The discount rate is the key factor in business valuation that converts future dollars into present value as of the valuation date. For a layperson, the discount rate utilized in a business valuation may appear to be subjective and pulled out of a hat. However, the discount rate is a crucial component of the valuation formula and must be assessed for the specific company at hand.

Using any method under the income approach, the valuation formula comes down to three things:

Ongoing (or expected) cash flow (or other measure of earnings)

Discount rate

Growth rate

In valuations that “feel” too high or too low, one of the potential culprits may be an aggressive discount rate, either on the high or low end. There are several generally accepted methodologies to build up discount rates employed by valuation analysts. In this article, we will examine the various components of a discount rate. Then, we will relate the discount rate to rates of return of other investments that should provide a commonsense road map for what is reasonable and what is not.

What Is a Discount Rate?

Companies with larger cash flows are likely to be more valuable, as are those with cash flows that are growing at a faster rate. Each of these statements makes perfect sense. Now, if the future cash flows are less certain, they are deemed to be riskier, which reduces the value of the business. The discount rate “discounts” future cash flows to a present value. As we have all heard, “a dollar today is better than a dollar tomorrow.” Measuring the present value of future earnings allows us to develop a value for a business today.

The discount rate goes by many names including “equity discount rate,” “return on investment,” “cost of capital,” and “rate of return.” For companies that use debt, the appropriate way to discount cashflows may be the weighted average cost of capital, or “WACC.” Thinking about a discount rate as a rate of return is likely the most intuitive approach.

Returns to an equity investor come after all other parties have been paid. Debt capital providers are paid before equity capital providers, typically at a fixed or floating interest rate (for example, a company’s line of credit could be 4.0% fixed rate or vary, such as 1% over the prime rate). After generating revenue, paying expenses and taxes, and reinvesting funds needed in the business, any remaining cash flow is shared by the equity investors. Because equity investors come last, they require the highest rate of return in order to provide equity capital to a business. Intuitively, this explains why the cost of equity, or “discount rate,” is higher than the cost of debt, or interest rate.

How to Build Up a Discount Rate

Before we delve into what is reasonable and what is not, one must first understand the components of a discount rate as these help the attorney understand how an appraiser estimates this rate. We describe the development of an equity discount rate with a description of each component below.

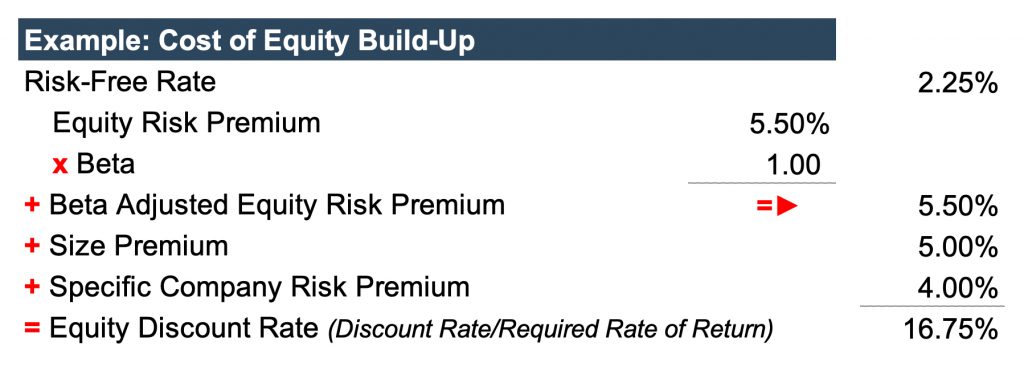

Risk-Free Rate: As alluded to previously, we would all prefer a dollar today over a dollar tomorrow, which both removes the uncertainty of receipt and quells any potential concerns about lost purchasing power from rising prices. To build up the discount rate, we begin with a base rate called the “risk-free rate,” which compensates for the time value of money. An example of a risk-free rate is the 20-Year Treasury Bond yield as of the valuation date. If an appraisal uses an alternative figure that is materially different than the prevailing rate, the assumption would likely require justification.

Equity Risk Premium: Next, to capture generic market risk for the equity market, appraisers employ an “equity risk premium,” frequently in the range of 4.0% to 7.0%, which captures what an investor would expect for an investment in the equity market over a less risky investment like the bond market. Again, something out of this range would likely require justification. [1]

Beta: The equity risk premium is then multiplied by a selected beta. The beta statistic measures a company’s exposure to market risks, with a beta of 1.0 indicating typical market risk. Low beta companies or industries are less correlated with market risk, while high beta companies are more exposed to market risk. For example: auto dealers and airlines tend to ebb and flow with the economy, doing well when the market is good and declining when economic activity contracts, meaning they tend to have betas of 1.0 or higher. In contrast, grocery stores tend to have a beta below 1.0. When the economy contracts, consumers increase their consumption at grocery stores instead of restaurants to save money. Consumers also need toilet paper regardless of the economic environment, and companies that sell such durable goods (like grocery stores) tend to be lower beta companies.

To this point, we have built up the equity discount rate under the Capital Asset Pricing Model (“CAPM”) for a diversified equity market investment.[2] The risk-free rate plus the equity risk premium (assuming a beta of 1.0) gives a rate of return of approximately 7.0% to 8.0%. This should sound familiar because money managers and retirement planners frequently say equity investors should anticipate investment returns on the order of 7.0%, or something in this range. While Mercer Capital makes no such investment advice, this is a reasonable consideration for large, diversified equity portfolios in the context of building up a discount rate for a smaller private company. However, in recognition of the greater risks inherent in privately held smaller companies, business valuation analysts frequently consider two other sources of risk premia: size and specific company.

