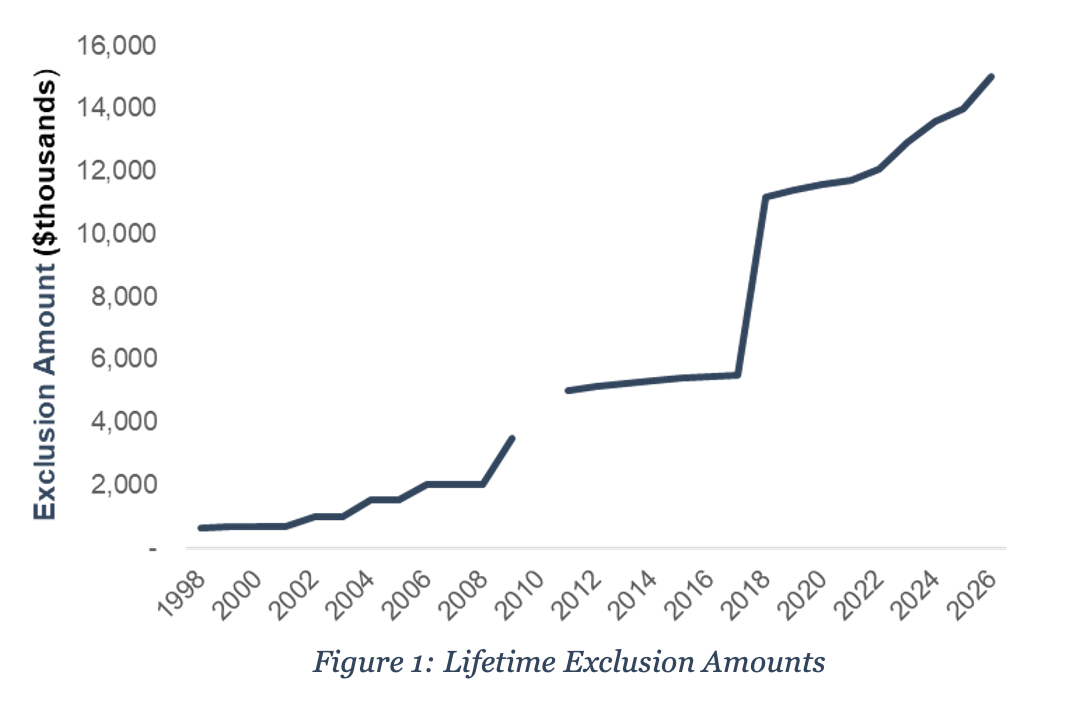

Of most immediate relevance to estate planners is the substantial revision of estate tax exemption thresholds. The lifetime exclusion amount – the amount under which estate and gift taxes are not owed – was increased to $15 million for single filers and $30 million for joint filers beginning in 2026. This amount is indexed to inflation and will increase in future years.

As shown in Figure 1, the lifetime exclusion amount has varied over time. The TCJA doubled the inflation-indexed exclusion amount from a base of $5 million to $10 million (or $5.49 million in 2017 to $11.18 million in 2018, after the inflation adjustment).

Absent the passage of the OBBBA, the expiration of TCJA in December 2025 would have resulted in the exclusion reverting back to the $5 million base level (which would have been just over $7 million in 2026 after the inflation adjustment).

It is also important to note that the estate exclusion amount is lifetime amount – gifts, estate, and generation-skipping transfers all work off of the same $15 million “pool” of exemption value. The actual rates applicable to gift and estate taxes are unchanged and portability between spouses remains.

Importantly, unlike the TCJA provisions, the OBBBA’s estate tax thresholds do not include sunset provisions, offering greater predictability. Nonetheless, future legislative changes remain a possibility, underscoring the importance of sustained, proactive planning.

Additionally, the OBBBA only impacts federal estate tax obligations; individual states may have their own estate tax rates and exemption levels. Taxpayers who maintain a course of consistent and vigilant estate planning will be best positioned to achieve their planning objectives and successfully thwart future challenges once the pendulum of enforcement activity and tax policies inevitably swing in the opposite direction.

As Ben Franklin observed over two hundred years ago, “in this world nothing can be said to be certain, except death and taxes.” In navigating these certainties, collaboration with experienced estate planners and valuation professionals is critical.

Feel free to reach out to us if you have any questions about the OBBBA’s impact on gift and estate tax valuations or to discuss a valuation issue in confidence.