Size Premium: Smaller companies tend to be subject to greater issues with concentration and diversification. Smaller companies also tend to have less access to capital, which tends to raise the cost of capital. To compensate for the higher level of risks as compared to the broad larger equity market, appraisers frequently add a premium of approximately 3.0% to 5.0% (or more, for very small businesses) to the discount rate when valuing smaller companies. To get an idea of reasonableness, we can consider the following example. A company valued at over $200 million may seem large, but it is actually relatively small when compared to most publicly traded companies. As such, a size premium would still apply, albeit on the lower end. Valuation analysts source these size premiums from data which provides empirical evidence in support of risks associated with smaller size. This data is updated annually, and providers such as Duff & Phelps are frequently cited.

Specific Company Risk Premium: The final component of a discount rate is the specific company risk premium. This represents the “risk profile” specific to the individual subject company above and beyond the factors above – i.e., what is the required return an investor requires to invest in said company over any other investment?

To illustrate with an example, a soon-to-retire CEO of a small business maintains all client relationships. In assessing the potential risk(s) to the business, we would inquire about and assess the risk of clients leaving when the CEO retires. In addition to the risk of losing clients, there are other risks associated with the departure of a key executive. Valuation analysts refer to these risks as “key person risk,” or “key person dependency.” We would also assess depth of other management and succession planning. A few additional examples, but certainly not all, of company specific risk are shown below:

Customer/Supplier Concentration: If the ongoing level of earnings/cash flow is heavily dependent on one key customer/vendor, and the loss of said customer/supplier would lead to significant revenue loss, a risk premium is appropriate.

Product Diversification: Does the company reap sales from a one hit wonder product, or are other product offerings available that diversify this risk?

Product Evolution/Research & Development: Is there research & development to keep the products evolving with consumer demands and technological advancements?

Geographic Concentration: If a company solely operates in one city or geographic region, the company could suffer if the local economy lags the growth of the national economy. Having operations in multiple locales would help reduce this risk. Also, concentration may create a ceiling to potential growth and expansion.

Earnings Volatility: Do earnings change significantly from year to year? If so, an investor in such a company would likely require a higher return to compensate for the uncertainty. (Note: it is important that the valuation analyst is cautious and does not double count risk considering the selected earnings stream. For example, if a company has one down year but the analyst includes it in a historical average, it may not be appropriate to add additional risk for earnings volatility. In this case, the risk may already be captured in giving weight to it in the analysis of ongoing earnings.)

Competitive Environment: Are there many competitors, and how does the company perform in comparison to those competitors? Does the company offer goods or services which are differentiated?

When determining a specific company risk premium, some analysts may choose to assess a company through a SWOT analysis – strengths, weakness, opportunities, and threats of the company – relative to past performance, performance of its peers, the industry, and the broader economy. Put simply, what is the risk profile of the business? If there are risks (or lack thereof) that are specific to said company, how much higher or lower does the discount rate have to be for an investor to be willing to invest in this company instead of an alternative company or investment?

The specific company risk premium is frequently an area where experts may differ due to selection of varying levels of risk for a company. While understanding what “feels” reasonable here takes nuance and experience, a valuation analyst should provide the attributes which support the selected risk premium.

What Is a Reasonable Discount Rate and What’s in Range?

Following our equity build-up example in Figure 1, adding a size premium of 5.0%, and specific company of 4.0% to an equity market return of 7.75% leads to a discount rate of 16.75%. For a smaller, riskier company, this could be higher; however, for a larger, less risky company with consistent history of strong earnings, this could be lower. An equity discount rate range of 12% to 20%, give or take, is likely to be considered reasonable in a business valuation. This is about in line with the long-term anticipated returns quoted to private equity investors, which makes sense, because a business valuation is an equity interest in a privately held company. Again, while many of the specific terms utilized in the build-up of a discount rate may be new to attorneys, rates of return quoted in that context are more familiar to many.

A business appraisal with a discount rate below 10% likely deserves more scrutiny, but it may be reasonable if the company is sufficiently large, diversified, well-capitalized, less exposed to market risk, has a strong management team and succession plan, and generates consistent cash flow and/or growth.

On the other end of the spectrum, a company with a discount rate in excess of 25% may be undervalued, and such a discount rate similarly deserves justification. However, there could be numerous reasons why this is ultimately reasonable given specific facts and circumstances. Early stage/start-up companies without sufficient history of earnings and performance would likely have a high discount rate. While there could be certain instances where a discount rate above 25% may be reasonable, a proper appraisal will enumerate in detail why such a large discount rate is warranted.

Conclusion

In financial situations that may be scrutinized by courts and other potential adversaries, an expert’s financial, economic, and accounting experience and skills are invaluable. These complex analyses are best performed by a competent financial expert who will be able to define and quantify the financial aspects of a case and effectively communicate the conclusion.

[1] Mercer Capital regularly reviews a spectrum of studies on the equity risk premium and also conducts its own study. Most of these studies suggest that the appropriate large capitalization equity risk premium lies in the range of 4.0% to 7.0%.

[2] W.F. Sharpe, “Capital Asset Prices: A Theory of Market Equilibrium Under Conditions of Risk,” Journal of Finance, Vol. 19 (1964): pp. 425-442.